June 2023 / INVESTMENT INSIGHTS

Global Equities: Everything Changes, So Focus on What Stays the Same

Our investment framework is constantly adapting to the challenges of change

Key Insights

- Geopolitical concerns and the need for supply chain independence will require investors to identify which companies and regions will win from this realignment.

- We continue to look for quality companies in which we have insights into improving economic returns, while not paying too much for them.

- The portfolio is balanced across sectors and factors, with the goal of maximizing capture ratio, hedging exogenous geopolitical shocks while allowing us to still focus on idiosyncratic stock picking.

There have been three key surprises in 2023. First, a warm winter spared Europe with energy prices going from an icy headwind to a pleasant tailwind. Second, the Chinese economy proved less robust than investors expected as it emerged from its zero‑COVID policies. And finally, the artificial intelligence (AI) wave exploded into markets, with semiconductor company earnings driven higher by panicked spending from internet giants keen to be at the forefront of the AI revolution. We were positioned well for the third surprise.

Three Equity Market Surprises

(Fig. 1) Lower energy prices, a disappointing economic recovery in China, and AIexuberance pose challenges for investors

As of June 2023.

Past performance is not a reliable indicator of future performance.

For illustrative purposes only.

Source: T. Rowe Price.

COVID Distortions Have Muddied the Water

The aspect of the COVID cycle that confounds top‑down thinkers the most is how US Federal Reserve (Fed) rate hikes have failed to inflict significant pain on the global economy. Fed hikes are always dangerous because they are a catalyst for synchronised economic slowdowns. Hikes can lead to “black ducks”—chances for unexpected crisis—that sometimes turn out to be “black swans,” but not always. Rate hikes also tend to set credit cycles in motion that are contagious and bring economic subsectors and regions into a harmony of slowing sales, earnings, capex, and rising unemployment. No doubt, rising rates and the increased cost of capital will slow the global economy, but the questions are when, at what level will rates bite, and is there sufficient synchronization of a credit cycle to set off a major recession.

The twist of the COVID cycle is that consumers and businesses did a good job of “terming” out their debt through better mortgage and high yield bond refinancing. The flood of deposits that filled consumer and business bank accounts softened the shock of higher rates and have fended off crisis so far. Meanwhile, pandemic‑related supply chain and labor disruptions prevented companies from pursuing major fixed asset investments. Like a rich kid with a stubborn trustee, the money was kept safe and only moderately misspent on some cryptocurrency and exercise equipment. The result has been a lack of synchronization of “bad” things, continued strong employment trends, and a “too slow” bleed of excess savings. The bears have been frustrated by mistaking ducks for swans.

Need for Supply Chain Independence Will Extend Inflationary Forces

Geopolitical change has been a hallmark of the post‑COVID world, with the Russian invasion of Ukraine altering Europe’s energy landscape. Meanwhile, the steady deterioration of the relationship between the US and China has led us off the efficient frontier for global markets in terms of logistics, labor, productivity, and capital investment. The US and China are tangibly focused on reshaping their worlds for a more competitive future, despite the bounty of the past 30 years of linked growth. It is virtually impossible to decouple the two giants anytime soon, but there is no doubt that the US is seeking to secure its supply chain—onshore or “friend shore”—and China wants to find ways to break the US’s technological constraints. This will result in the need for new relationships that will require new investments. The key for equity investors will be identifying the companies and regions that can win from the realignment.

COVID money and geopolitical tensions have also acted to extend inflationary pressures, despite the fortuitous short‑term release valve of a slow China recovery and unexpectedly low energy prices. Sticky inflation will mean sticky interest rates, something the Fed has clearly signaled in describing a policy of higher rates for longer. This does not mean that we will not have short‑term periods of economic acceleration and deceleration, but—in general—interest rate cuts and a return to “secular stagnation” seem unlikely in the near term.

Operating in the New Environment

It is important to stress that a changing environment does not change our investment framework. We look for quality companies in which we have insights into improving economic returns in the future, and we do not pay too much for them. This framework is well suited for a changing world, but it requires the resources to recognise where change is happening. That is why the research platform at T. Rowe Price is crucial to our ability to be repeatable.

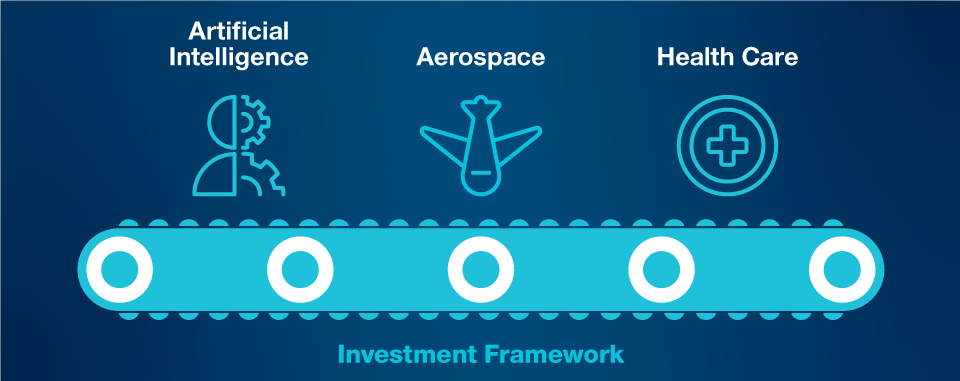

Operating in the New Environment

(Fig. 2) Three areas of focus using our investment framework

As of June 2023.

For illustrative purposes only.

Source: T. Rowe Price.

Encouragingly, the idiosyncratic investment opportunity set is rich. We are especially excited about AI, which will go through stages of infrastructure build, optimization, application development, disruption, and distribution. This will likely bring about a profound change across the global economy with opportunity for significant value creation (avoiding the charlatans along the way). There will be companies that successfully distribute and monetise AI and those that will be disrupted. One of the most interesting areas we are focused on is companies that can take AI technologies and monetise them through existing software and services offerings. Technology, financial, health care, industrial, and even natural resource companies have the chance to capitalise on significant change.

Elsewhere, aerospace is undergoing not only a recovery from COVID but also what we believe could be a multiyear improvement in returns driven by a consolidated industry structure, continued penetration of emerging markets, and technological innovation. There simply are not enough planes, parts, or engine service hours to keep up with demand.

The theme of onshoring and “friend shoring,” meanwhile, offers a broader and less understood opportunity. Energy security, logistics and transport, and the construction ecosystem could all offer new and fruitful opportunities.

There are also opportunities within health care. Heart disease, cancer, stroke, diabetes, and other causes of debilitation and death are strongly linked with obesity. New diabetes drugs that can manipulate the metabolic system that leads to significant and healthy weight loss can potentially reverse those conditions and increase healthy life spans. As these drugs get cheaper and move from injection to oral doses, there is a compelling case to be made for significant societal change. We are focused on understanding these drugs, their competitive positioning, and which companies stand to benefit the most from their adoption.

Overall, our portfolio now looks different from the one we owned from the global financial crisis through the pandemic. New opportunities are opening, while others are closing. We are managing the portfolio in a more balanced way across sectors and factors, with the goal of maximizing capture ratio, hedging exogenous geopolitical shocks while preserving the bulk of our positioning for idiosyncratic stock picking.

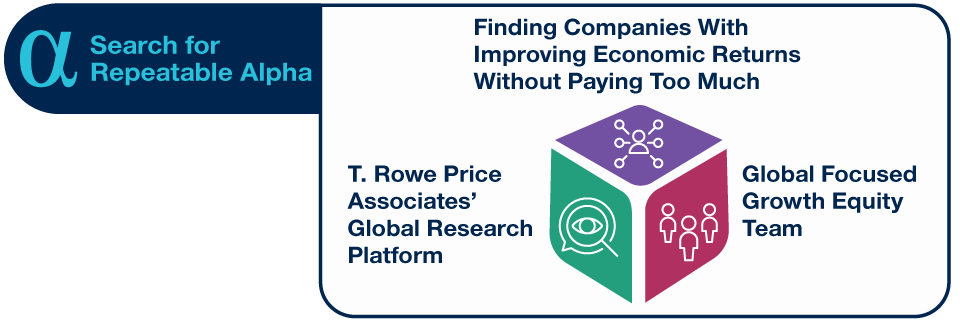

Executing Our Global Focused Growth Playbook

(Fig. 3) Keys to success: platform, framework, and team

As of June 2023.

For illustrative purposes only.

Source: T. Rowe Price.

Where Do We Stand Today?

Market breadth is extremely narrow. Small‑caps are out of favour, and value sectors are under pressure. China feels unloved and unowned. But mega‑cap tech has proven resilient and levered to AI trends. Returns, however, have been concentrated in just a handful of stocks. The VIX Index is under 16,1 but valuations—especially in large‑cap quality and growth areas—appear stretched and potentially unsustainable in a sticky inflation and interest rate future. We need to navigate the unfolding environment, and expect volatility into year‑end.

Although recession remains a risk, and a vocal minority in the market expects the Fed to cut rates this year, we are also thinking about the less obvious risk of a reacceleration in inflation fears, driven by stimulus response in China, OPEC energy policy, and simple seasonality in Europe. Winter is coming. This makes it prudent to own some commodity exposure and take advantage of more defensive/lower‑beta exposure when stocks are so cheap, in our view. Autumn/Fall will be an interesting season to observe how market positioning evolves.

Our job is to create repeatable alpha and be difficult to imitate. We continue to execute our playbook—platform (research), framework (improving returns without paying too much), and team (executing the framework). We think the global financial crisis to COVID environment is gone and we should embrace the changing nature of world politics and the global economy. Our goal as always is to put our clients first and on the right side of change.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

June 2023 / INVESTMENT INSIGHTS