March 2022 / MARKET OUTLOOK

Shifting Ground for Investors Amid Fiscal, Monetary and Geopolitical Risks

Insights Webinar Summary

Katie Deal, Investment Analyst, and Chris Dillon, CFA, Global Investment Specialist, recently spoke about what to expect from fiscal and monetary policy perspectives and the asset allocation considerations within today’s complex investment environment.

The views contained herein are those of the presenters as of the date noted and are subject to change without notice. These views may differ from those of other T. Rowe Price Group companies and/or associates. This material is not intended to be investment advice or a recommendation to take any particular investment action.

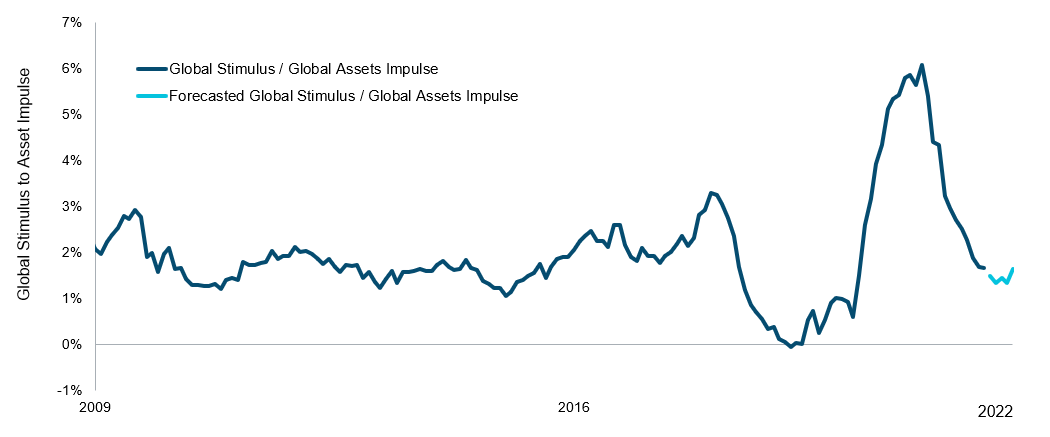

The Fed “Plot” Thickens

- Policy fade and peak earnings represented material headwinds for equity markets coming into 2022.

- Led by the U.S., massive global monetary and fiscal policy response met the economic ravages of the coronavirus pandemic head on during the back half of 2020 and into 2021.

- Largely as a result of this aggregated stimulus (in the range of U.S. $28 trillion), U.S. equity markets are still remarkably up in the range of 108% since March 23, 2020, through the end of March 2022.

- But as referenced in the chart below, the introduction of vaccines in late 2020 also meant that massive COVID-19-related policy response would not be repeated, which made “policy fade” a market headwind in the second half of 2021.

- Offsetting massive policy fade last year was remarkable earnings growth, which exceeded 60% for S&P 500 companies. Such a torrid pace of earnings growth appeared unsustainable heading into the new year. As a result, a multiple-driven market had become an earnings-driven market during late 2021.

- Coming into 2022, the combination of an earnings-driven market facing margin pressure and extraordinarily tough “comps,” an active Federal Reserve and the crisis in Ukraine represents a confluence of material market headwinds.

- There is some good news, however. The worst part of policy fade is now in the rearview mirror as is also depicted in the chart below.

Change in Global Stimulus

January 2009 to February 2022, Forecasts Through June 2022

Sources: Bloomberg Finance L.P., data analysis by T. Rowe Price. There is no guarantee that any forecasts made will come to pass.

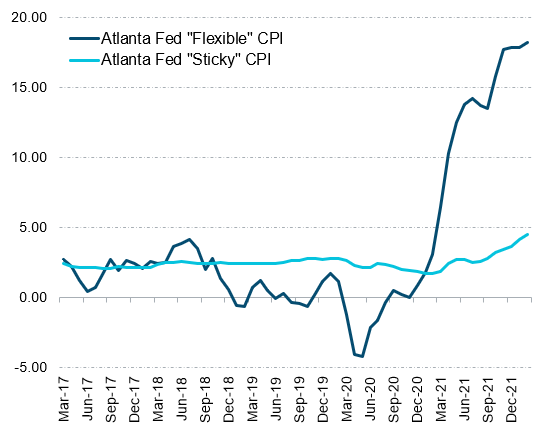

More Than “Transitory” Inflation, and Now War in Ukraine Is Forcing the Fed to Act Decisively

- In the current market environment, inflation has proven to be more than transitory.

- Domestic “Flexible” vs. “Sticky” consumer price index (CPI) as seen by the Federal Reserve Bank of Atlanta

- Before the crisis in Ukraine, Flexible CPI in the U.S. that measured quickly changing prices was trending in the materially high range of 18% but was largely connected to pandemic-related “friction” in domestic and global supply chains. This Flexible CPI trend was the key driver for 8% range “headline” inflation in the U.S.

- Sticky CPI, which captures those price change trends in the U.S. much less rapidly, also began to climb late last year as the market began to accept the fate of higher long-term inflation trends.

- The expectation that the pandemic transitioning to an endemic phase in 2022 was thought to be a catalyst for remedying domestic and global supply chain pressure, which, in turn, would help and decelerate inflation momentum. While this inflation relief phenomenon is still expected as this year progresses, the crisis in Ukraine now clouds this picture. Key agricultural and other commodities that come from Ukraine and Russia, for example, that will not only impact prices but also global supply chains, now come into question.

- The current environment, combined with monetary policy lessons from the 1970s, has forced the Fed into a more aggressive “front loaded” policy response playbook.

“Flexible" vs. “Sticky” CPI

Sources: Bloomberg Finance L.P., data analysis by T. Rowe Price.

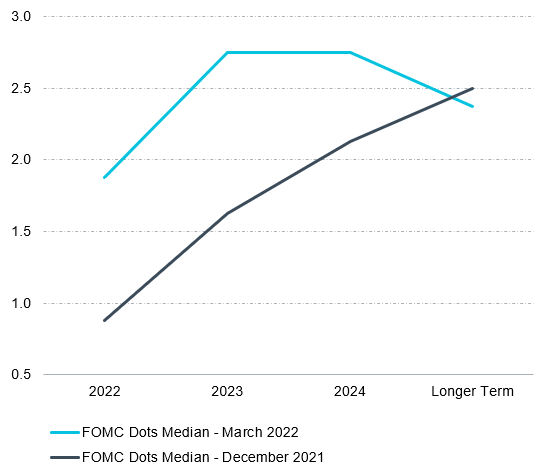

Fed Dot Plot – December 21 VS. March 22

Sources: Bloomberg Finance L.P., data analysis by T. Rowe Price.

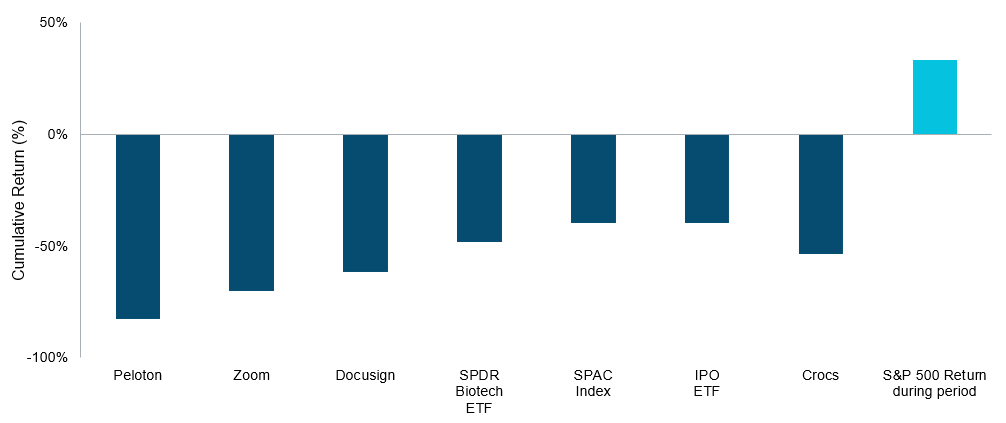

There Is Good News

- Last year, there was a significant amount of broad-based repricing in the market that has been broadly underreported in the financial press. While the S&P 500 Index was up over 28% last year, large portions of the market had been meaningfully repriced lower.

- Arguably, any resolution of the conflict in Ukraine could also represent a tailwind for markets as considerable pain has already been priced in.

- Certain emerging market equity strategies focused in Eastern Europe are down as much as in the 80% range year to date.

- Additionally, year-to-date, fixed income markets have experienced a scale of drawdowns that haven’t been seen in decades.

- With the valuation bar for global assets being reset lower than may generally be perceived, as illustrated in the chart below, there is room for some cautious optimism in the current environment.

Percent Price Drop From 2021 Peak to February 28, 2022 vs. S&P 500 Index Return

Past performance is not a reliable indicator of future performance.

Except for the S&P 500 Index, the stocks and asset classes referenced depict the drop in their respective peak market prices during the period December 31, 2020, through February 28, 2022, relative to their actual market prices as of February 28, 2022. These performance trends are then contrasted with the experienced total return of the S&P 500 Index during the same period from December 31, 2020, through February 28, 2022.

The specific securities identified and described are for informational purposes only and do not represent recommendations.

Sources: Bloomberg Finance L.P., Standard & Poor’s; analysis by T. Rowe Price.

Russia's “Revanchist” Aspirations Create a Difficult Diplomatic Spot for China

- The recent crisis in Ukraine stands in contrast to what has been a generally benign period for geopolitics during the past decade plus.

- The map displayed on the next page is of the Soviet Union as it was in 1989, before it dissolved in 1991. The map is important as Russian expansion in Georgia in 2008, in Crimea in 2014, and now in Ukraine has revealed what appear to be revanchist ambitions where Russia seeks to reclaim its former empire.

- Importantly, while many questions existed for Western leadership coming into 2022, the West does appear to have been unexpectedly galvanized in its support of Ukraine.

- But geopolitical complexity remains as approximately half of the world’s population has yet to condemn Russian action in Ukraine.

- Recent headlines indicate that Russia may want to sell oil to India but be paid in Russian rubles.

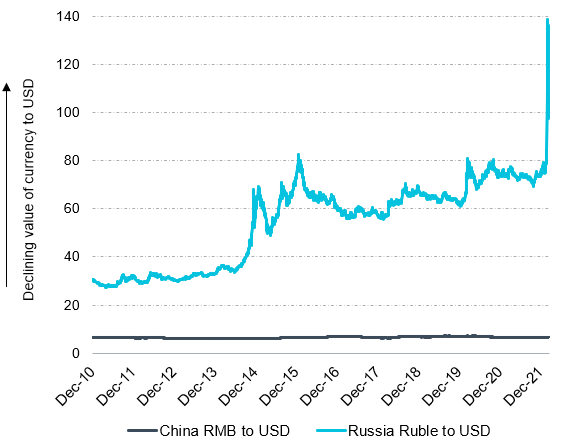

- Why would that be the case? Shown on the left-hand chart on the next page, you will see both the Russian ruble and Chinese renminbi compared with the U.S. dollar. In the analysis, a country’s currency line moving upward indicates weakness versus the U.S. dollar. As illustrated, this global currency regime has not been working for Russia in recent decades.

- Meanwhile, China’s “long game” of executing on its quasi-communist state-led model within a global “western” framework has been working thanks to what has been a remarkably stable currency. But now China’s relationship with the U.S. and the West now suddenly comes into question with what appears as a cohesive go-forward relationship with Russia.

The Best and Worst Of Times From an FX Perspective

As of February 22, 2022

Past performance is not a reliable indicator of future performance.

Source: Bloomberg Finance L.P. All Rights Reserved.

Source: Encyclopedia Britannica. Due to the escalating events in Ukraine and Russia and the rapidly changing market environment, the current holdings and/or country exposure may be different.

Positioning—Overlying Message Is That Active Management Matters

- Global economic strength: The U.S. economy importantly comes into 2022 from a position of economic strength. This consideration matters with the Federal Reserve tightening monetary policy in a “front loaded” manner. If Fed Chairman Jerome Powell, for example, can achieve a “soft landing” for the U.S. economy even with tightening monetary policy, risk assets could be supported in such an environment.

- Consider the S&P 500, which in early March experienced a price “Death Cross” where its 50-day moving average moved downward through its 200-day moving average. While acknowledging that such a Death Cross can sometimes represent an ominous sign for markets, it can also represent an attractive entry point for risk assets if a soft landing is the ultimate destination for the U.S. economy after the Fed ends its current tightening campaign.

- Ultimately, watching for a soft landing for the U.S. economy is an important indicator for risk assets going forward.

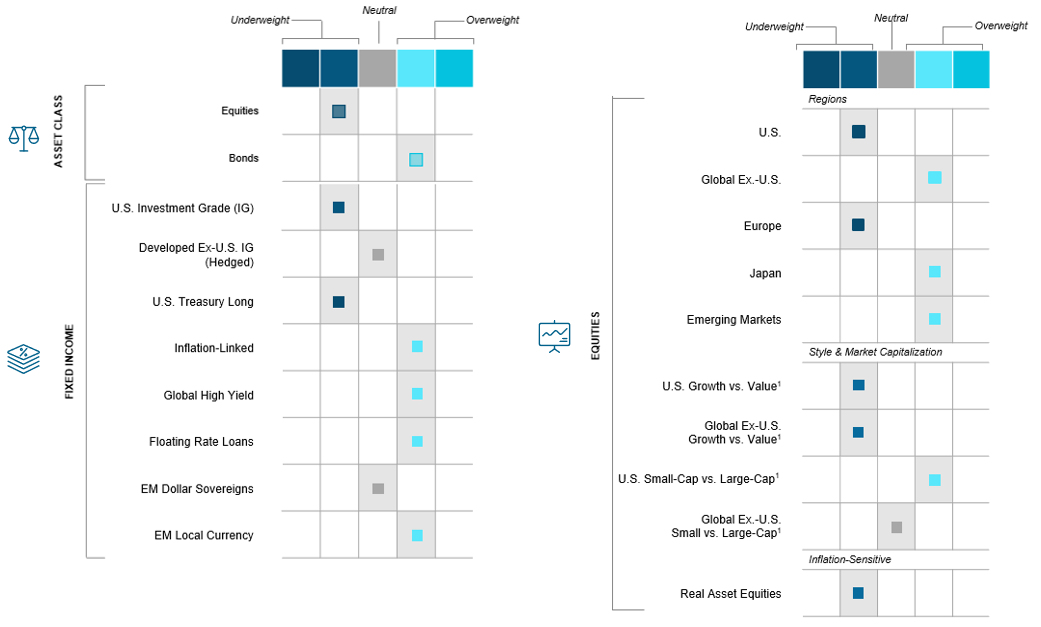

- Positioning considerations for T. Rowe Price Multi-Asset (MAS) in representative strategies:

- Against the backdrop of policy fade, MAS moved to underweight stocks this time last year and added to that underweight as 2021 ended. As last year concluded, markets had become earnings-driven and earnings growth faced headwinds off tough comps, margin pressure, and a Fed in play.

- Assessing the environment relative to the crisis in Ukraine and how far the Fed goes with its tightening campaign relative to the resiliency of the domestic and global economy all factor into positioning considerations this year.

- Some things to think about “tactical” positioning include:

- Short duration, emphasizing plus sectors, but with the highest conviction in the floating rate bank loan sector.

- Absolute return fixed income featuring active duration management and low to negative correlation to equities has worked well from a year-to-date perspective.

- Limited duration inflation protected bonds have also worked well in this current environment of heightened inflation.

- From an equity perspective, MAS migrated to a global overweight to value in the summer of 2020 that has worked well but may now need to be revisited. Looking ahead, if a “soft economic landing” is a destination, then the division’s overweight to the small- to mid-cap space appears even more prudent. And to the extent that some relief to the crisis in Ukraine unfolds in conjunction with global economic lift that could still come with the end to the pandemic, international equities remain of interest.

T. Rowe Price Multi-Asset Summary

T. Rowe Price Multi-Asset Positioning

As of February 22, 2022

1 For pairwise decisions in style and market capitalization, positioning within boxes represent positioning in the first mentioned asset class relative to the second asset class. This material is not intended to be investment advice or a recommendation to take any particular investment action.

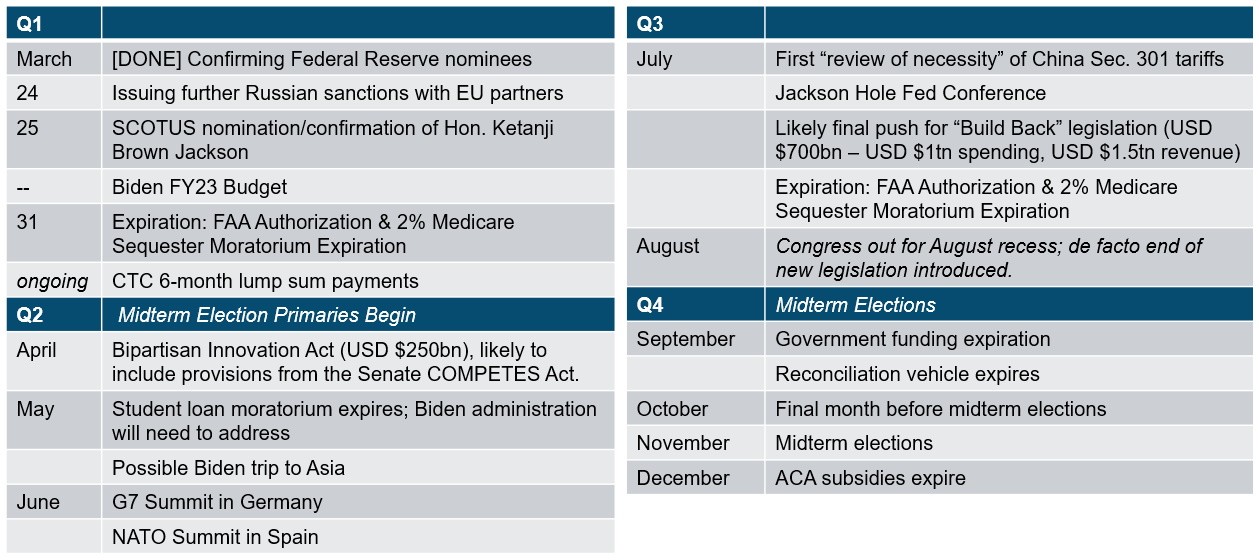

Policy Ties—Biden Administration Actions

- Looking back to when the Biden administration was first starting to transition into power before the inauguration, we were discussing what the core priorities the incoming administration would roll out:

- Most importantly, it was moving past the pandemic and the public health crisis and thinking more broadly about what the new economic future would be within the country.

- The administration was starting to pivot toward a new industrial economy and thinking through clean energy policy.

- It was revisiting some health care priorities that were long lasting and long-standing, specifically related to eldercare and other forms of social infrastructure.

- Fast-forward two years: The public health care emergency continues, but we are in the tail end of it. However, the situation in Ukraine completely disrupted the legislative and regulatory environment and the administration's focus on its preexisting goals leading into the midterm elections.

- The Biden administration is trying to turn the page and quickly tackle its domestic agenda before potentially facing a divided government next year.

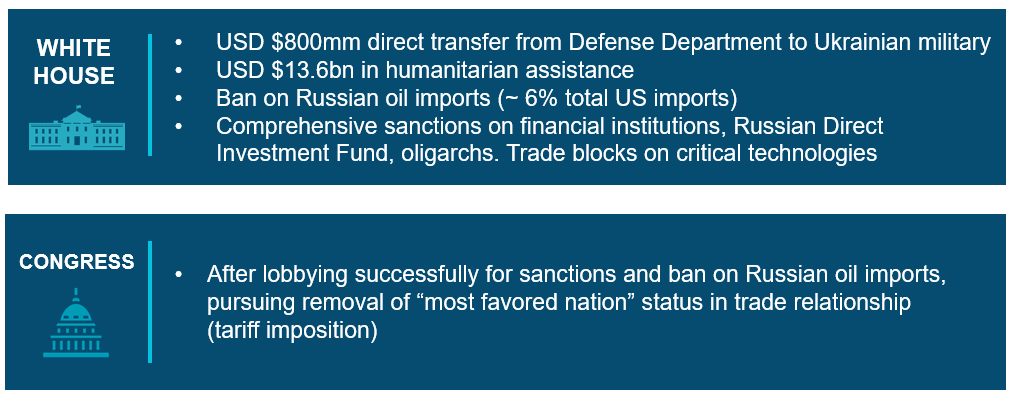

U.S. Actions Taken to Counter Russian Attacks on Ukraine

As of March 23, 2022

Due to the escalating events in Ukraine and Russia and the rapidly changing market environment, the current holdings and/or country exposure may be different.

Inflation and Timing

- There are many different bills on Capitol Hill that must be passed for actions to begin, but there are two compressing dynamics:

- Timing

- There are only so many legislative days available on the calendar to consider must-pass items such as: the defense budget, the federal budget, and the extension of ACA subsidies—all of which have concrete deadlines.

- We are now about the dynamics of timing as we look forward into the course of the year; considerable action is expected in July and August before the budget deadline of September 30.

- Inflation

- The Biden administration's legislative capacity, especially on the discretionary side, will be limited by inflation rates, which will also affect the political will of the Democratic Caucus.

- It will also affect the administration’s capacity to pass wide-sweeping legislation, such as the Build Back Better Act, which was negotiated over the better part of last year.

Timing and Inflation Will Put Pressure on Biden’s Legislative Agenda

As of March 23, 2022

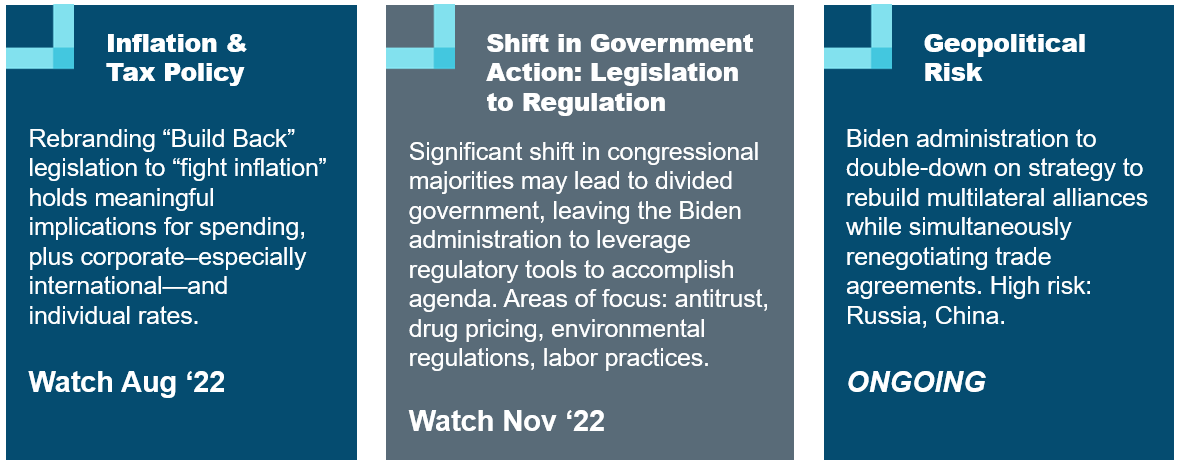

Themes to Monitor

- We are seeing the evolution of legislation turn into infrastructure as seen by the Build Americas Better Act. One of the core differences in messaging versus the Build Back Better Act is taking climate legislation and framing it as an industrial incentive to perform and to innovate while curbing inflation. That comes in the form of tax credits and revamping current government investment, including the addition of other technologies to PTC and ITC tax credits so that the United States is on the cutting edge of policy and technology.

- Something significant that should be kept in mind when thinking about portfolio positionings is the stickiness of tax reform provisions.

- Due to senatorial positioning, we aren’t going to see as much dilution in tax policy as if we were just operating along party line votes.

- What will the world look like if there is any type of shift in government power? If after the midterm elections we see a Republican majority in Congress, that could potentially block the legislative goals that President Biden has, specifically around spending.

- As a result, the administration may need to pivot to federal agencies for policy implementation with an area of focus on antitrust, drug pricing, environmental regulations, labor practices, and rulemaking. This is all going to play out in 2023 and 2024.

- With geopolitical risk, the Biden administration will have to “double down” on its NATO alliances in rebuilding the multilateral alliances we saw over the last four to five years.

- We also need to keep in mind what was happening in China before Russia invaded Ukraine. Most of the conversations to that point were about internal geopolitical concerns, specifically when it came to critical technology, risk to foreign investment, and intellectual property.

Themes to Monitor: 2022 to 2023

As of March 23, 2022

Final Remarks With Q&A

- Lack of progress for President Vladimir Putin in Ukraine: How are we thinking about the escalation of risk in Ukraine, and more broadly in Europe, potentially additional asset blocks or commodity bands?

- This is a fluid situation, but there is a need to assess the sheer scale of the agricultural commodity complex in Ukraine. A lack of fertilizer near term could be a catalyst for an entire growing season to get missed, which has longer-term implications that include a global food crisis. While North America can isolate itself from such a crisis to a large degree, the implications for a continent like Africa would be more dire.

- A vast commodity complex beyond Russian oil and gas that includes aluminum all the way to certain “noble” gases needed for semiconductor manufacturing could create a global supply chain issue at an already strained time due to the pandemic.

- As a result, the situation clouds our view of inflation becoming more dormant in the back half of this year with the pandemic becoming endemic, creating an entire new set of inflationary pressures off the conflict in Ukraine.

- From a positive perspective, Russia’s actions have galvanized the West where the G-7 just felt more like the G-zero in practical terms just a few months ago.

- Are we looking at a possible Cold War II or the end of globalization? While too soon to tell, instead of the end of globalization, a more nuanced outcome appears to be a go-forward reality where an “uneasy truce” continues to be defined between the U.S. and China.

- What are T. Rowe Price’s views on a possible recession? How are we thinking about it internally?

- As referenced during our discussion, T. Rowe Price is looking for a soft landing relative to the strength of the U.S. economy. With the strength of the U.S. economy and with the pandemic soon becoming endemic, a transition to the services side of the U.S. economy is not to be underestimated. We're assigning a low probability of recession in a soft landing, even though historical data may say otherwise, especially with a Fed tightening campaign.

- What are your views on the broader U.S. relationship with China, compared with six months ago?

- We are approaching a path toward strategic differences versus tactical differences with more stability and certainty in the relationship. Note that this possibly might be a better relationship but one that would offer more informational value.

- Former President Donald Trump's administration focused much more so on tactics rather than strategy when it came to China, while the Biden administration realized it can make strategic gains over time. Much policymaking progress is taking place behind the scenes of this administration, out of the public view. We do know there is an unsteady recognition between both governments that our trading relationship is too important and that our economies are too interwoven to completely decouple.

- Is China investible? There’s a matrix that needs to be navigated.

- Investors can't swim against the tide of Chinese regulatory policy.

- Chinese government policy is transparent in three areas:

- Financial stability

- Social stability

- National security

- China still needs trading partners to meet their goals, including the U.S., which ultimately means that large opportunities exist between the cracks that exist within its policies for active managers.

Important Information

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is no guarantee or a reliable indicator of future results.. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

USA—Issued in the USA by T. Rowe Price Associates, Inc., 100 East Pratt Street, Baltimore, MD, 21202, which is regulated by the U.S. Securities and Exchange Commission. For Institutional Investors only.

© 2024 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.