In Emerging Markets, Does it Pay to Worry about ESG Factors?

Executive Summary

- Emerging markets (EM) have made great progress in relation to environmental, social, and governance (ESG) considerations in recent years, with many companies today displaying ESG standards in line with global best practices.

- Yet there remains a general perception among investors that EM continue to suffer from an “ESG shortfall.”

- This presents opportunities for active investors to find mispriced companies where strong or improving ESG standards are underappreciated, thereby offering long‑term price improvement potential.

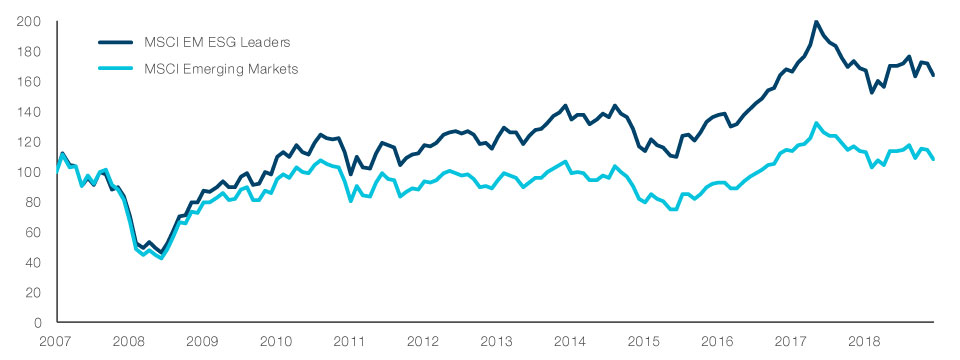

While environmental, social, and governance (ESG) investing has entered the mainstream in developed markets, these factors are still not as widely incorporated when investing in emerging markets (EM). However, while there are many EM companies that are still behind the curve in terms of ESG best practices, there are also many that are committed to improving or maintaining high ESG standards. And in answer to the question, “Does it pay to worry about ESG factors in EM?” we only need to look at the comparative long‑term value creation between those companies that do versus those that do not (Fig. 1).

FIGURE 1: Having an ESG Lens Has Delivered a Long-term Performance Advantage in EM

Cumulative Index Performance – Net Returns

30 Sept 2007 – 30 Sept 2019

Past performance is not a reliable indicator of future performance.

Sources: MSCI (see Additional Disclosure); data analysis by T. Rowe Price. Total Return Indices (Net Dividends), rebased to 100 in USD.

Ultimately, we make investment decisions based on financial considerations, however as part of our objective to make money for investors, we also consider ESG factors as part of our company analysis. We look to invest in businesses on the right side of change, and integration of ESG factors is an important part of our investment process.

There remains a general perception among investors of an “ESG shortfall” when it comes to EM. This broad‑brush view, in turn, presents good opportunities for active investors to identify mispriced stocks, where strong or improving ESG standards are being underappreciated. Our firm belief is that strong ESG standards are a clear and important influence on long‑term business sustainability.

Simply Being Cheap is Not Enough

As a value investor, incorporating ESG factors is a fundamentally important part of our investment framework. We look for forgotten companies where the long‑term value potential is either unrecognized or not fully understood. Simply being cheap is not reason enough for us to invest in a company. We also need to see clear potential for fundamental change. This could be the result of external factors, such as a change in government or a recovery in the economic cycle, or it can also be driven internally through cost‑cutting, new management, or restructuring of the business. Similarly, strong or improving ESG standards can also provide a positive impetus for stock price improvement. This is where the ESG theme fits closely with the value style of investing—both are about trying to achieve long‑term change.

1,135

Number of stocks listed on the MSCI Emerging Markets Index1 — a broad opportunity set, but where ESG standards vary significantly.

ESG Standards Within EMs Are Rapidly Improving

Given the general perception of weaker ESG standards within the emerging world, and the size of the universe, there are good opportunities to find underappreciated value in those companies with strong or improving ESG ratings. We continue to find many EM companies that display best practice standards when it comes to ESG factors—standards that are equal, or even superior, to developed market counterparts. And in certain cases, some EM companies do have good ESG standards, but they score poorly simply due to a lack of proper disclosure. Even among those EM countries and industries where ESG considerations are less progressed, there are many companies that are clearly committed to change and that understand the importance of ESG considerations for the long‑term sustainability of their businesses. Conversely, there are also companies that continue to ignore, or give little attention to, ESG considerations, particularly in the area of governance standards. Our experience tells us that these companies tend to be higher risk, as they will potentially experience higher costs, greater capex, and reduced profits over time, undermining any longer‑term value creation for investors.

Standards of corporate governance are particularly important because they essentially determine how a company is managed. While governance is perhaps the area where EM standards, in aggregate, lag developed markets the most, it is also the area where considerable progress has been made. More and more EM companies are focusing on increasing long‑term shareholder value, understanding that this is central to attracting capital, especially from foreign investors. Therefore, we always consider factors like how a company is allocating its capital, its management remuneration structure, the make‑up and independence of its board, and any acquisition/disposal plans. Ultimately, we need to feel comfortable that the management team is capable of running the business efficiently, profitably, and with the best long‑term interest of shareholders in mind.

In incorporating ESG factors as part of our analysis, we focus on the materiality of each, and the potential positive or negative impacts on a company’s long-term financial performance.

In incorporating ESG factors as part of our analysis, we focus on the materiality of each, and the potential positive or negative impacts on a company’s long-term financial performance.

Investors also need to be aware of different ownership dynamics that exist in EM. State ownership, for example, is more prevalent than in developed markets, and this can prove a hindrance to efficient management, as well as not aligning business objectives with the interests of minority shareholders. Family ownership of a listed company is also a more common occurrence in EM than it is in developed markets. Once again, these structures are often characterized by weak standards of governance. Company boards, for example, tend to be dominated by members of the controlling family, with no independent voice or input, meaning the interests of minority shareholders are generally poorly represented.

If we look at the social aspect of ESG, this includes all the key stakeholders of a business along its entire value chain—from suppliers to customers to staff—and even the regulatory bodies that it deals with. These key relationships are crucial to the operational efficiency of a company and, ultimately, to the long‑term sustainability of the business itself.

GAZPROM

From Value Trap to Value Creator

For a long time, the stock price of a Russian energy giant, Gazprom, effectively flatlined, stuck within a narrow range over an extended multi‑year period, and little value created for investors.

Given Gazprom’s large weighting within the MSCI Emerging Markets Index, and the relative cheapness of its share price, we had monitored the stock for some time. However, despite the deep value seemingly on offer, it looked and behaved like a classic “value trap” company.

As recently as the start of 2019, Gazprom was among the very cheapest stocks in the EM investment universe, on a price‑to‑book ratio basis, yet we continued to avoid the company as we could not identify a thesis for fundamental change. The company’s management were seemingly unable, or unwilling, to implement the kind of reforms needed to improve the business and so create value for investors.

However, the landscape shifted in the early months of 2019, with the announcement of a change in management at the company. A number of long‑serving, senior personnel were relieved of their positions, replaced by younger, more progressive, executives. The new management team announced plans to allocate capital more effectively and generally improve the overall efficiency of the business. This change in management, and early signs of a commitment to reform, signaled the type of fundamental, potentially value‑creating, change that we look for in forgotten or unloved businesses.

The company’s new management team appears willing to prioritize improved returns for shareholders. In mid‑May, Gazprom announced that it will pay out a record dividend of around 8.5% to its shareholders in 2019—equating to roughly 30% of the company’s total net income. What’s more, market expectations are for the company to increase this payout ratio further, to around 50% in the coming years.

This shift in strategy, placing a greater focus on shareholder returns, had an almost immediate impact on Gazprom’s share price, which rose by more than 35% since the dividend hike was announced in May 2019.2 This change in policy—should it be fully implemented—is encouraging and came at a time when the company had largely been forgotten by investors.

While the signs appear positive so far, it is still too early to determine whether this reflects a real and sustainable change in Gazprom’s business. As such, we continue to monitor its progress closely.

ESG Factors and the Avoidance of “Value Traps”

In incorporating ESG factors as part of our analysis, we focus on the materiality of each and the potential positive or negative impacts on a company’s long‑term financial performance. For example, a company’s selling practices, its use of fossil fuels, its employee relations track record—these are just some of the material ESG‑related factors that can, in turn, impact operational areas such as pricing power, market share, operating costs, employee retention, and productivity. As a value investor in EM, specifically, these considerations are particularly important as there are many companies that appear very cheap and to have solid long-term upside potential based on traditional financial factor analysis alone. However, by also including analysis of nonfinancial ESG factors, it soon becomes clear that many of these companies are cheap for good reason. With little attention given, or commitment made, to improving ESG standards, these “value traps” in EM are likely to remain cheap for a very long time.

While potential value traps are prevalent in EM, it is not always appropriate to assume the worst. Rather than poor underlying practices and procedures, it can often be a matter of disclosure, with management not really understanding why these factors are of such interest to investors or how they can be most effectively reported on. Indeed, our experience is that there is an increasing appetite for engagement among EM companies and a willingness to learn about many of these important issues—a keenness that is sometimes stronger than that exhibited by their developed market counterparts.

Harnessing ESG Insights

From an investment perspective, while we have long incorporated ESG factor analysis as part of our investment decision‑making process, the quality and consistency of this analysis has been greatly enhanced in recent years with the addition of a dedicated, in‑house responsible investment research team at T. Rowe Price.

Particularly within EM, where ESG research can be inconsistent and much of the third‑party data available are outdated or backward‑looking, being able to draw upon timely ESG analysis where factor materiality is the primary focus adds an important and differentiated component to our investment decision‑making.

1 Source: MSCI (see Additional Disclosure), as at August 31, 2019.

2 Source: Thompson Reuters, © 2019 Refinitiv. All rights reserved. As of September 30, 2019. Data analysis by T. Rowe Price. For the period May 13, 2019 to September 30, 2019. The company announced it would pay an increased dividend on May 14, 2019.

Additional Disclosure

FIGURE 1. MSCI and its affiliates and third party sources and providers (collectively, “MSCI”) makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI. Historical MSCI data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Important Information

The specific securities identified and described are for informational purposes only and do not represent all of the securities purchased, sold or recommended for the portfolio, and no assumptions should be made that the securities were or will be profitable.

This material is being furnished for general informational purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, and prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction. Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

201910-971902