May 2021 / INVESTMENT INSIGHTS

What’s Next for Value Stocks

Value stocks have rallied, but we see the potential for more upside

Key Insights

- The U.S. economy appears poised for strong growth in 2021, but equity market valuations appear elevated.

- We, nonetheless, have a favorable outlook for the cyclical financials and energy sectors as well as attractively valued dividend payers.

- We remain focused on identifying companies whose intrinsic value may not be fully appreciated by markets.

The rotation from growth to value stocks accelerated in the first quarter of 2021. However, with valuations arguably reaching elevated levels in some areas, questions have emerged about the durability of the rally in cyclical industries and, if value stocks have more room to run, what the next leg higher might look like.

Much depends on the success of efforts to bring the coronavirus pandemic under control, in our view. Encouraging progress in vaccination programs, the sizable fiscal stimulus that the government has injected into the U.S. economy, and the potential for additional spending on infrastructure in the coming years create the potential for strong economic growth. The markets have noticed, with broader U.S. indexes reaching all-time highs in April. This march upward and our view of equity valuations lead us to believe that the broader market may generate somewhat muted returns in coming quarters.

Nevertheless, we are finding opportunities in select cyclical sectors, such as financials and energy, where we are attracted to quality companies that could benefit from a continuing recovery in the U.S. economy but also exhibit what we regard as a favorable valuation profile. The setup for attractively valued dividend payers also strikes us as favorable, given our view that elevated valuations could temper market returns and potentially burnish the appeal of stocks that offer a yield. Utility stocks, for example, sport above-market dividend yields, and we believe that the market does not fully appreciate the sector’s growth prospects stemming from the transition to renewable energy.

The Potential Next Phase of the Value Rally

The value stocks in the large-cap Russell 1000 Index outperformed their growth counterparts and the broader market in the first quarter of 2021, benefiting from the reversal of pandemic-driven economic and market dislocations that dominated the investment landscape last year. Chief among these developments were a rotation out of secular growers that investors bid up without regard to valuation and expectations that the combination of a return to normal activity and massive fiscal stimulus could unleash pent-up demand and drive earnings growth in cyclical industries.

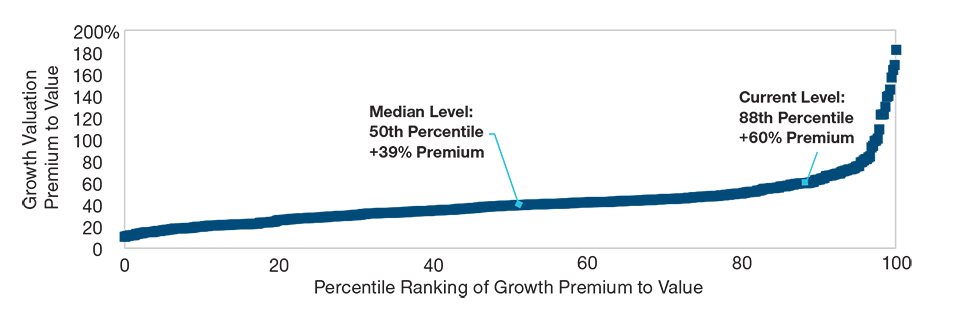

Value Stocks Could Have Room to Run

(Fig. 1) Percentiles of large-cap growth stocks’ valuation premium to value peers1

Based on historical data from December 31, 1978, to March 31, 2021.

Past performance is not a reliable indicator of future performance.

Source: T. Rowe Price analysis using data from Thomson Reuters and FactSet Research Systems Inc. Allrights reserved.

1 The weighted average 12-month forward price-to-earnings ratio for the Russell 1000 Growth Index divided by the same valuation metric for the Russell 1000 Value Index.

Although these excesses had moderated in the first quarter, the valuation premium at which the Russell 1000 Growth Index traded to the Russell 1000 Value Index remained elevated at the end of March 2021, suggesting that this differential may have room to narrow further via a rotation out of growth stocks and possible multiple expansion on the value side.

Against a backdrop of a potentially strong economic expansion, we see the possibility for some cyclical sectors, especially those where valuations still appear favorable, to fare well should earnings growth accelerate and multiples recover from the compression that occurred in recent years. This setup stands out against the broader market and growth equities, which we believe trade at levels that have priced in a good deal of upside, setting a high bar of expectations that corporate earnings would need to clear.

In our view, dividend-paying equities that land in the value style category—a group that has lagged in recent years but started to catch a bid in the first quarter—could also do well in an environment where the broader market’s muted performance prompts investors to shift their attention to stocks whose return propositions include a yield component. Rising interest rates and inflationary pressures can erode a dividend’s future value, but we note that rates remain low on a historical basis and believe that our tilt toward cyclical companies could help offset this headwind. In this environment, we see the potential for income-focused investors to gravitate toward dividend-paying equities because of the low yields available in the bond market.

Where We’re Finding Opportunities

Energy and financials were the leading performers in the S&P 500 Index in the first quarter, but we believe that these cyclical sectors could still offer compelling risk/reward profiles for discerning value investors.

Usually during downturns, cyclical stocks experience an increase in their price-to-earnings ratios because of the decline in profits that accompanies an economic contraction. Both the energy and financials sectors suffered from shrinking valuation multiples last year while their earnings came under pressure from the pandemic-driven disruptions. We believe this extreme dislocation indicated how out of favor financials had become after a prolonged period of middling economic growth and low interest rates. In the energy sector, depressed valuations likely stemmed from familiar culprits: concerns about the declining cost of incremental oil and gas production and the terminal values of hydrocarbon assets as the transition to clean energy gains steam.

Coming from such low levels, valuations in both sectors still appear attractive to us. And we see the potential for companies’ earnings and cash flows to surprise to the upside if economic growth accelerates, interest rates rise, and inflationary pressures emerge. Such a scenario could set the stage for valuation multiples to improve. Of course, our financials and energy holdings also offer exposure to potential upside catalysts that are specific to each company, which gives us a measure of confidence if these macro tailwinds do not play out as we expect.

In the financials sector, we hold banks where we believe cost reductions and other company-specific drivers could unlock value for shareholders regardless of the direction of interest rates and loan demand. Some banks may have the potential to increase their dividends or step up their share buybacks as they release capital that had been reserved against possible credit losses. We also like the risk/reward profiles offered by select property and casualty (P&C) insurers, a group that has lagged a bit during the recovery rally because of its reputation as a somewhat defensive industry. Here, we think that the market does not fully understand the potential multiyear boost in P&C insurers’ cash flows that could come from price increases and tighter underwriting standards.

We are keenly aware of the long-term challenges that the energy sector faces because of concerns about climate change and efforts to reduce carbon emissions. At the same time, we take a somewhat more constructive view of the energy sector because prevailing valuations do not appear to reflect the potential that the oil price environment could prove more supportive in the coming years—if labor and capital constraints instill greater discipline on the supply side. Among oil and gas producers, we favor high-quality operators with strong balance sheets, capable management teams, and assets that we believe are lower on the cost curve.

We are also finding opportunities outside of cyclical companies as relative valuations in defensive industries become more attractive. For example, the utility sector has lagged during the recovery rally amid concerns about rising interest rates. Many utilities feature appealing dividend yields. What’s more, some are well positioned to grow their rate bases1 through capital investments related to the clean energy transition and efforts to improve system resilience.

Although we continue to favor cyclical names in the current environment, our valuation discipline and in-depth research into industries and individual companies remain our guides as we seek to take advantage of near-term market dislocations and evolving risk/reward profiles.

What We're Watching Next

The search for attractively valued companies that offer decent yields has drawn our attention to the pharmaceutical industry, where we are monitoring the potential for regulatory and legislative developments to address concerns about rising health care costs. Depending on the shape of these initiatives, pharmaceutical companies could make up some of their price concessions on the consequent increase in volumes that would accompany improvements to health care affordability and access.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

May 2021 / GOING BEYOND THE NUMBERS