November 2021 / INVESTMENT INSIGHTS

Rising Inflation Risk and How to Address It

Inflation risk can be mitigated by using inflation-linked bonds, cyclical assets, and high-yielding bonds with low duration

Key Insights

- Sustained inflation has historically been a headwind for stocks and bonds, reducing the diversification benefits of holding both in a multi‑asset portfolio.

- Although markets appear to assume the current inflation spike is temporary, durable increases in housing costs and wages may challenge that view.

- Inflation risk can be mitigated by inflation‑linked sovereign bonds; cyclical stocks that keep up with inflation; and high‑yielding, low‑duration bonds.

For more than a decade, inflation has not been regarded as a major investment risk. Indeed, since the global financial crisis, deflation has been seen by many as a bigger threat—policymakers in Japan and the eurozone have been struggling to push inflation up, not down. With inflationary pressures now building across the world, though, this could change.

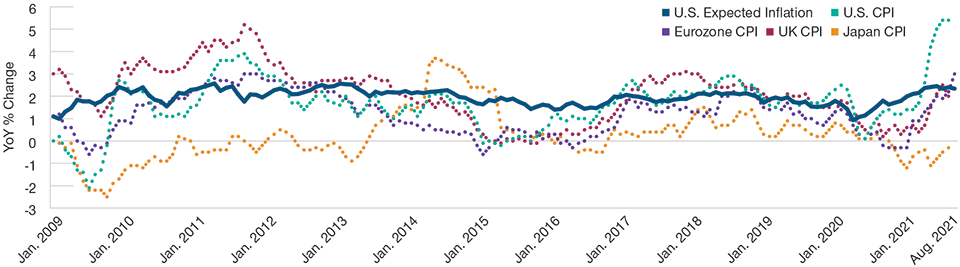

U.S. Inflation Expectations Are Anchored Despite CPI Spike

(Fig. 1) Recent realized inflation has been highly volatile

As of August 31, 2021.

Sources: U.S. CPI Urban Consumers YoY (U.S. Bureau of Labor Statistics), Euro Area MUICP All Items (Eurostat), UK CPI EU Harmonized YoY (UK Office for National Statistics), Japan CPI Nationwide YoY (Ministry of Internal Affairs and Communications), U.S. Breakeven 10 Year. Analysis by T. Rowe Price.

At present, the market‑implied 10‑year‑forward inflation expectation for the U.S. and most other developed countries remains relatively muted, reflecting widespread assumptions that the current inflation spike may prove temporary. Figure 1 shows the year‑on‑year (YoY) changes in consumer price indices (CPIs) for the U.S., the eurozone, the UK, and Japan as well as the market’s expected rate of inflation in the U.S. (10‑year breakeven inflation rate of inflation‑linked government bonds). It reveals that while inflation has recently spiked across the U.S., the eurozone, and the UK, expected inflation remains relatively anchored—and indeed has been more stable than realized monthly inflation for an extended period. In Japan, inflation is still in negative territory.

Sustained Inflation Would Challenge Markets

If inflation were to remain elevated for an extended period, it would pose a challenge for financial markets. Higher inflation typically brings higher interest rates, which cause bond markets to sell off. Significantly higher inflation has also depressed equity valuations in the past (Figure 2), a potential headwind for stocks. In an environment of persistent elevated inflation, higher positive correlations between stocks and bonds can diminish the diversification benefits of a multi‑asset portfolio.

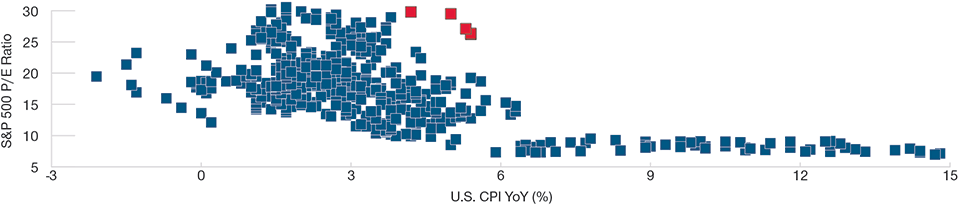

The Inflation Spike Has Not Depressed Equity Valuations—Yet

(Fig. 2) Historically, valuations have been suppressed when inflation hits 6%

As of August 31, 2021.

Past performance is not a reliable indicator of future performance.

The chart shows month‑end, YoY data from January 1978 through August 2021.

Sources: T. Rowe Price analysis using price earnings (P/Es) ratios (Standard & Poor’s) of the S&P 500 (see Additional Disclosure) and U.S. CPI Urban Consumers YoY (U.S. Bureau of Labor Statistics).

The red dots in Figure 2 show the five most recent relationships between U.S. inflation and the P/E ratio of the S&P 500 Index (at the end of April, May, June, July, and August 2021). They reveal that the recent inflation spike does not appear to have depressed equity valuations yet. This likely reflects the market’s expectation that inflation will prove transitory, which will allow the Federal Reserve to keep its policy rate lower for longer and avoid eroding real wage growth and corporate earnings.

We take a similar view: In our opinion, short‑term U.S. inflation will probably be higher than it has been over the past decade—but not high enough to be a major concern. Recent inflation prints have been heavily influenced by extreme price hikes in categories that experienced a sudden stop and restart due to the pandemic, such as used cars and travel. When we examine some of the drivers behind the spike in inflation in more detail, we believe these are likely to moderate in the near term.

For example, a key inflationary driver on the demand side has been the reopening of major economies following restrictions during the pandemic. Coupled with a rise in household savings, thanks to government support from employment replacement and furlough schemes (and limited opportunities to spend), this has unleashed a wave of pent‑up demand. However, the reopening is likely to only occur once: We do not anticipate that economies will close and reopen again, and we therefore believe that the current spending spree will wane with time.

Disruptions to supply chains due to COVID‑19 have also driven inflation higher. These include factories that are not yet producing at capacity, shortages of semiconductor chips, and rising freight and transportation costs. We believe these effects are also likely to be transitionary. As life returns to normal—or at least a version of normality—supply and production should return to something close to pre‑pandemic levels.

A third factor behind the inflation spike has been the base effect. Inflation is typically measured on a year‑on‑year basis—in other words, prices today are compared with prices a year ago. Last year, the world was engulfed by the worst of the pandemic. Demand and prices were depressed. It should be no surprise, then, that year‑on‑year changes in CPI are high when compared with such a low base. With time, inflation should be measured against the higher prices seen during the recovery period. Base effects are by their nature transitory.

Uncertainty Over Inflation Means Caution May Be Required

However, while the evidence suggests that the inflation spike is temporary, it is impossible to know this for certain. A more sustained period of accelerating prices cannot be ruled out. As such, we are closely monitoring housing costs—a significant component of consumer prices—and wage inflation. Housing costs have been rising steadily for the past decade, a trend heightened by increasing work‑from‑home arrangements.

Meanwhile, higher wages have historically led to price hikes as employers sought to offset rising labor costs. Durable increases in these two components could, in our view, generate more sustained inflation. Furthermore, logistic and supply bottlenecks may prove to be stubborn as vaccination rollouts differ across countries linked via global trade, for example, and some sectors may be slower to get back to full capacity than others.

As the saying goes, investors should hope for the best and prepare for the worst. Even if we hope for reasonable levels of inflation—not too low to be deflationary, not too high to become a headwind to investments—portfolios should include some protection against inflation. The key is to strike a balance between protecting against inflation and the cost or opportunity cost of such protection.

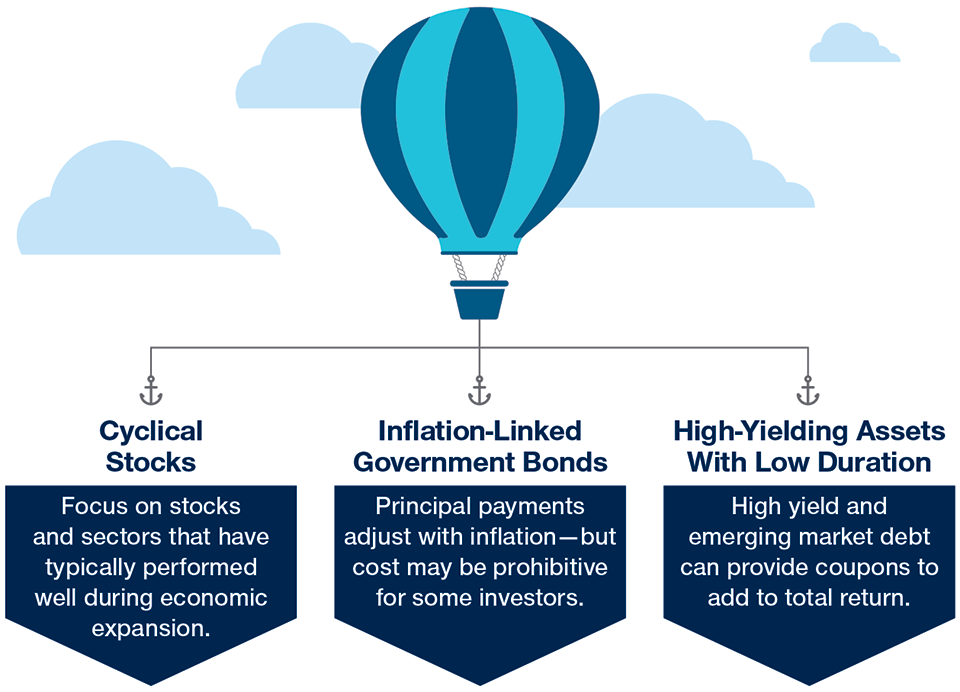

Three Ways to Mitigate Inflation Risk in Your Portfolio

Cyclical stocks, index‑linked bonds, and high yield assets can play a role

For Illustrative Purposes Only.

Three Ways to Help Protect Portfolios Against Inflation

Investors should consider ways to position their portfolios for persistent inflation. These may include:

- Purchasing inflation‑linked government bonds (ILBs). Designed to help investors to protect portfolios from inflation, ILBs are indexed to the price level so that the principal and interest payments rise and fall with the rate of inflation. One challenge with ILBs is their price, which is high in many markets. This means the after‑inflation yield they offer is low or negative, leading to potentially negative realized total returns in real terms. Moreover, ILBs should outperform standard nominal government bonds with a similar duration only if realized inflation is higher than the breakeven inflation rate (reflected in the difference between the yield of nominal bonds and ILBs). Now, breakeven rates are quite high, setting a high bar for ILBs to outperform as inflation must beat increased market expectations.

- Investing in cyclical stocks that are likely to perform well in an environment of rising prices. Inflation typically rises during periods of economic expansion, when cyclical assets tend to fare well. Examples of cyclical stocks include value stocks (partially due to the large financial sectors that should benefit from rising rates); small capitalization stocks (due to the economic expansion); and Japanese, European, and emerging market stocks (due to having export‑oriented economies that should benefit from a rebound in global trade).

- Buying high‑yielding assets with relatively low duration,1 such as global high yield bonds and emerging market debt. Higher yield means a greater cushion from collecting coupons to add to total returns. The two main caveats with such assets are (1) that they are correlated with equity markets, so they do not diversify equity risk, and (2) that they contain credit risk, meaning that credit analysis is required to mitigate losses.

The advantage of the second and third ideas discussed above is that they should likely perform well during periods of higher and lower inflation, not necessarily during periods of elevated inflation. In other words, they may provide some protection against inflation without an explicit cost in terms of foregone expected returns. Given that it is impossible to be certain about the level of inflation over the next few years, investment strategies such as these may prove particularly useful.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

November 2021 / DEFINED CONTRIBUTION

November 2021 / INVESTMENT INSIGHTS