June 2022 / INVESTMENT INSIGHTS

Global Asset Allocation Viewpoints

Our experts share perspective on market themes and regional trends, plus insights into current portfolio positioning.

Market Perspective

As of 31 May 2022

- While global growth is trending lower, recent economic data, especially pertaining to the labor market, has shown resilience amid geopolitical challenges, supply disruption, and reduction of liquidity.

- The U.S. Federal Reserve remains committed to its tightening policy, hinting at a frontloaded path of rate hikes. The European Central Bank (ECB) has telegraphed its plan to end asset purchases and begin raising rates despite a fragile macro backdrop, while the Bank of Japan remains steadfast on its policy of yield curve control.

- Emerging market central banks continue to tighten policy in response to heightened inflation and weak currencies, while China’s policies continue moving in the opposite direction to counter weakening growth caused by zero-COVID policy.

- Key risks to global markets include central bank missteps, lingering inflation, commodity impact of Russia-Ukraine conflict, sharp slowdown in economic data and China balancing growth amid COVID-related lockdowns.

Portfolio Positioning

As of 31 May 2022

- While equity valuations are more reasonable after recent declines, we remain cautious on the earnings growth outlook and inflationary impacts on margins supporting our modest underweight. Within fixed income, we remain underweight bonds and overweight cash.

- We continued to add to real assets-related equities, bringing the position to neutral, to provide a hedge should inflationary pressures persist longer, or settle higher, than expected.

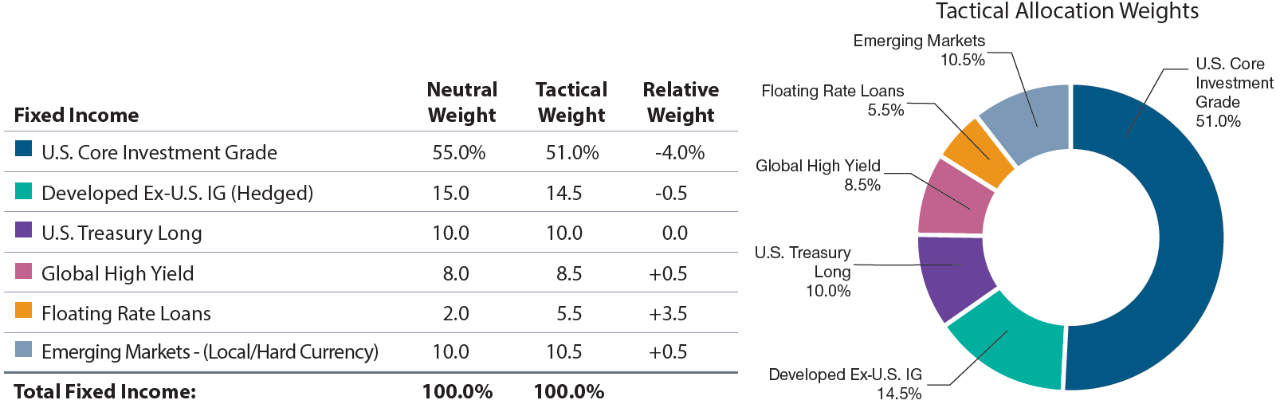

- Within fixed income, we moderated our floating rate loans exposure following a period of outperformance. While loans remain attractive, we reinvested profits in emerging market bonds and high yield given more compelling valuations.

- Despite attractive carry from elevated inflation levels, we trimmed our position in short-term Treasury inflation protected securities and added to cash as we expect inflation to moderate from current highs.

- Taking advantage of higher yields, we added to long-term U.S. Treasuries, providing mitigation against heightened global market risks.

Market Themes

As of 31 May 2022

So Far, So Good...

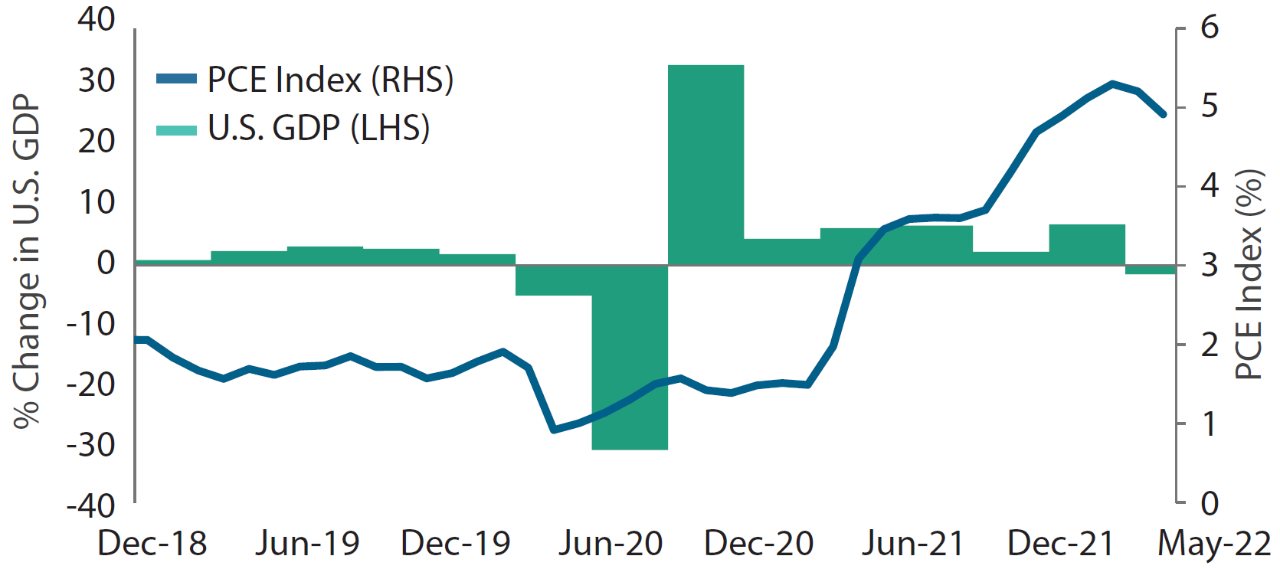

With inflation at multi-decade highs and growth already slowing, investors were rightfully skeptical about the Fed’s ability to aggressively tackle inflation without sending the economy into recession having waited too long. Now two hikes in and messaging frontloading future hikes with 50 basis point moves, recent data suggests the broader economy is largely holding up. Although first- quarter gross domestic product showed the economy surprisingly contracted by 1.5%, it appeared an anomaly due to temporary disruptions in trade and inventories, masking underlying support from consumer and capex spending. And while expected to slow, full year 2022 growth estimates still expect a 2.6% expansion, near pre-covid averages. Inflation too is showing some early signs of cooperating, with recent data suggesting easing in producer prices and wages, giving Fed officials a sigh of relief. While far from out of the woods, with top-line CPI still expected to be near 6% levels at year-end, so far it seems like maybe, just maybe a Fed-driven recession or stagflation are not inevitable.

U.S. GDP & Inflation1

As of 31 May 2022

Past performance is not a reliable indicator of future performance.

Sources: Bloomberg Finance L.P. and London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). Please see the last page for information about this FTSE Russell information.

1U.S. GDP is represented by the U.S. Gross Domestic Product Index quarter over quarter. The PCE Index is represented by the Personal Consumption Expenditure Core Price Index year over year.

Growth Spurt?

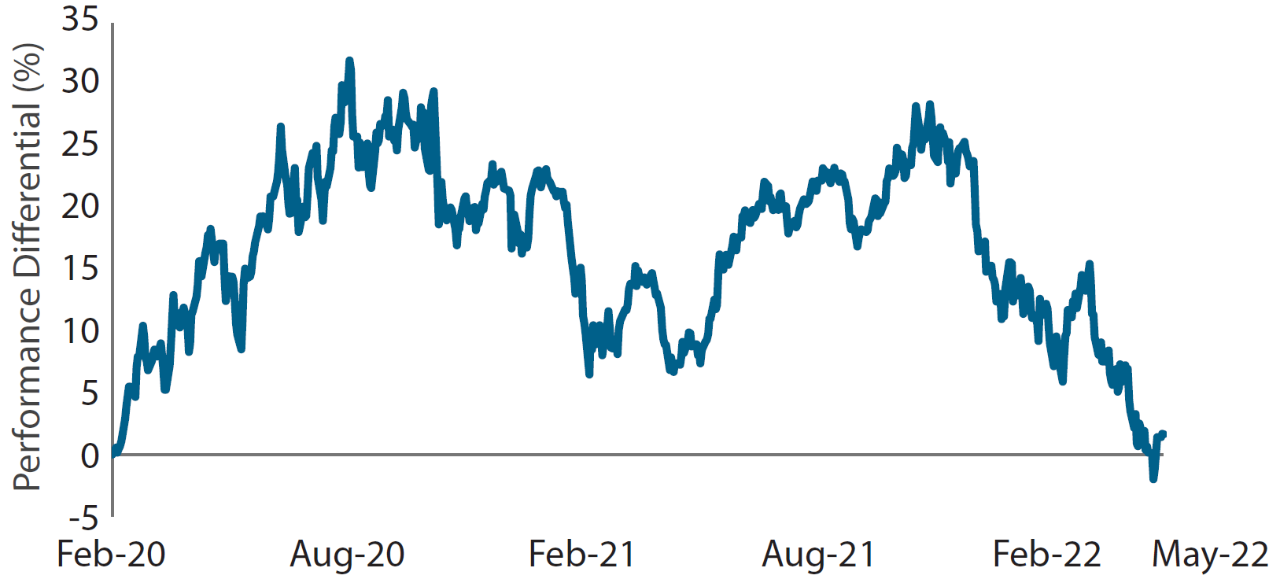

After more than a decade of outperformance versus value amid years of low economic growth, growth stocks went nearly parabolic during COVID lockdowns as many large-cap technology companies disproportionately benefitted from stay-at-home trends, sending valuations to record levels. That trend abruptly ended at the end of last year and has continued amid a spike higher in interest rates and threats of aggressive Fed tightening to battle multi-decade high inflation. The sharp drawdown in growth stocks has led to more reasonable valuations and the move higher in rates appears to be largely priced in as expectations for economic growth are moderating—historically a time when growth stocks have tended to outperform. While time will tell if this is a pivotal inflection in style back toward growth stocks, they still face near-term challenges on upcoming earnings comparisons and uncertainty around the path of Fed policy. But, for now growth could be due for a spurt higher as many of the tailwinds for value—higher energy prices and rates—may be peaking.

Growth vs. Value2

As of 31 May 2022

Past performance is not a reliable indicator of future performance.

Sources: Bloomberg Finance L.P. and London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). Please see the last page for information about this FTSE Russell information.

2Chart represents the difference between Growth and Value indices. Growth is represented by Russell 1000 Growth Index and Value is represented by Russell 1000 Value Index.

Regional Backdrop

As of 31 May 2022

| Positives | Negatives | |

|---|---|---|

| United States |

|

|

| Europe |

|

|

| Developed Asia/Pacific |

|

|

| Emerging Markets |

|

|

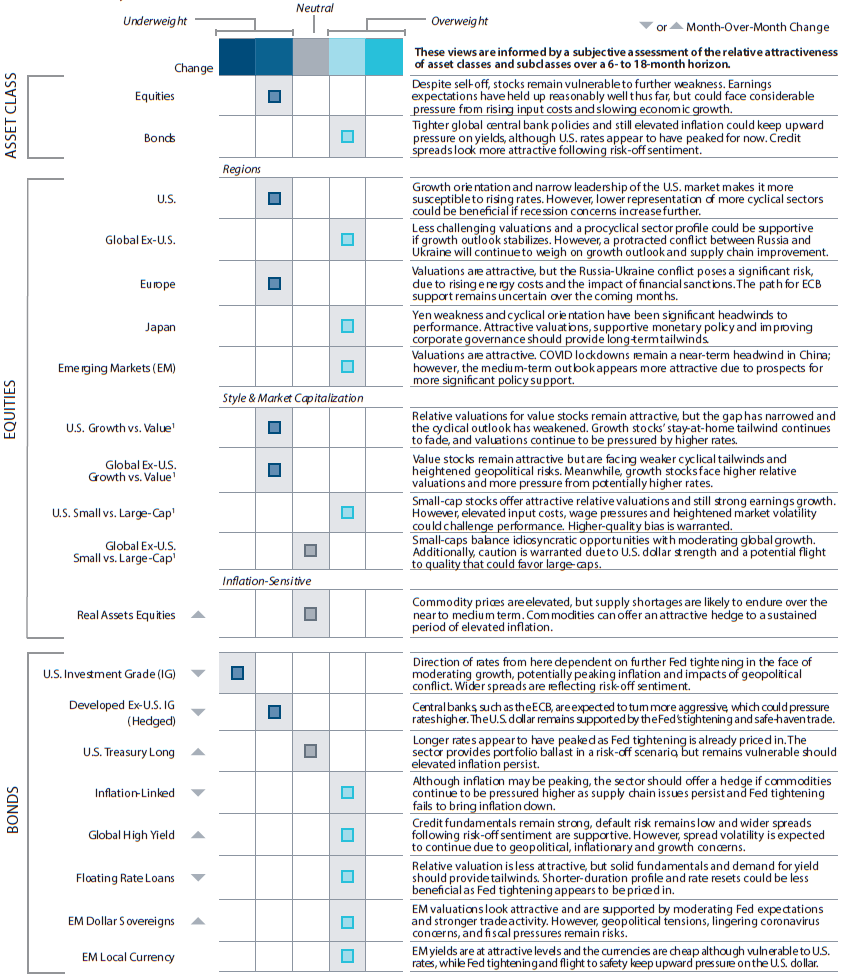

Asset Allocation Committee Positioning

As of 31 May 2022

1For pairwise decisions in style & market capitalization, positioning within boxes represent positioning in the first mentioned asset class relative to the second asset class. The asset classes across the equity and fixed income markets shown are represented in our Multi-Asset portfolios. Certain style & market capitalization asset classes are represented as pairwise decisions as part of our tactical asset allocation framework.

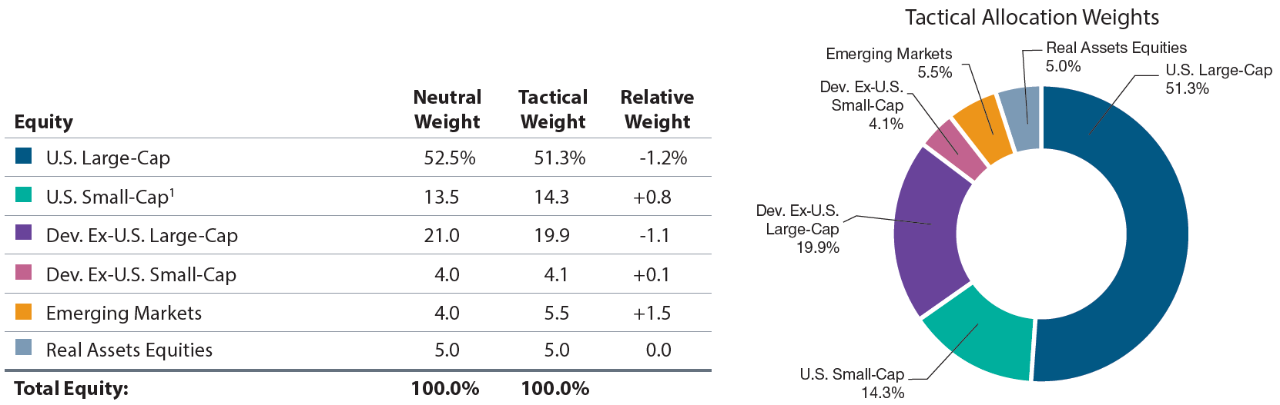

Portfolio Implementation

As of 31 May 2022

1U.S. small-cap includes both small- and mid-cap allocations.

Source: T. Rowe Price. Unless otherwise stated, all market data are sourced from FactSet. Copyright 2022 FactSet. All Rights Reserved.

These are subject to change without further notice. Figures may not total due to rounding.

Neutral equity portfolio weights representative of a U.S.-biased portfolio with a 70% U.S. and 30% international allocation; includes allocation to real assets equities. Core fixed income allocation representative of U.S.-biased portfolio with 55% allocation to U.S. investment grade.

Source: MSCI. MSCI and its affiliates and third party sources and providers (collectively, “MSCI”) makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI. Historical MSCI data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

“Bloomberg®” and Bloomberg Indices are service marks of Bloomberg Finance L.P. and its affiliates, including Bloomberg Index Services Limited (“BISL”), the administrator of the index (collectively, “Bloomberg”) and have been licensed for use for certain purposes by T. Rowe Price. Bloomberg is not affiliated with T. Rowe Price, and Bloomberg does not approve, endorse, review, or recommend Global Asset Allocation Viewpoints. Bloomberg does not guarantee the timeliness, accurateness,or completeness of any data or information relating to Global Asset Allocation Viewpoints.

London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). © LSE Group 2022. FTSE Russell is a trading name of certain of the LSE Group companies. All rights in the FTSE Russell indexes or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company’s express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication.

Important Information

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is no guarantee or a reliable indicator of future results.. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

USA—Issued in the USA by T. Rowe Price Associates, Inc., 100 East Pratt Street, Baltimore, MD, 21202, which is regulated by the U.S. Securities and Exchange Commission. For Institutional Investors only.

© 2024 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.

June 2022 / INVESTMENT INSIGHTS