March 2022 / INVESTMENT INSIGHTS

How We Are Navigating Upheaval in Energy Markets

Long-term fundamentals continue to guide our investment approach.

Key Insights

- Russia’s invasion of Ukraine could lend urgency to the clean energy transition and encourage policymakers in Europe to view legacy fuels more pragmatically.

- Oil prices are likely to be volatile as news flow related to the conflict comes out. Still, high oil prices should cure high oil prices over time.

- Our approach to the energy transition seeks quality companies with strong core businesses that could benefit from, but do not wholly depend on, this trend.

Russia’s invasion of Ukraine, followed by an escalating exchange of sanctions with the West, has ratcheted up volatility in the energy markets. We continue to monitor how this highly fluid situation is evolving. Instead of trying to predict the exact outcome of what might occur based on developments that are very hard to forecast, we are focusing on two areas:

- Where we see likely changes based on what has already occurred and

- Our rigorous analysis of long‑term fundamentals and deep understanding of individual companies, which continue to drive our investment approach.

Following the data and focusing on what the world might look like after a crisis can help us to avoid overreacting to short‑term volatility and aid in identifying potential longer-term opportunities.

Despite the lack of clarity surrounding the Ukraine‑Russia war and its ramifications, we believe that Russia’s actions thus far likely have shifted the calculus for energy policy, with supply security concerns significantly elevated and becoming more intertwined with environmental considerations. Governments may seek to accelerate efforts to wean their economies off fossil fuels but, at the same time, may show more pragmatism around diversifying the legacy sources of baseload power, especially to the extent that eurozone member states strive to reduce their reliance on Russian natural gas. Given the uncertainty surrounding these transitions, we tend to gravitate toward high‑quality companies whose growth stories, in our estimation, could benefit from these trends but do not entirely depend upon them.

The near‑term outlook for oil prices will likely remain volatile as markets digest the latest news flow. At the same time, history suggests that although geopolitical risks may drive oil prices in the near term, fundamentals tend to hold sway over longer time horizons. In our view, the cure for high oil prices is still high oil prices because they can stifle demand and incentivize a supply response to help rebalance the market over time. We remain selective in our positioning in oil and gas companies.

Additional Impetus for the Clean Energy Transition

We believe Russia’s invasion of Ukraine was enough of a shock to energy security that, regardless of the ultimate duration of the conflict and the severity of associated disruptions to global energy markets, policymakers in key economies are likely to seek to accelerate the push to clean energy. That said, we would expect governments to take a more pragmatic approach to the pace at which they phase out of legacy sources of energy, as supply security now becomes an important factor in shaping policy.

The case for policies supporting a clean energy transition often centers on concerns about greenhouse gas emissions and their contributions to climate change. Russia’s attack on Ukraine likely elevates the importance of energy security in this equation, serving as a reminder that Europe’s concentrated reliance on imported fossil fuels from potentially unreliable sources could be a vulnerability.

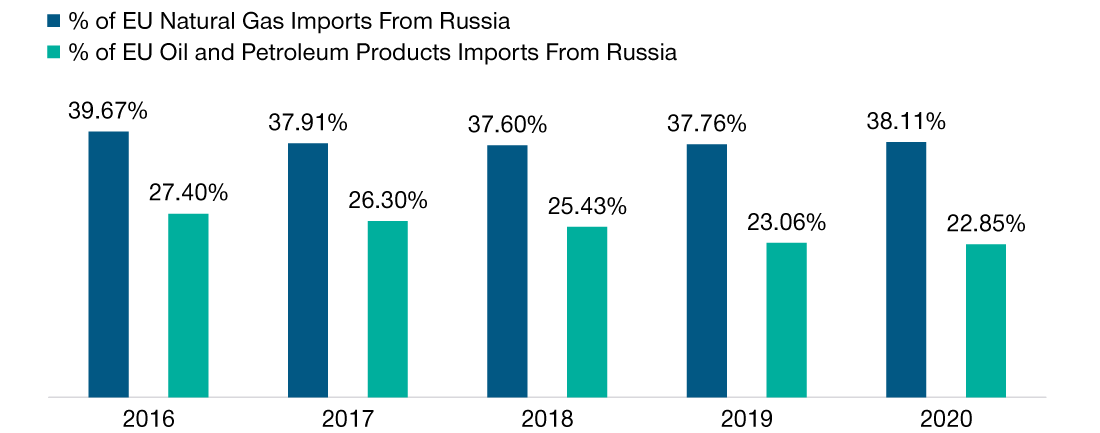

These risks ring particularly true for the European Union (EU), which in 2020 sourced more than 35% of its imported natural gas and almost 23% of its crude oil and petroleum products from Russia (Figure 1).

Noting that the EU last year imported the equivalent of 90% of the natural gas it consumed over that period, the European Commission on March 8, 2022, issued a highly ambitious framework, dubbed REPowerEU, for dramatically reducing the bloc’s reliance on volumes sourced from Russia by 2030. Renewable power, battery storage, and so‑called green hydrogen produced by clean energy‑powered electrolysis are among the areas of emphasis. Although the economic feasibility of and timelines for executing these proposals are open to question, the sentiment underlying this proclamation suggests that the clean energy transition has gained additional urgency among policymakers.

Investing in the Energy Transition

We have long believed that the global transition from fossil fuels would take significant time and investment, although the scope, complexity, and cost of the challenge make us less certain about the exact timing and the paths different economies might take to achieve these goals.

Against this backdrop, we seek to avoid speculative names where the underlying business strikes us as being of questionable quality or instances where the stock appears to trade at a prohibitively high valuation. Instead, we tend to gravitate toward established companies where we believe exposure to these secular trends could enhance their already appealing core businesses—for example, by boosting growth or expanding their addressable markets. We also evaluate whether we think a company’s economics can remain palatable in an environment where cost deflation and government subsidies are often critical to encouraging widespread adoption.

Regulated U.S. utilities are one area where we continue to find opportunity. We believe that the market does not fully appreciate the potential durability of these companies’ cash flow growth as they add wind and solar power capacity, reinforce critical infrastructure against extreme weather, and invest in much‑needed upgrades and expansions to aging electricity grids. Indeed, we view grid modernization as essential to rising adoption of wind and solar power as well as electric vehicles, potentially creating a durable secular tailwind for a variety of companies with exposure to this trend.

European Union Has Relied Heavily on Energy Imports From Russia

(Fig. 1) Percent of annual EU natural gas or oil and petroleum products sourced from Russia*

As of December 31, 2020.

Source: Eurostat. Data analysis by T. Rowe Price.

*By volume.

A Renewed Pragmatism Toward Legacy Fuels?

Stepped‑up investment in renewable energy and other technologies at the heart of the clean energy transition is unlikely to be enough to wean the eurozone off imported natural gas in the near term, regardless of where these volumes originated.

The intermittent nature of these clean energy sources, and the nascent state of storage solutions, makes it difficult for systems to match electricity supply and demand at a given time. Solar energy poses a particular challenge because peak daytime production does not correspond with peak demand, which typically occurs during the evening. Accordingly, access to a flexible source of baseload power—the sort provided by nuclear reactors and gas‑ or coal‑fueled power plants—is critical to offsetting these imbalances and avoiding service disruptions.

EU efforts to reduce imports of natural gas from Russia could prompt some countries to increase the utilization rates and extend the operating lives of baseload generation powered by legacy fuels, including coal and uranium. Policymakers’ appetite for potential price inflation could also dictate the aggressiveness with which member states might move, as competing for cargos of liquefied natural gas (LNG) in a tight global market would be expensive in the near term. Meeting this increased demand for LNG could also require potential suppliers to build additional export capacity—capital‑intensive projects that usually require long‑term offtake agreements to move forward. European nations might also need to build additional import terminals, depending on the extent to which they seek to replace Russian pipelines with LNG cargos.

Given the uncertainty regarding how aggressively the EU plans to rely on the LNG market to substitute for Russian pipeline supplies, we favor high‑quality companies that we believe would benefit in this scenario but also offer exposure to other potential upside catalysts in which we have conviction.

High Oil Prices Are Still the Cure for High Oil Prices

Near‑term news flow related to Russia’s invasion of Ukraine is likely to continue to drive volatility in crude oil prices. We can envision several scenarios that could propel what we regard as already elevated spot prices for crude even higher, including wartime damage to pipeline infrastructure, sanctions that make it harder for counterparties to purchase oil from Russia, or Russia cutting off hydrocarbon sales to some nations.

Regardless of how this highly fluid situation plays out, we note that the market’s natural rebalancing mechanisms remain in place: High oil prices eventually should be the cure for high oil prices, in our view.

The basic mechanics of this rebalancing process are familiar, even if the exact circumstances differ. On the other side of the massive demand shock that occurred during the pandemic, the recovery in supply will take time to catch up as elevated prices incentivize producers to step up drilling and well completions. Meanwhile, oil prices have reached levels where we would expect some degree of demand destruction globally, especially as this is occurring against a backdrop of dramatically elevated coal and non-U.S. natural gas prices and upward cost inflation pressures in other areas of the economy. In our view, this backdrop, along with likely improvement in well productivity, remains supportive of our view that oil prices should normalize lower over the long term.

We remain highly selective in our energy holdings. In keeping with our mandate, we aim to maintain a philosophically appropriate level of risk‑adjusted exposure to these commodity‑sensitive industries through valuation discipline and a focus on what we regard as the highest‑quality names.

Russia’s invasion of Ukraine has roiled global energy markets and, predictably, prompted an abundance of noise and speculation about the possible near‑term implications. We remain focused on the long term, where we see the potential for both increased support for clean energy as well as a more pragmatic approach to natural gas and legacy energy sources in Europe. The oil market’s natural rebalancing process also remains intact, in our view, though we believe these forces are likely to take time to play out and that volatility is likely to remain elevated in the near term. We continue to monitor this highly fluid situation and seek to arbitrage our deep knowledge of individual companies and industries, with an eye toward managing risk and identifying potential opportunities.

Risks—the following risks are materially relevant to the portfolio:

Sector concentration risk—the performance of a portfolio that invests a large portion of its assets in a particular economic sector (or, for bond portfolios, a particular market segment), will be more strongly affected by events affecting that sector or segment of the fixed income market.

General Portfolio Risks

Capital risk—the value of your investment will vary and is not guaranteed. It will be affected by changes in the exchange rate between the base currency of the portfolio and the currency in which you subscribed, if different.

Environmental, social, and governance and sustainability risk—may result in a material negative impact on the value of an investment and performance of the portfolio.

Equity risk—in general, equities involve higher risks than bonds or money market instruments.

Geographic concentration risk—to the extent that a portfolio invests a large portion of its assets in a particular geographic area, its performance will be more strongly affected by events within that area.

Hedging risk—a portfolio’s attempts to reduce or eliminate certain risks through hedging may not work as intended.

Investment portfolio risk—investing in portfolios involves certain risks an investor would not face if investing in markets directly.

Management risk—the investment manager or its designees may at times find their obligations to a portfolio to be in conflict with their obligations to other investment portfolios they manage (although in such cases, all portfolios will be dealt with equitably).

Operational risk—operational failures could lead to disruptions of portfolio operations or financial losses.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.