November 2021 / FIXED INCOME

High Valuations Balance Healthy Credit in Global High Yield

Credit analysis can expose value even amid tight credit spreads

Key Insights

- Credit spreads on global high yield bonds are well below historical averages, but credit quality in the sector has probably never been better.

- With valuations looking fair, the Sector Strategy Advisory Group has a neutral tactical view of the overall sector.

- Our credit analysts are still finding attractive opportunities in individual credits through bottom-up fundamental analysis.

With U.S. Treasury yields mired at low levels and credit spreads1 on global high yield bonds2 well below historical averages as of late September, yields in the below investment-grade sector are at record lows. The flip side of these tight spreads is that credit quality in the broad global high yield market has probably never been better. With valuations looking fair, the Sector Strategy Advisory Group3 has a neutral tactical view of the overall sector. With that said, our credit analysts are still finding attractive opportunities in individual credits through bottom-up fundamental analysis.

Strengthening Credit Quality

Some general trends in the global high yield market since the onset of the pandemic have contributed to a strengthening of fundamental credit quality. The weakest credits defaulted during the peak of the crisis in 2020 and have left the market. At the same time, a flood of “fallen angels”—issuers downgraded from investment grade into the high yield universe—greatly increased the number of BB rated (the top rung of high yield ratings) credits in the market.

Credit quality in the sector is continuing to improve. Issuer leverage is falling as profitability recovers, and underwriting standards for new issues have been largely reasonable, in part due to a lack of aggressively structured leveraged buyouts (LBOs). Technical conditions in the market are also supportive as the search for yield in the ongoing low rate environment has buttressed demand for below investment-grade bonds, while new issuance has declined from its 2020 highs.

Easy Access to Liquidity

Also, issuers currently have easy access to liquidity by selling new bonds, borrowing from banks, or tapping the equity market through secondary stock offerings. Private credits can also sometimes obtain equity funding via a special purpose acquisition company (SPAC), which equity investors snapped up earlier in 2021. Many companies have used the proceeds from equity raises to pay down debt.

These credit-positive trends kept the default rate at unusually low levels after the initial pandemic-induced economic shutdowns. The U.S. high yield default rate (excluding the energy sector) was only 0.58% over the 12 months through August 31, 2021, compared with an average annual default rate since 2005 of 3.88%.4 Given the strong credit quality of the sector and robust economic growth, we anticipate that the default rate will remain near historic lows into 2022.

Tight Credit Spreads

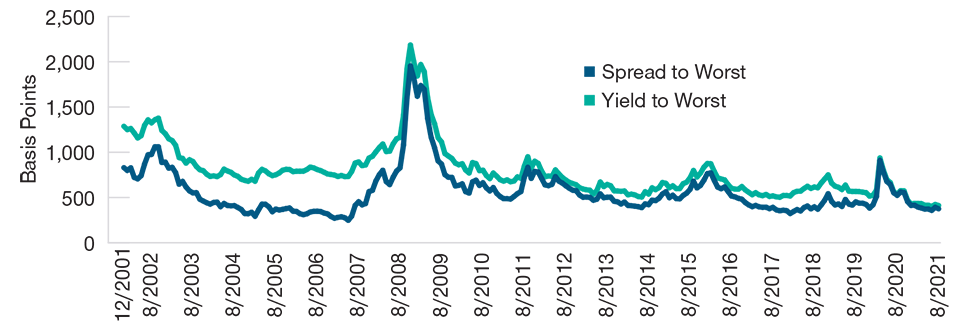

Credit spreads in global high yield are tight, which we believe is an accurate representation of the strong current credit quality in the sector. As of August 31, the spread on the ICE BofA Global High Yield Index was 375 basis points (bp) 5 versus the 10-year average of 505 bp. Combined with U.S. Treasury yields that are still near historic lows, this has pushed the yield on the index to near record-low levels: 4.12% as of August 31. Also, credit curves in the sector are unusually flat—investors gain an atypically small amount of additional spread by moving down in credit quality within the below investment-grade universe.

These broad trends—strong and improving overall credit quality accompanied by tight credit spreads—also generally apply for high yield markets outside the U.S. The European below investment-grade market typically provides some additional spread relative to the U.S., but that extra spread is currently smaller than usual.

We are also seeing low spread premiums to the U.S. in most below investment-grade emerging market regions—the notable exception being the Asian high yield market, which is experiencing high levels of volatility stemming from the Chinese government’s attempt to curb excessive leverage among certain Chinese property developers (notably China Evergrande). While this volatility has caused the bonds of many Asian high yield issuers to decline, we have seen opportunities to add to our favorite higher-quality Asian bonds at what we believe are attractive discounts.

Spreads and Yields Near Historical Lows

(Fig. 1) Spread and yield to worst,* global high yield bonds**

Past performance is not a reliable indicator of future performance.

As of August 31, 2021.

Source: ICE Data Indices, LLC (“ICE DATA”), is used with permission. ICE DATA, ITS AFFILIATES AND THEIR RESPECTIVE THIRD-PARTY SUPPLIERS DISCLAIM ANY AND ALL WARRANTIES AND REPRESENTATIONS, EXPRESS AND/OR IMPLIED, INCLUDING ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, INCLUDING THE INDICES, INDEX DATA AND ANY DATA INCLUDED IN, RELATED TO, OR DERIVED THEREFROM. NEITHER ICE DATA, ITS AFFILIATES NOR THEIR RESPECTIVE THIRD-PARTY SUPPLIERS SHALL BE SUBJECT TO ANY DAMAGES OR LIABILITY WITH RESPECT TO THE ADEQUACY, ACCURACY, TIMELINESS OR COMPLETENESS OF THE INDICES OR THE INDEX DATA OR ANY COMPONENT THEREOF, AND THE INDICES AND INDEX DATA AND ALL COMPONENTS THEREOF ARE PROVIDED ON AN “AS IS” BASIS AND YOUR USE IS AT YOUR OWN RISK. ICE DATA, ITS AFFILIATES AND THEIR RESPECTIVE THIRD-PARTY SUPPLIERS DO NOT SPONSOR, ENDORSE, OR RECOMMEND T. ROWE PRICE OR ANY OF ITS PRODUCTS OR SERVICES.

*The lowest possible credit spread and yield that can be realized on a bond that does not default.

**Represented by the ICE BofA Global High Yield Index.

High Volume of Potential Rising Stars

There is a large volume of high yield bonds with improving credit quality that could move into the investment-grade universe, where they would become “rising stars.” In U.S. high yield bonds, 9.5% of the Bloomberg U.S. High Yield Index was one rating move away from investment grade as of August 31 versus 7.0% at the end of 2019. A remarkable 23% of the U.S. index was two or fewer rating moves from investment grade, up from 15% on December 31, 2019.

This trend, which stems from both credit rating upgrades and fallen angels entering the market, illustrates how much the overall credit quality of the sector has improved. It should also provide technical support for global high yield by removing a large volume of bonds from the market as they receive upgrades and gain investment-grade ratings.

Global High Yield Carry Still Attractive

Although the narrow credit spreads limit the room for capital appreciation through spread compression, global high yield still offers attractive carry6 relative to other credit sectors—most of which are near their own record-tight spread levels. One global high yield segment where we do see some potential for spread tightening is credits that could soon become rising stars.

We rely heavily on our global team of high yield credit analysts to select credits that appear to represent attractive value relative to their credit quality. This bottom-up analysis and security selection drive any industry overweights or underweights. We are currently finding some opportunities in segments most affected by the pandemic, where concerns about the delta variant have pressured prices. These areas include airlines (particularly bonds backed by airline mileage programs), domestic gaming, and automotive. We also have a long-standing overweight to the cable industry—particularly in Europe—which has benefited from stable business models. We are cautious on energy-related credits despite the recent runup in commodities prices.

Bank Loans Attractive vs. High Yield Bonds

In many cases, we prefer to invest in bank loans over high yield bonds from the same issuer. Loans typically have below investment-grade credit ratings but are higher in the capital structure than bonds, giving them repayment priority in the event of default. Bank loan coupon payments adjust in line with changes in a benchmark short-term interest rate such as the three-month London interbank offered rate (LIBOR). This means that they have low duration.7 Many loans currently provide spreads comparable to—or even better than—bonds with similar credit quality. The combination of minimal interest rate risk, lower exposure to commodities prices, strong technical support, and relatively high carry makes bank loans attractive.

Potential Macro and Technical Risks

While we are confident in these select opportunities in global high yield debt, we are monitoring several potential risks that could cause a sell-off and credit spread widening. The delta variant could have a larger-than-anticipated impact on growth, likely dragging commodities prices lower (approximately 20% of the global high yield bond market is commodities-related) and weighing on the global economy in general. Pandemic-related fiscal stimulus is winding down, which will remove meaningful support from the bumpy economic recovery from the pandemic. Also, the new high yield issuance calendar for the fall looks busy, so the additional supply could create more challenging technical conditions in the global high yield market.

Barring a sharp increase in Treasury yields or a deep downturn in global growth, we anticipate that the ongoing search for yield will continue to support demand for global high yield bonds and bank loans.

Key Risks—The following risks are materially relevant to the strategy highlighted in this material:

Debt securities could suffer an adverse change in financial condition due to ratings downgrade or default, which may affect the value of an investment. Fixed income securities are subject to credit risk, liquidity risk, call risk, and interest rate risk. As interest rates rise, bond prices generally fall. Investments in high yield bonds involve greater risk of price volatility, illiquidity, and default than higher-rated debt securities. Investments in bank loans may at times become difficult to value and highly illiquid; they are subject to credit risk, such as nonpayment of principal or interest, and risks of bankruptcy and insolvency.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.