June 2023 / INVESTMENT INSIGHTS

High Yield Approaches Inflection

Security selection is imperative in an environment of higher credit volatility

Key Insights

- We believe that the asset class remains appealing, but security selection is critical as credit volatility could start to rise.

- 2023 is potentially a year of transition where the focus shifts from macro risks dominating to concerns over credit risk.

- The asset class is entering this inflection from a position of strength, however, which should help with navigating periods of higher volatility.

Where next for the high yield bond market? The asset class has bounced back strongly from the extremes of 2022 to deliver a total return of almost 8%1 for the six-month period ending March. Overall, we believe that the asset class continues to offer an attractive combination of compelling yields, solid fundamentals, and low exposure to interest rate risk. But security selection is imperative as an inflection nears with the market likely to shift focus later this year from macro concerns dominating to worries over credit risk.

The Yield Buffer

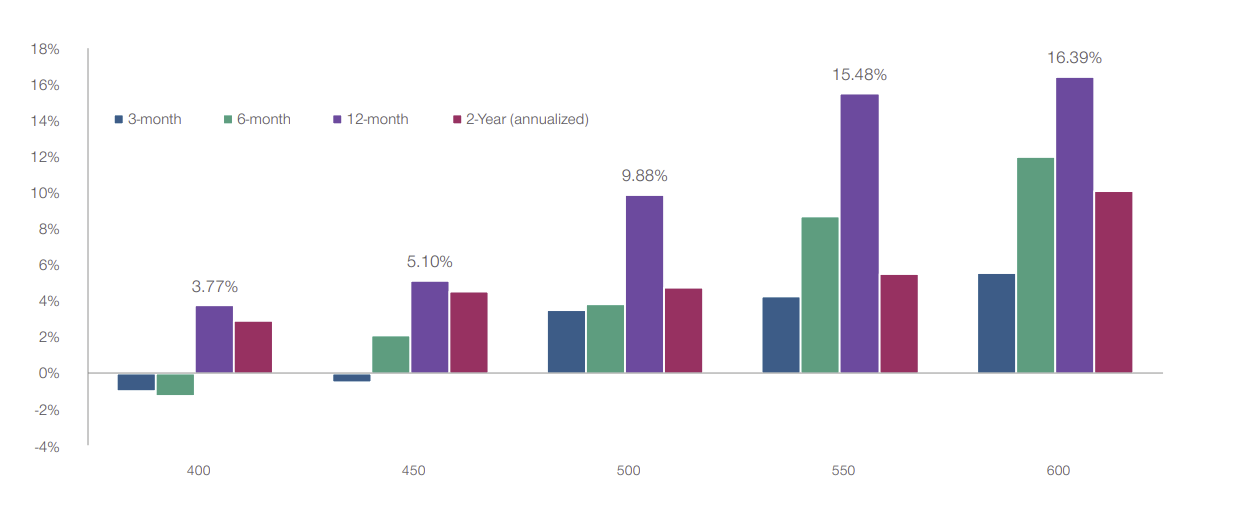

A unique feature of high yield debt is the yield “buffer” that it offers. High coupons should provide consistent and meaningful income, which helps dampen price volatility and has delivered attractive risk-adjusted returns over time. The sharp rise in yields during 2022 has meant that this buffer has returned, providing investors with a powerful compounding effect—March’s yield to maturity of 7.65% is meaningfully higher than the average of 4.64% over the past 10 years.2 Although European high yield bond spreads have somewhat tightened from the extremes of 2022, we believe there is still value. History shows that when spreads reach levels of 500 basis points or more, investors have typically gained positive average returns over the subsequent three-month, six-month, 12-month, and two-year time horizons (Figure 1). At the end of March, the spread-to-worst of European high yield debt was 504bps.

At current yield levels, we believe that investors continue to be well compensated for their risks, especially when combined with fundamentals and a duration of only just over three3 years. But we recognize that high yield debt issuers continue to face a difficult operating environment. On the one hand, sticky inflation is keeping input costs high; on the other hand, central bank rate hikes have driven up borrowing costs, which is curtailing consumer demand— and this may ultimately lead to recession. Firms facing high costs, falling demand, and weaker cash generation are at greater risk of default, which underscores the importance of security selection. Because it’s not just about picking potential winning companies; avoiding losers is just as important.

Inflection nears

For more than a year, anxiety over interest rate hikes, high inflation, and low growth, have overshadowed credit risk concerns for investors. But we expect this to increasingly shift as 2023 progresses because the slowing growth environment is likely to put the spotlight on companies, particularly the quality of their balance sheets and their ability to cover rising interest rate costs. This transition could mean increased bouts of credit-driven volatility in the future. Although this may be challenging, the asset class is entering this inflection from a position of strength, in our view, which should help with navigating periods of higher credit volatility. For example, the refinancing wave of 2020–2021 means that most firms have healthy levels of cash relative to debt on their balance sheets. They also were able to borrow at very low rates for a long time, enabling them to extend maturities out, so a lot of companies don’t need to issue bonds this year. Although, more will likely be required to return in 2024, it’s important to remember that companies tend to have debt with varying maturities spread over multiple years, so the impact of the rise in interest rates is not immediate – it’s smoothed out over time.

Overall, fundamentals continue to be supportive. Combined with attractive yields and low exposure to interest rate risk, we believe that the asset class remains compelling. But security selection is critical as some companies may not survive in a slowing growth environment. Against this backdrop, we believe that fundamental bottom-up research is essential, which is at the heart of our approach. We utilize our global team of credit analysts to select individual securities. Because macroeconomic and political developments—along with environmental, social, and governance (ESG) concerns—can also impact performance, we supplement our fundamental credit analysis with top-down insights from our team of sovereign and ESG analysts. We believe this approach enables us to fully understand a company and the potential risks and rewards involved with investing.

Figure 1: European high yield remains attractive

Average forward returns of European high yield at various spread thresholds*

Past performance is not a reliable indicator of future performance.

As of March 31, 2023.

*Uses historical European high yield returns to forecast average forward returns. European high yield is represented by the ICE BofA European Currency High Yield Index. The date range used is January 1, 2012 through March 31, 2023. Performance periods shown once index spreads moved through the spread threshold and had not been at that level for the preceding 30 business days.

Source: ICE BofA (see Additional Disclosures). Analysis by T. Rowe Price

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.