A Diversified Approach to Tail-Risk Mitigation

Executive Summary

- Investors often seek to manage exposure to tail risk using options and other financial products. However, the costs can overwhelm the potential benefits.

- T. Rowe Price offers a diversified risk‑mitigation strategy that seeks to balance effective hedging against tail risk with durable long‑term performance.

- Our framework incorporates a number of complementary strategies, each with their own performance characteristics inside and outside of left‑tail outcomes.

Tail‑risk hedging, tail‑risk mitigation, downside protection, and drawdown protection are common terms that relate to the objective of limiting the “left tail” of a portfolio return distribution. Investors who fear left‑tail events often turn to specific financial products as remedies. These may include options, structured products, constant proportion portfolio insurance (CPPI), or customized protection from insurers and/or investment banks.

While these products may make sense for specific investors, in many other situations the costs (both direct and indirect) may overwhelm the potential hedging benefits, leading to poor investment results and investor disappointment.

As an alternative to these products, T. Rowe Price has developed a diversified tail‑risk mitigation framework that potentially can deliver the desired outcome of protecting against left‑tail events while simultaneously limiting the drag on portfolio performance in more normal investment environments. Our approach incorporates a number of complementary strategies, each with their own attributes and behaviors inside and outside of the left tail.

We begin this paper by categorizing tail‑risk mitigation strategies. After describing the components of our tail‑risk mitigation framework and our portfolio construction process, we present a case study that demonstrates how investors can align a tail‑risk mitigation strategy with their own specific risk tolerance and long‑run return objectives.

Categorizing Tail‑Risk Mitigation Strategies

We generally think of tail‑risk mitigation strategies as falling into one or more of four1 broad categories:

1. Structural: Structural strategies seek to reduce risk to the underlying assets with minimal basis risk—for example, by hedging an equity portfolio with a short equity futures position.

2. Proxy: Proxy strategies seek to reduce effective risk to the underlying assets by constructing long or short positions that are expected to be negatively correlated to the underlying assets (e.g., an equity portfolio hedged with a short emerging markets currency position).

3. Dynamic: Dynamic strategies seek to create empirical convexity to the underlying assets via dynamic trading (e.g., constant proportion portfolio insurance, managed volatility strategies).

4. Non‑Linear: Non-linear strategies seek to provide ex‑ante convexity to the underlying assets via use of options or other non‑linear instruments.

It is important to note that these categories are not mutually exclusive. For instance, a simple put option could fit the characteristics of categories 1, 2, and 4, all in one instrument.

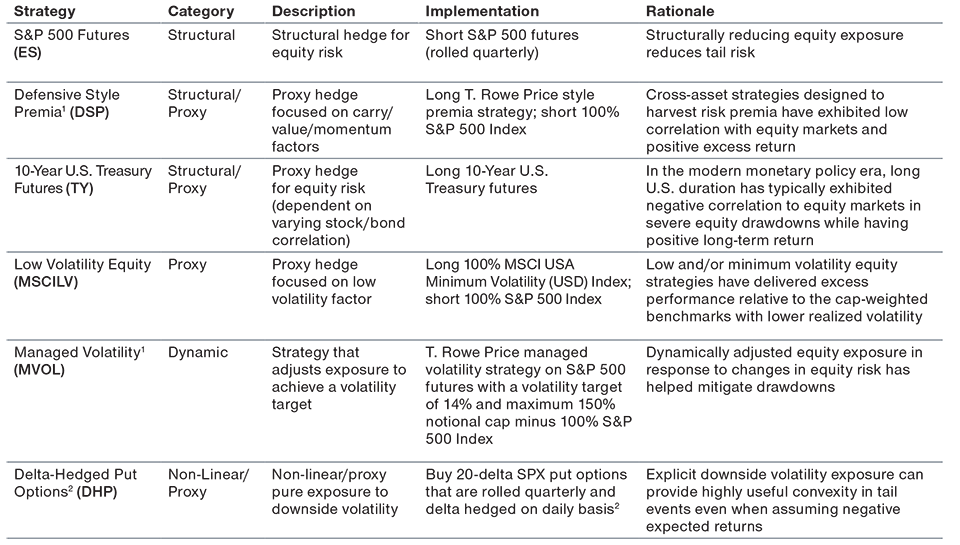

T. Rowe Price’s tail‑risk mitigation framework incorporates six strategies that have both theoretical and empirical properties that align with at least one of the categories above. Figure 1 provides a categorization of these six components, along with brief descriptions and the rationales for their inclusion in our framework.

Components of T. Rowe Price’s Tail-Risk Mitigation Framework

(Fig. 1) Descriptions and categorization

Source: T. Rowe Price.

1 Return series for DSP and MVOL are back test results of independent strategies managed by T. Rowe Price. See the important information on hypothetical portfolios at the end of this paper.

2A 20‑delta SPX put option would be expected to fall $0.20 for every dollar the S&P 500 Index rises and vice versa.

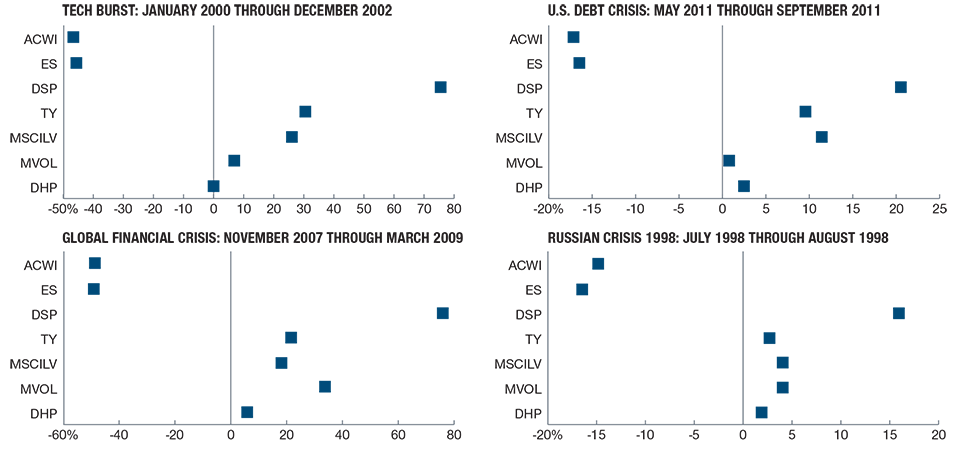

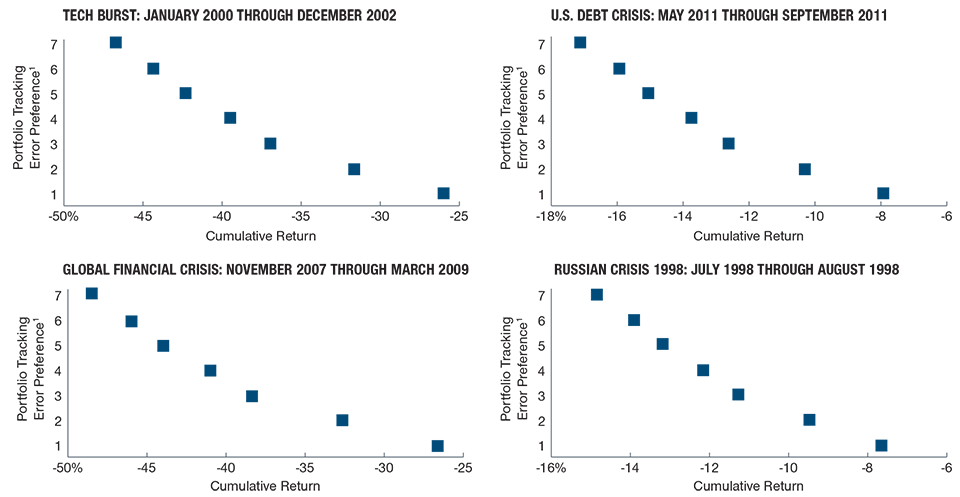

Tail‑Risk Mitigation Model Strategies

(Fig. 2) Hypothetical Performances in Historical Tail‑Risk Scenarios

Cumulative Returns for Periods Shown1

This chart contains hypothetical analysis, which is shown for illustrative purposes only and is not indicative of realized past or future performance. See the important information on hypothetical portfolios at the end of this paper.

Sources: Citi, Standard & Poor’s, MSCI (see Additional Disclosures), and T. Rowe Price; data analysis by T. Rowe Price.

Source for Bloomberg Barclays index data: Bloomberg Index Services, Ltd (see Additional Disclosures).

1 Figures are calculated in U.S. dollars.

Historical Performance in Tail‑Risk Scenarios

We examined potential hypothetical performance by each of the six strategies in our tail‑risk mitigation framework across a range of historical left‑tail regimes, including the 1998 Russian debt default, the bursting of the technology bubble of the late 1990s, the 2007–2009 global financial crisis, and 2011 concerns about the U.S. federal debt limit.

The performance results shown in Figure 2 might lead an investor to conclude that any one of the component strategies in our framework would be sufficient to mitigate tail‑risk. But what is not shown in Figure 2 are the return profiles of the component strategies in periods “outside the tail.”

Investing is a multi‑period problem, not a one‑period problem. In the case of option‑based strategies (a common approach to tail‑risk hedging), repeated net purchases of options can result in a significant negative return drag even when left‑tail events are encountered.

For example, suppose an investor seeking left‑tail mitigation pursued a simple long option strategy that purchased 3½ month 20‑delta S&P 500 put options and rolled those positions on the last day of the month before expiration. Over a period beginning January 1, 1998, and ending February 29, 2020, the hypothetical annualized return on that strategy would have been ‑2.5%.2 About 125 basis points (bps) of the performance drag would have been due to the structural 20% short equity position associated with a 20‑delta put option, but the remainder reflected a combination of the variance risk premium and the horizon, roll, and strike choices associated with the option.3

Buy‑and‑hold option positions require an investor to make specific choices on time horizon, roll, and strike, which all lead to path dependency in the investment process. Because drawdowns and tail‑events unfold over a wide variety of time horizons, we believe that effective tail‑risk mitigation should not rely on good timing—or luck.

...we believe that effective tail‑risk mitigation should not rely on good timing—or luck.

...we believe that effective tail‑risk mitigation should not rely on good timing—or luck.

Constructing a Tail‑Risk Mitigation Model

Our tail‑risk mitigation framework uses a multi‑step portfolio construction process that emphasizes the potential risk‑and‑return characteristics of each component strategy during tail events. While we consider performance behavior during historical tail events, our portfolio construction process relies on forward‑looking assumptions for each strategy component.4

For example, the annualized return over cash of 10‑year U.S. Treasury futures from January 1, 1998, through May 31, 2019, was 3.61%. However, as of January 31, 2020, the 10‑year U.S. Treasury note was yielding just 1.51%. This means that designing a tail‑risk mitigation portfolio based on historical 10‑year U.S. Treasury futures performance would result in a materially different allocation than an approach that used what we believe is a more reasonable forward‑looking return assumption—which, in the case of our model, is a 1.00% annual return over cash.

There are five steps in our portfolio construction process:

- Step 1: Determine the unconditional equilibrium return, risk, and Sharpe ratio assumptions for the initial portfolio and tail‑risk mitigation strategies for an investor with no specific tail‑risk preferences;

- Step 2: Estimate a new covariance matrix that better captures risk and correlations in tail scenarios (note that we deliberately avoid estimating skewness, kurtosis, etc. or directly optimizing on historical returns);5

- Step 3: Based on the Sharpe ratios from Step 1 and the “tail” covariance matrix from Step 2, determine the equilibrium “tail” return assumptions;

- Step 4: Using an implementation of the Black‑Litterman model, blend forward‑looking views on the underlying and tail‑risk mitigation strategies with the “tail” equilibrium assumptions;6 and

- Step 5: Using the “tail” covariance matrix from Step 2 and blended return assumptions from Step 4, calculate the mean variance optimal (MVO) portfolio after applying an additional penalty to account for client tracking‑error preferences.

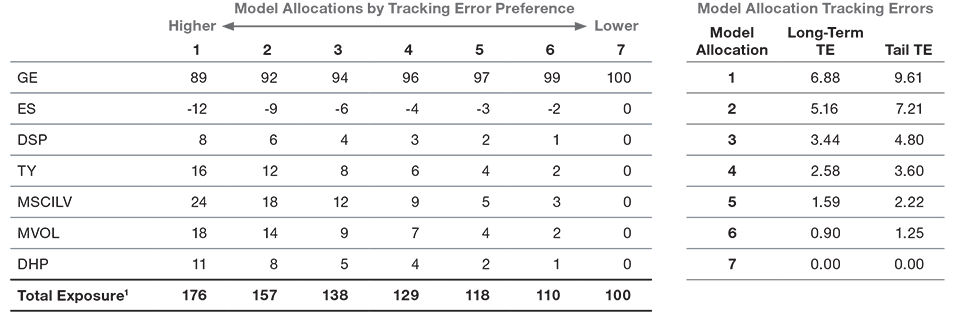

Our portfolio construction framework is designed to be flexible and can accommodate a wide range of portfolio designs and targeted tracking error profiles. To demonstrate this flexibility, we offer a case study for a hypothetical global equity portfolio.

Case Study: MSCI ACWI

We assume that the hypothetical investor in our case study is interested in a tail‑risk mitigation solution for an U.S. dollar-denominated global equity (GE) allocation, which is represented by the MSCI ACWI. Using our portfolio construction model, we designed seven model allocations across a range of tracking error targets. Model seven is a simple unhedged global equity portfolio, represented by the MSCI ACWI.

Figure 3 presents the range of model allocations for the six component strategies in our tail‑risk mitigation framework and the unhedged global equity portfolio, sorted by their forecasted tracking error. Allocation one has the highest exposure and tracking error, while allocation seven, which does not include any tail‑risk strategy exposure, has no expected tracking error. Our framework is designed to customize the tracking error (and accompanying notional exposure) to investor preferences.

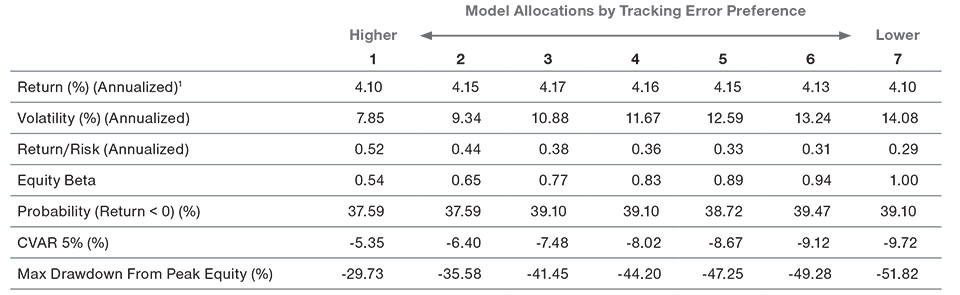

Figure 4 summarizes the results of a historical back test of the allocations shown in Figure 3. The annualized return on the underlying global equity allocation could have been only modestly impacted by the tail‑risk mitigation allocations, but the volatility of those allocations and the associated performance statistics—such as the maximum drawdown and the conditional value at risk (CVAR)—could have materially improved as notional exposure to the strategies increased. Cumulative returns in the four historical tail-risk scenarios we examined also could have been improved significantly (Figure 5).

As previously discussed, our portfolio construction methodology incorporates forward-looking assumptions for the component tail‑mitigation strategies in our framework given what we believe is the inappropriateness of optimizing based on historical returns. In anticipation of investor curiosity regarding the performance of the tail‑risk mitigation strategies based on forward‑looking return assumptions, Figure 6 offers two additional scenario analyses:

- Scenario 1 blends historical returns for the MSCI ACWI with our forward‑looking return assumptions for the tail‑risk mitigation strategies.

- Scenario 2 combines our capital market assumption for global equity (as represented by the MSCI ACWI) with our forward‑looking return assumptions for the tail‑risk mitigation strategies.

Because our return assumptions are more modest than the historic averages, the results shown in Figure 6 present a more “intuitive” risk/return trade-off (in the sense that return is not fully preserved) as notional exposure to the tail-risk strategies increases. Yet, we see demonstrable potential improvement in risk-adjusted returns using the tail-risk mitigation framework.

Customizing Tail‑Risk Mitigation Strategies to Investor Requirements

(Fig. 3) Global Equity Hedged Allocations (%) by Tracking Error Preference

January 1, 1998, through May 31, 2019.

This chart contains hypothetical analysis, which is shown for illustrative purposes only and is not indicative of realized past or future performance. See the important information on hypothetical portfolios at the end of this paper.

Sources: Standard & Poor’s, MSCI (see Additional Disclosures), and T. Rowe Price; data analysis by T. Rowe Price.

1Total exposure does not include potential netting.

Tail-Risk Mitigation Potentially Reduced Volatility Without Sacrificing Returns

(Fig. 4) Hypothetical Performance Statistics for Global Equity Model Allocations

January 1, 1998, through February 29, 2020.

This chart contains hypothetical analysis, which is shown for illustrative purposes only and is not indicative of realized past or future performance. See the important information on hypothetical portfolios at the end of this paper.

Sources: Standard & Poor’s, MSCI (see Additional Disclosures), and T. Rowe Price; data analysis by T. Rowe Price.

1 Returns calculated excess of cash.

Higher Tolerance for Tracking Error Could Have Improved Results

(Fig. 5) Potential Cumulative Returns for Model Allocations in Historical Tail-Risk Scenarios

Cumulative Returns for Periods Shown1

This chart contains hypothetical analysis, which is shown for illustrative purposes only and is not indicative of realized past or future performance. See the important information on hypothetical portfolios at the end of this paper.

Sources: Citi, Standard & Poor’s, MSCI (see Additional Disclosures), and T. Rowe Price; data analysis by T. Rowe Price.

1 Figures are calculated in U.S. dollars.

Sensitivity Analysis Finds More Intuitive Risk/Reward Trade-Off

(Fig. 6) Hypothetical Results Based on Historical and Forward‑Looking Assumptions

January 1, 1998, through February 29, 2020.

This chart contains hypothetical analysis, which is shown for illustrative purposes only and is not indicative of realized past or future performance. See the important information on hypothetical portfolios at the end of this paper.

Sources: Citi, Standard & Poor’s, MSCI (see Additional Disclosures), and T. Rowe Price; data analysis by T. Rowe Price.

Source for Bloomberg Barclays index data: Bloomberg Index Services Limited.

1 Returns calculated excess of cash. The indexes used for the 5-year capital market assumptions are global equity (the MSCI ACWI), 5.0%; global investment grade (BBgBarc Global Aggregate Bond Index), 1.9%; and cash (USD), 1.6%. See the Important Information about our capital market assumptions at the end of this paper.

Conclusions

Equity market returns are inherently difficult to predict. Tail‑risk hedging programs that rely on a single approach, such as option‑based strategies, are inherently inefficient given the inability of most investors to time the tail event. We believe the use of a multi‑strategy tail‑risk mitigation framework potentially can provide the tail‑risk management investors desire without sacrificing too much performance “outside the tail.”

Important Information—Capital Market Assumptions

T. Rowe Price Capital Market Assumptions: The information presented herein is shown for illustrative, informational purposes only. Forecasts are based on subjective estimates about market environments that may never occur. This material does not reflect the actual returns of any portfolio/strategy and does not guarantee future results. The historical returns used as a basis for this analysis are based on information gathered by T. Rowe Price and from third‑party sources and have not been independently verified. The asset classes referenced in our capital market assumptions are represented by broad‑based indices, which have been selected because they are well known and are easily recognizable by investors. Indices have limitations due to materially different characteristics from an actual investment portfolio in terms of security holdings, sector weightings, volatility, and asset allocation. Therefore, returns and volatility of a portfolio may differ from those of the index. Management fees, transaction costs, taxes, and potential expenses are not considered and would reduce returns. Expected returns for each asset class can be conditional on economic scenarios; in the event that a particular scenario comes to pass, actual returns could be significantly higher or lower than forecast.

Important Information—Hypothetical Portfolios

The information presented herein is hypothetical in nature and is shown for illustrative, informational purposes only. This material is not intended to forecast or predict future events, but rather to demonstrate T. Rowe Price’s capability to manage assets in this style. It does not reflect the actual returns of any portfolio/strategy and does not guarantee future results. Certain assumptions have been made for modeling purposes and are unlikely to be realized. No representation or warranty is made as to the reasonableness of the assumptions made or that all assumptions used in modeling analysis presented have been stated or fully considered. Changes in the assumptions may have a material impact on the information presented. Data shown for the sample portfolios are as of the dates shown and represent the manager’s analysis of sample portfolios as of that date and are subject to change over time. The sample portfolios do not reflect the impact that material economic, market, or other factors may have on weighting decisions. If the weightings change, results would be different. Management fees, transaction costs, taxes, potential expenses, and the effects of inflation are not considered and would reduce returns. Actual results experienced by clients may vary significantly from the hypothetical illustrations shown. The information is not intended as a recommendation to buy or sell any particular security, and there is no guarantee that results shown will be achieved.

The gross model performance results do not reflect the deduction of investment advisory fees. Returns shown would be lower when reduced by the advisory fees and any other expenses incurred in the management of an investment advisory account. For example, an account with an assumed growth rate of 10% would realize a net of fees annualized return of 8.91% after three years, assuming a 1% management fee.

1 There is a fifth category, which we call “explicit” hedging, where an investor would partner with an investment bank or insurance company to provide a customized explicit guarantee or floor on a custom portfolio. We do not consider these approaches in our framework.

2 Note that we did not include the performance of the underlying position in our analysis, only the returns on the options strategy.

3 The variance risk premium is the tendency for option‑implied volatility to trade above subsequent realized volatility.

4 Forward-looking return assumptions (all excess of cash and per annum) are as follows: for the underlying strategy: 100 bps outperformance of the benchmark, the Morgan Stanley Capital International All Country World Index (MSCI ACWI); for DSP, outperforming a short S&P 500 position by 100 bps; for TY, 100 bps; for MVOL, -50 bps; for MSCLIV, equal to return of the MSCI Minimum Volatility (USD) Index; for DHP, -75 bps; for ES, equal to the return of the S&P 500 Index.

5 Sébastien Page and Robert A. Panariello, When Diversification Fails, Financial Analysts Journal, Vol. 74, Issue 3, Third Quarter 2018.

6The Black‑Litterman asset allocation optimization model is described in Litterman, Robert B. Modern Investment Management: An Equilibrium Approach. Hoboken, N.J.: John Wiley, 2003.

Additional Disclosures

Copyright Citigroup 2005‑2020. All Rights Reserved.

Copyright © 2020, S&P Global Market Intelligence (and its affiliates, as applicable). Reproduction of any information, data or material, including ratings (“Content”) in any form is prohibited except with the prior written permission of the relevant party. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice. Credit ratings are statements of opinions and are not statements of fact.

MSCI and its affiliates and third party sources and providers (collectively, “MSCI”) makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI. Historical MSCI data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Important Information

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

Australia—Issued in Australia by T. Rowe Price Australia Limited (ABN: 13 620 668 895 and AFSL: 503741), Level 50, Governor Phillip Tower, 1 Farrer Place, Suite 50B, Sydney, NSW 2000, Australia. For Wholesale Clients only.

Canada—Issued in Canada by T. Rowe Price (Canada), Inc. T. Rowe Price (Canada), Inc.’s investment management services are only available to Accredited Investors as defined under National Instrument 45‑106. T. Rowe Price (Canada), Inc. enters into written delegation agreements with affiliates to provide investment management services.

DIFC—Issued in the Dubai International Financial Centre by T. Rowe Price International Ltd. This material is communicated on behalf of T. Rowe Price International Ltd. by its representative office which is regulated by the Dubai Financial Services Authority. For Professional Clients only.

EEA ex‑UK—Unless indicated otherwise this material is issued and approved by T. Rowe Price (Luxembourg) Management S.à r.l. 35 Boulevard du Prince Henri L‑1724 Luxembourg which is authorised and regulated by the Luxembourg Commission de Surveillance du Secteur Financier. For Professional Clients only.

Hong Kong—Issued by T. Rowe Price Hong Kong Limited, 6/F, Chater House, 8 Connaught Road Central, Hong Kong. T. Rowe Price Hong Kong Limited is licensed and regulated by the Securities & Futures Commission. For Professional Investors only.

New Zealand—Issued in New Zealand by T. Rowe Price Australia Limited (ABN: 13 620 668 895 and AFSL: 503741), Level 50, Governor Phillip Tower, 1 Farrer Place, Suite 50B, Sydney, NSW 2000, Australia. No Interests are offered to the public. Accordingly, the Interests may not, directly or indirectly, be offered, sold or delivered in New Zealand, nor may any offering document or advertisement in relation to any offer of the Interests be distributed in New Zealand, other than in circumstances where there is no contravention of the Financial Markets Conduct Act 2013.

Singapore—Issued in Singapore by T. Rowe Price Singapore Private Ltd., No. 501 Orchard Rd, #10‑02 Wheelock Place, Singapore 238880. T. Rowe Price Singapore Private Ltd. is licensed and regulated by the Monetary Authority of Singapore. For Institutional and Accredited Investors only.

Switzerland—Issued in Switzerland by T. Rowe Price (Switzerland) GmbH, Talstrasse 65, 6th Floor, 8001 Zurich, Switzerland. For Qualified Investors only.

UK—This material is issued and approved by T. Rowe Price International Ltd, 60 Queen Victoria Street, London, EC4N 4TZ which is authorised and regulated by the UK Financial Conduct Authority. For Professional Clients only.

USA—Issued in the USA by T. Rowe Price Associates, Inc., 100 East Pratt Street, Baltimore, MD, 21202, which is regulated by the U.S. Securities and Exchange Commission. For Institutional Investors only.

© 2020 T. Rowe Price. All rights reserved. T. Rowe Price, INVEST WITH CONFIDENCE, and the bighorn sheep design are, collectively and/or apart, trademarks or registered trademarks of T. Rowe Price Group, Inc.

ID0003058 (03/2020)

202003‑1110391