November 2023 / INVESTMENT INSIGHTS

Perspectives on Securitised Credit

Third Quarter 2023

Key Insights

- Securitized markets produced mixed results amid rising rates, with lower-rated segments mostly leading.

- Light supply remains a technical tailwind except in asset-backed securities, where heavier supply has cheapened valuations in spots.

- Fundamentals are deteriorating, but at a gradual pace, and we see select areas of value within sectors.

Securitized credit markets generated mixed but generally favorable relative results in the third quarter (Q3) amid a further sell-off in the U.S. Treasury market. Treasury yields rose, particularly for longer-term maturities, causing a deeply inverted yield curve to markedly re-steepen. This has historically been an ominous sign for the economy, as similar past occurrences have been reliable leading indicators of a forthcoming recession. However, this episode has been somewhat unique as a “bear steepener”—or a curve steepening led by long-term yields increasing rather than short-term yields decreasing as was the case of most past instances that presaged economic downturns. Higher levels of U.S. government debt issuance, the Federal Reserve’s “higher for longer” guidance on interest rates, partisan discord over funding the U.S. government, and a spike in oil prices all played a role in the significant move higher in longer-term Treasury yields, which broadly weighed on bond prices.

In credit markets, investors appeared more confident that the Fed could engineer a soft economic landing. Securitized credit was generally resilient in the face of interest rate volatility and an unrelenting ascent in nominal and real Treasury yields that further tightened financial conditions. On the heels of a rally in the second quarter as concerns about the banking system diminished, credit spreads maintained a tightening trajectory through mid-August.1 Spreads widened to varying degrees later in the quarter and into October as the Fed remained resolute about keeping rates elevated well into next year, and increased geopolitical risks weakened risk appetite.

Negative Returns for Longer-Duration Sectors

With the rise in longer-term Treasury yields, sectors with longer-duration profiles produced more negative total returns.2 Conduit commercial mortgage-backed securities (CMBS) and parts of the non-agency residential mortgage-backed securities (RMBS) markets, such as nonqualified (non-QM) and jumbo mortgage loans, declined on an absolute basis. By contrast, areas with shorter durations and/or floating coupons—such as asset-backed securities (ABS), collateralized loan obligations (CLOs), and credit risk transfer (CRT) securities—recorded positive total returns.3

In most cases, bonds lower on the credit quality spectrum performed better on a duration-adjusted basis than higher-rated issues, indicating that investors were less concerned about credit risk than they were about interest rate risk. ABS, CRT securities, and CLOs were among areas where lower-rated debt outperformed, benefiting from higher spread carry as well as mild spread tightening.

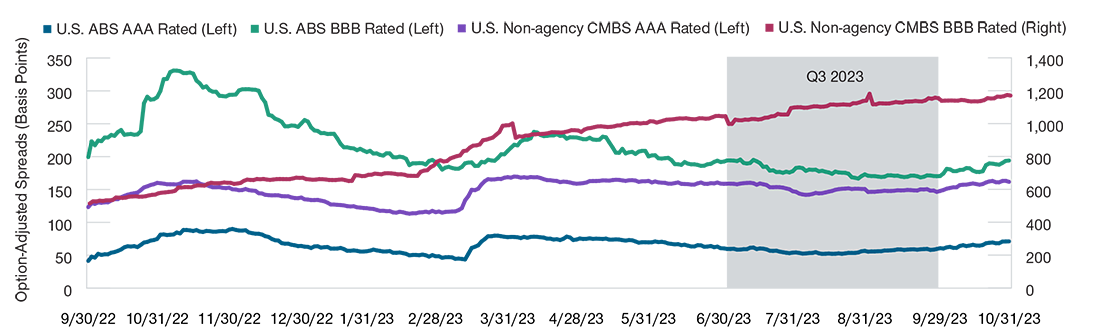

Securitized Credit Spreads Generally Tightened in Q3 2023

(Fig. 1) Lower-rated CMBS countered this trend as spreads continued to widen amid fundamental concerns.

September 30, 2022, through October 31, 2023.

Source: Bloomberg Index Services Limited. Please see Additional Disclosures page for additional information.

Indexes shown are the AAA and BBB credit quality tranches of the Bloomberg ABS Index and Non-Agency Investment-Grade CMBS indices using the index credit rating methodology.

The CMBS market ran counter to this trend as AAA and AA rated securities produced the strongest excess returns versus similar-duration Treasuries.4 Investors continued to have little interest in lower-quality CMBS given the significant, well-publicized fundamental challenges facing the commercial real estate (CRE) market. Spreads on BBB rated CMBS have steadily climbed since early 2022, when the Fed began vigorously raising borrowing costs to combat inflation. Although spread widening for lower-rated CMBS continued in Q3, the pace has eased somewhat, suggesting that selling may be nearing exhaustion (Figure 1).

Significantly Lower Issuance This Year Outside of ABS

As of mid-October, overall gross issuance across the U.S. ABS, CLO, CMBS, and non-agency RMBS market totaled USD 477 billion year-to-date, putting the market on pace to fall well short of 2022, when USD 754 billion came to market.5 Issuance volumes have plummeted since 2021, a year that saw more than USD 1 trillion in gross issuance for the first time since the 2008–2009 global financial crisis. The lighter issuance this year combined with inflows into U.S.-focused diversified bond funds provided welcome technical support for securitized credit spreads.

The RMBS and CMBS markets experienced the biggest slowdown in primary market activity. In RMBS, gross issuance broadly declined by over 50% compared with the same period in 2022 and is expected to remain tepid through the end of the year. The dearth of RMBS supply was most pronounced in the agency investor, jumbo prime, CRT, and single-family rental (SFR) markets. The drop-off was less severe in the non-QM market, which was hurt by a glut of supply in 2022, keeping upward pressure on spreads in that market niche.

In CMBS, issuance in the single-asset/single-borrower (SASB) and CRE CLO segments was down more than 70% compared with the same period in 2022, while the private-label conduit and agency CMBS subsectors saw smaller declines of roughly 30%. A recent development in the conduit CMBS market, where loans have traditionally been 10-year maturities, is the appearance of five-year mortgage loans. These shorter terms allow sponsors to lock in higher rates for less time, which could benefit them sooner if interest rates decline from today’s expensive levels. For investors, five-year deals provide a shorter-duration option in an uncertain rate environment.

The CLO market saw USD 98 billion of issuance through mid-October, down about 30% from the same period in 2022. Most of that total consists of true new issuance rather than refinancings and resets of previous deals, as many deals exiting their non-call periods were issued when CLO spreads were at tighter levels. However, refinancing and reset transactions picked up a bit over the past quarter. The arbitrage incentive for CLO managers, which stems from the spread differential between bank loan assets and CLO debt liabilities, has also been weak, disincentivizing new CLO formations, which had flourished in recent years. For incentives to improve, loan valuations either need to cheapen or CLO spreads need to tighten.

The ABS market is the lone sector where gross issuance is on track to surpass 2022’s robust level of USD 243 billion. September was the heaviest month of ABS issuance this year as the market reawakened following the August vacation season. Demand was healthy, but the ample supply caused spreads to drift wider from their August lows. As of mid-October, year-to-date issuance totals were slightly higher than at the same point last year. The increase was primarily due to higher auto-related issuance—particularly prime auto loans as well as lease and fleet lease deals. Subprime auto loans, an area where rising delinquencies have garnered attention, saw slightly less issuance. Equipment deals maintained a steady pace, but other major areas like credit cards and student loans experienced lighter volumes than last year.

Valuations are Highly Varied

Our valuation framework analyzes pricing in our sectors from numerous angles, including on an isolated basis relative to historical spread levels, compared with spread-sector alternatives (e.g., agency MBS and corporate bonds), and relative to other securitized sectors. We also take into account the level of interest rate volatility and make valuation adjustments accordingly.

Based on our most recent analysis, securitized credit sectors overall look slightly cheap relative to corporate credit but are somewhat rich compared with agency MBS. CLOs and RMBS broadly screen as more expensive, while specific parts of the CMBS and ABS markets offer the most value. In general, senior tranches are more dearly valued than subordinate tranches. Areas that we have found more attractive from a valuation standpoint include AAA rated CMBS, prime auto ABS across the quality spectrum, and subordinate equipment ABS. Lower-rated CMBS optically look quite cheap, with spreads on BBB rated non-agency bonds at more than 1,000 basis points above comparable Treasuries.6 But this is an area where we are treading carefully.

Fundamentals Trending Negatively

While the fundamental picture is largely neutral at present, the trend is mostly negative across sectors. Yet the deterioration in fundamentals has been gradual and is largely reflected in current prices, in our analysts’ opinions.

ABS: A tight U.S. labor market, resilient wage growth, and record household wealth are supportive of consumer spending and, by extension, ABS fundamentals. But the resumption of student loan payments and the depletion of savings accumulated during the pandemic period, particularly for lower-income households, will be headwinds going forward. Delinquency rates have increased across consumer ABS sectors, a trend that we expect to continue but remain manageable.

The health of the lower-end consumer is an area that bears watching. In the auto loan sector, for example, the rate of non-prime loans that were more than 60 days delinquent reached 6.1% in September according to rating agency Fitch. By contrast, the delinquency rate for prime auto loans was only 0.3%, a subdued rate consistent with the longer-term average. Similar divergent trends can be seen in credit cards. With fundamentals deteriorating at a faster pace for consumers with lower credit scores, strong collateral and deal structure analysis are essential to ensure that the loans backing deals are sound and that bonds have sufficient structural protections to absorb losses.

CLOs: The bank loan market, which underlies CLOs, has produced impressive performance this year in the face of higher rates and recession worries. However, higher borrowing costs have begun to take a toll on more leveraged loan issuers, and we expect the bank loan default rate to rise over the next year from its current level below 3%. Loan downgrades from the major rating agencies have exceeded upgrades, driven by the B- rating bucket. The subsequent increase in CCC rated loans has ramifications for the CLO market given that CLOs are typically penalized if that credit quality bucket exceeds more than 7.5% of the portfolio. Falling interest coverage ratios will likely cause an acceleration in downgrades, and we expect recoveries in default scenarios to remain well below historical levels due to weaker loan covenants. Given these developments, we maintain a higher-quality bias in CLOs at present.

CMBS: The fundamental challenges facing the CRE market have received considerable attention in the financial press, with much of that focused on the office segment. While offices remain the epicenter of concern, we expect to see pressures in other sectors. Retail SASB bonds are challenged by increased online shopping, store closures, and a slowdown in luxury goods spending. Our analysts also have some concerns about the SASB multifamily apartment segment; debt-servicing costs have increased substantially due to most issuance being floating rate, and many loans are 2021–2022 vintages, when property values peaked. We are more confident in the lodging and industrial SASB segments, and the collateral diversification found in the conduit subsector should be fundamentally supportive.

RMBS: Mortgage delinquency rates have generally remained stable so far in 2023 for most subsectors and have not strayed far from pre-pandemic levels. An incremental pickup in delinquencies in the non-QM and prime jumbo segments is not yet worrisome to us. Given the stabilization in home prices, aided by a shortage of supply, and continued strength in the labor market, we expect RMBS collateral performance to exhibit only modest deterioration through the rest of the year. But the continued rise in mortgage rates and stretched home affordability will likely cause a deceleration in home price appreciation, and mortgage delinquencies will inevitably rise if tight Fed policy causes a rise in unemployment.

Select Opportunities Across Securitized Credit Sectors

With spreads at wide levels, CMBS clearly offer the most value from a spread carry perspective, and this is where we have the highest conviction in long-term value given that the market has already priced in poor outcomes. Yet we remain highly selective for the fundamental reasons noted above. Segments that we like in the beleaguered sector include junior AAA rated conduit deals, which offer substantial credit enhancement to help shield investors from losses. In the largely floating rate SASB segment, our analyst team has preferred lodging credits where refinancing prospects are better. If issuers are able to refinance, discounted bond prices could rise to par value, boosting return potential.

Abundant issuance in the ABS market could continue to create attractively priced opportunities. We also like the defensive characteristics of the sector at this stage of the credit cycle. ABS are typically a more stable sector and should hold up better if securitized spreads widen into the end of the year. We particularly like subordinate prime auto loans, timeshares, and equipment deals.

RMBS valuations are on the richer side of fair, but fundamentals are not overly concerning. The interest rate-sensitive sector was punished by the sharp rise in rates since early 2022 but should conversely perform well if rates decrease as the Fed concludes tightening policy. However, a soft-landing scenario would certainly be better for the sector than policy easing that is in response to recessionary conditions. We currently like new issue non-QM bonds at the AAA level, which offer attractive spreads on high-quality assets. We also like AAA rated prime floating rate debt with higher coupons and SFR bonds across the capital structure. These areas should hold up better than other sectors if rates continue to rise and volatility remains high.

Finally, CLO valuations screen rich, and fundamentals are skewed negatively. The sector also needs a catalyst for spreads to tighten. A potential catalyst is a revival of demand from banks, but we do not foresee that happening until well into 2024. At present, we favor AA rated CLOs. They offer a decent amount of spread pickup versus the highest-quality AAA rated tranches. We are wary of moving too far down the capital structure, as we expect the credit curve to steepen, with spreads on lower-rated mezzanine tranches widening the most, if the economy weakens and loan downgrades and defaults pick up. Additionally, although the timing of rate cuts appears to have been pushed back, demand for floating rate instruments like CLOs could wane if rates eventually moderate.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

November 2023 / INVESTMENT INSIGHTS

November 2023 / INVESTMENT INSIGHTS