March 2024 / INVESTMENT INSIGHTS

A decade-long adventure navigating treacherous markets successfully

The Dynamic Global Bond Strategy celebrates its 10-year anniversary this month since launch

Key Insights

- At its 10‑year anniversary, the Dynamic Global Bond Strategy’s strong focus on risk management helps it to navigate uncertain market environments successfully.

- The strategy’s three objectives of steady returns, capital preservation, and diversification are driven by a decentralized, research‑driven investment process.

- In multi‑asset portfolios, the strategy serves as a defensive anchor, pursuing enhanced risk‑adjusted returns.

As the Dynamic Global Bond Strategy1 celebrates its 10‑year anniversary in February since launch, we analyze the key drivers for performance, whether the strategy has kept up with the changing times, and if it is still relevant in a market environment that is a mirror image of the time when it was launched.

The strategy’s origins were rooted in the years following the global financial crisis when the highly accommodative monetary policy stances of major central banks resulted in a significant hunt for yield in fixed income markets. This led many investors to seek higher income by taking on greater risks in credit sectors such as investment grade and high yield. However, these sectors tended to be less liquid than government bonds and positively correlated to equity markets, so they typically suffered when there was a sell‑off in risk assets. Therefore, an opportunity to develop a fixed income product focused primarily on interest rate management as opposed to broadly taking on credit risk resulted in the birth of the strategy a decade ago.

The role of the Dynamic Global Bond Strategy

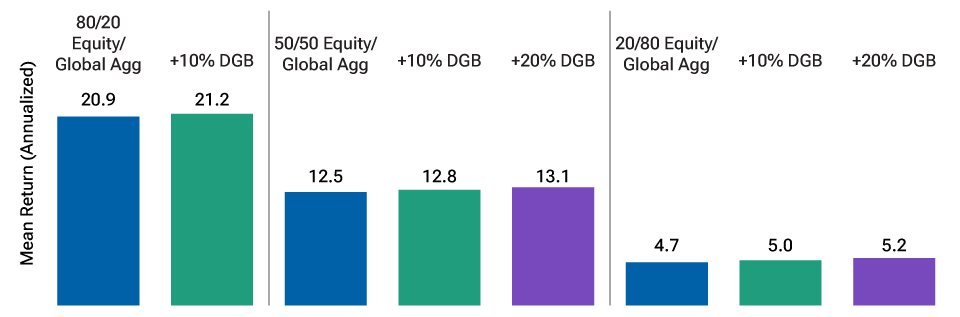

(Fig. 1) Allocations to the strategy improved risk‑adjusted returns for a traditional stock/bond portfolio

As of December 31, 2023.

The information shows hypothetical results, which are shown for illustrative purposes only and are not indicative of realized past or future performance.

Actual investment results may differ significantly. As the hypothetical portfolios are based on the performances of market indexes and the Dynamic Global Bond (USD Hedged) (DGB) Composite as described, index performance does not incorporate fees, expenses, or any other costs associated with an actual investment. The DGB Composite returns are calculated net of fees. Net of fees performance reflects the deduction of the highest applicable management fee that would be charged based on the fee schedule contained within this material, without the benefit of breakpoints. It reflects the reinvestment of dividends and are net of all non‑reclaimable withholding taxes on dividends, interest income, and capital gains. The assumed rebalancing frequency of the hypothetical portfolios is on an annualized basis. See the appendix for additional details on the study methodology and for important information regarding hypothetical performance.

Sources: Bloomberg Finance L.P. Analysis by T. Rowe Price. Equity is represented by S&P Total Return Index. Global Agg is represented by Bloomberg Global Aggregate Index. DGB is represented by T. Rowe Price Dynamic Global Bond (USD Hedged) Composite (see Additional Disclosures).

At a broad level, the Dynamic Global Bond Strategy’s success stems from its unwavering focus on its three main objectives: steady returns, capital preservation, and diversification from risky markets.

Mitigating risks

“The number one focus is to generate strong relative returns when clients need us the most,” said Scott Solomon, co‑portfolio manager for the Dynamic Global Bond Strategy.

In 2014, yields across bond markets were near zero and major stock markets had only managed to recoup their losses from the global financial crisis. Flash‑forward 10 years, and developed bond market yields are at multiyear highs while stock markets are basking in record territory.

Some argue that bonds have regained their credibility as a diversifier against risky assets. However, higher yields have been accompanied by greater volatility in the fixed income markets as central banks have begun to unwind their bond purchase programs in the backdrop of rising debt issuance. Additionally, numerous stumbling blocks for the global economy abound while geopolitical hot spots are flashing red.

We believe these are fertile grounds for the strategy. Rising volatility and uncertain markets are scenarios under which the composite outperformed traditional markets. For example, in December 2022 when major stock markets declined by more than 5%, the composite gained. In the bond markets, when the 10‑year U.S. treasury yield climbed more than 80 basis points between August to October 2023, the composite outperformed. This is due to its structural design of having a substantial degree of risk hedges in the portfolio. And while there is a valid argument that policymakers can successfully steer the global economy through the numerous headwinds, the case for owning a strategy that can deliver outperformance when other asset classes are struggling is robust.

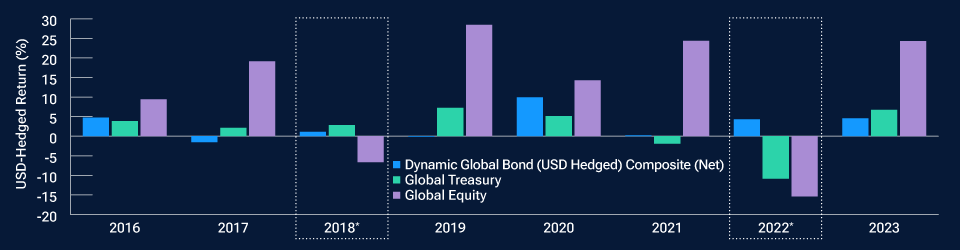

Differentiated returns for the Dynamic Global Bond (USD Hedged) Composite

(Fig. 2) Composite returns were uncorrelated to traditional bond and equity markets

As of December 31, 2023.

Past performance is not a reliable indicator of future performance.

* 2018 and 2022 were years when other asset classes underperformed compared with the composite in the backdrop of increased market volatility.

Sources: T. Rowe Price, Bloomberg Finance L.P. Composite return is shown net‑of‑fees return. Net of fees performance reflects the deduction of the highest applicable management fee that would be charged based on the fee schedule contained within this material, without the benefit of breakpoints. It reflects the reinvestment of dividends and are net of all non‑reclaimable withholding taxes on dividends, interest income, and capital gains. Global Treasury is represented by Bloomberg Global Treasury Index USD Hedged. Global Equity is represented by MSCI World 100% Hedged Net Total Return USD Index (see Additional Disclosures).

The composite’s strong track record is rooted in its sound risk management approach. During buoyant market conditions, the strategy aims to deliver a cash‑like return due to its majority holdings in the deep liquid government bond markets. But when risk markets come under intense selling pressure, the strategy aims to provide portfolio stability and the composite generated outperformance vs. traditional equity and fixed income markets as seen during the pandemic period in 2020 and the aggressive policy tightening period in 2022.

Evolution of the strategy

At the core of the strategy’s success is our robust research platform, the powerful engine that generates our investment ideas. Covering more than 80 countries and over 40 currencies, our deep research capabilities enable us to uncover inefficiencies and exploit opportunities across the full fixed income universe.

The strategy has zero home bias, and our ability to unearth alpha via duration management is a testament to the strong research‑driven investment process that is constantly evolving. For example, the investment team recognized last year that Latin American economies would be among the first cohort of countries to cut interest rates in this economic cycle as they led the global economy in tightening monetary policy in 2021, recognizing surging inflationary pressures.

Second, the strategy’s allocation to risk‑hedging positions to adhere to its capital preservation goal has typically resulted in increased costs. However, in recent years, the investment team has made meaningful progress in using derivatives to reduce the associated costs while maintaining its focus to shield against downside risks in risk markets.

Moreover, the strategy’s predominant investments in the global government bond markets mean that it remains liquid and supports clients’ demand for liquidity even during market stress events, such as the UK pension fund crisis in late 2022.

The strategy has also benefited from a co‑portfolio management structure2 as it has broadened the perspective and increased the global reach of the portfolio. Quentin Fitzsimmons and Scott Solomon have complementary skill sets, with Scott having a strong credit background and Quentin possessing tenured experience in interest rate management and portfolio construction.

Portfolio anchor

“The strategy is an established diversifier in portfolios, having thrived when traditional asset markets faltered,” said Amanda Stitt, a portfolio specialist.

The composite underperformed the benchmark ICE BoFA U.S. 3‑month Treasury Bill Index in 2023. However, the strategy’s resolute focus on its objectives and its goal to provide portfolio ballast means the strategy retains its attraction as a core component in multi‑asset portfolios.

Investors typically view the role of fixed income as a diversifier in their portfolios. Put simply, when things go bad, they want something in their portfolio whose value would rise while everything else is declining. We think the Dynamic Global Bond Strategy fulfills a similar role in multi‑asset portfolios when viewed through the lens of a portfolio anchor as seen through its long‑term track record.

The strategy is not designed to outperform in every market condition because of the conservative nature of our investment process and adherence to our three objectives. For example, between 2017 and 2019 when equity markets were generating double‑digit returns and credit spreads were narrowing, the strategy underperformed. But during events of market stress, the strategy was an outperformer.

Moreover, allocating a portion of a typical stock/bond portfolio to the Dynamic Global Bond Strategy has the potential to enhance risk‑adjusted portfolio returns over multiple time periods, supporting the case for a continued allocation in broader asset allocations.

Conclusion

In a volatile market environment marked with different investment risks, the Dynamic Global Bond Strategy is a sturdy but flexible fixed income strategy. The strategy’s heavy emphasis on risk management at a security and a portfolio level means it is focused on its objectives. But it is also flexible due to its global remit and wide latitude in duration management as opposed to some of its more fixed income benchmark‑focused peers.

“The relevance of the strategy is as strong now as it was back then as debt levels rise and central banks navigate an uncertain economic environment,” said Quentin.

Dynamic Global Bond (USD Hedged) Composite

Risks—the following risks are materially relevant to the portfolio:

ABS and MBS—Asset‑backed securities (ABS) and mortgage‑backed securities (MBS) may be subject to greater liquidity, credit, default, and interest rate risk compared with other bonds. They are often exposed to extension and prepayment risk.

Contingent convertible bond—Contingent convertible bonds may be subject to additional risks linked to capital structure inversion, trigger levels, coupon cancellations, call extensions, yield/valuation, conversions, write downs, industry concentration, and liquidity, among others.

Credit—Credit risk arises when an issuer’s financial health deteriorates and/or it fails to fulfill its financial obligations to the portfolio.

Currency—Currency exchange rate movements could reduce investment gains or increase investment losses.

Default—Default risk may occur if the issuers of certain bonds become unable or unwilling to make payments on their bonds.

Derivative—Derivatives may be used to create leverage, which could expose the portfolio to higher volatility and/or losses that are significantly greater than the cost of the derivative.

Distressed or defaulted debt—Distressed or defaulted debt securities may bear a substantially higher degree of risks linked to recovery, liquidity, and valuation.

Emerging markets—Emerging markets are less established than developed markets and therefore involve higher risks.

High yield bond—High yield debt securities are generally subject to greater risk of issuer debt restructuring or default, higher liquidity risk, and greater sensitivity to market conditions.

Interest rate—Interest rate risk is the potential for losses in fixed income investments as a result of unexpected changes in interest rates.

Issuer concentration—Issuer concentration risk may result in performance being more strongly affected by any business, industry, economic, financial, or market conditions affecting those issuers in which the portfolio’s assets are concentrated.

Liquidity—Liquidity risk may result in securities becoming hard to value or trade within a desired time frame at a fair price.

Prepayment and extension—Mortgage‑ and asset‑backed securities could increase the portfolio’s sensitivity to unexpected changes in interest rates.

Sector concentration—Sector concentration risk may result in performance being more strongly affected by any business, industry, economic, financial, or market conditions affecting a particular sector in which the portfolio’s assets are concentrated.

Total return swap—Total return swap contracts may expose the portfolio to additional risks, including market, counterparty, and operational risks as well as risks linked to the use of collateral arrangements.

General Portfolio Risks

Capital—The value of your investment will vary and is not guaranteed. It will be affected by changes in the exchange rate between the base currency of the portfolio and the currency in which you subscribed, if different.

Counterparty—Counterparty risk may materialize if an entity with which the portfolio does business becomes unwilling or unable to meet its obligations to the portfolio.

ESG and sustainability—Environmental, social, and governance (ESG) and sustainability risk may result in a material negative impact on the value of an investment and performance of the portfolio.

Geographic concentration—Geographic concentration risk may result in performance being more strongly affected by any social, political, economic, environmental, or market conditions affecting those countries or regions in which the portfolio’s assets are concentrated.

Hedging—Hedging measures involve costs and may work imperfectly, may not be feasible at times, or may fail completely.

Investment portfolio—Investing in portfolios involves certain risks an investor would not face if investing in markets directly.

Management—Management risk may result in potential conflicts of interest relating to the obligations of the investment manager.

Market—Market risk may subject the portfolio to losses caused by unexpected changes in a wide variety of factors.

Operational—Operational risk may cause losses as a result of incidents caused by people, systems, and/or processes.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.