December 2022 / MARKET OUTLOOK

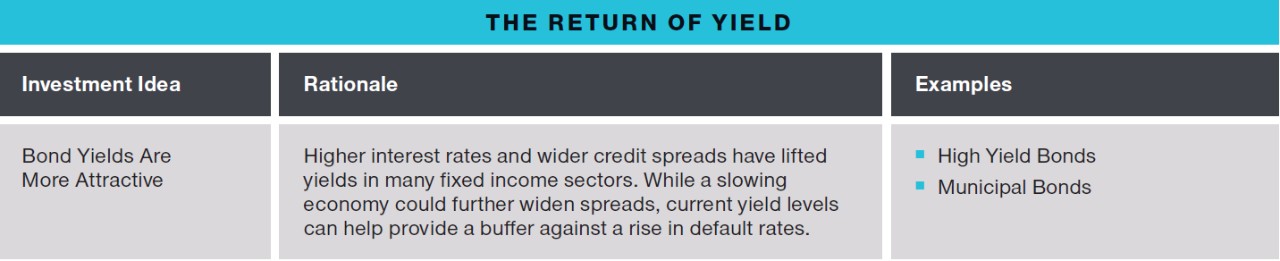

The Return of Yield

Yields are appealing in select markets and buying opportunities exist, but investors will need to be mindful about volatility.

A brutal year for bond markets in 2022 ended with a silver lining for investors: It raised fixed income yields to some of the most attractive levels seen since the global financial crisis.

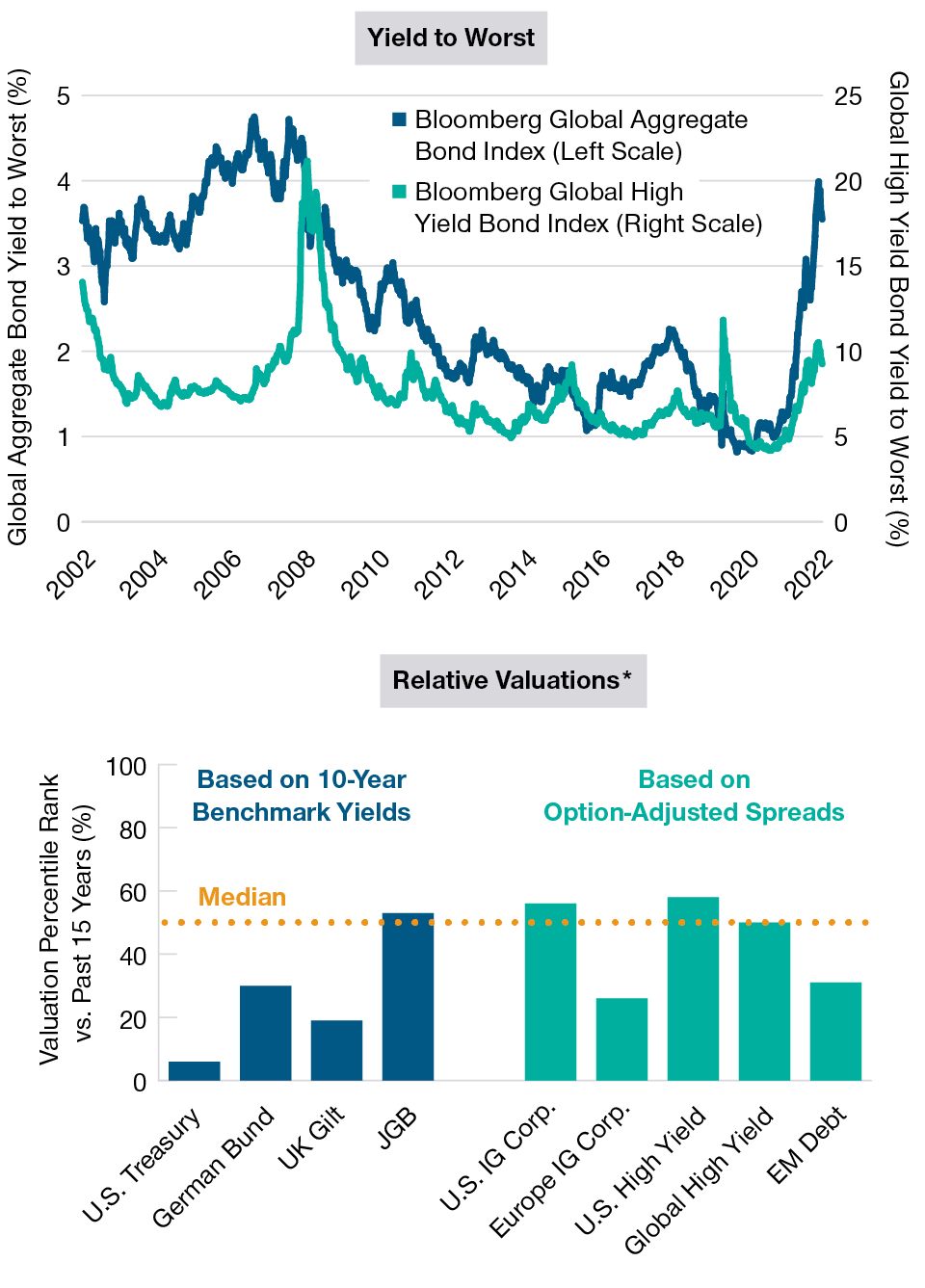

Higher yields (Figure 4, left) were mirrored in greatly improved valuations for both sovereigns and private credits, with many sectors selling close to or below their 15‑year historical medians as of late November (Figure 4, right).

Higher‑quality credits in the mortgage‑ backed and asset‑backed sectors also are attracting inflows from investors looking to put cash to work or extend duration (a measure of interest rate sensitivity), McCormick adds.

The Bond Bear Market Has Improved Both Yields and Relative Valuations

(Fig. 4) Yields on Aggregate Bond and High Yield Indexes; Fixed Income Valuations vs. Historical Averages

Past performance is not a reliable indicator of future performance.

Yields as of November 25, 2022. Valuations as of November 30, 2022. Subject to change.

*U.S. Treasury = 10‑Year Note, German Bund = 10‑Year Bund, UK = 10‑Year Gilt, JGB = 10‑Year Japanese Government Bond, U.S. IG Corp.= Bloomberg U.S.

Investment Grade Corporate Index, Europe IG Corp. = Bloomberg EuroAggregate Credit Index, U.S. High Yield = Bloomberg U.S. Aggregate Credit–Corporate High

Yield Index, Global High Yield = Bloomberg Global High Yield Index, Emerging Markets Debt = Bloomberg Emerging Markets USD Aggregate Index.

Sources: Bloomberg Financial L.P. and Bloomberg Index Services Limited (see Additional Disclosures). T. Rowe Price analysis using data from FactSet Research

Systems Inc. All rights reserved.

“This is the first opportunity try to lock in high‑single‑digit yields in over a decade,” McCormick says. “Anytime there’s been a glimmer that the Fed might be ready to slow its pace, or that inflation might have peaked, we’ve seen money find its way into the market.”

High yield bonds could offer particularly attractive return opportunities in 2023, McCormick and Page both say. Page cites three potential positives:

- Credit spreads—the yield difference between private credits and comparable U.S. Treasury maturities— have widened while default rates have remained relatively low.

- Corporate balance sheets generally are in strong shape.

- Energy accounts for a smaller share of U.S. high yield debt than in the past helping reduce default sensitivity.

Default rates almost certainly will rise if the U.S. economy slips into recession, Page acknowledges. But it would take a substantial leap to offset the return advantage built into current spreads. “If we get anything outside of a deep recession, the valuation case for U.S. high yield appears pretty strong,” he argues.

As of late November, McCormick adds, T. Rowe Price credit analysts estimated that U.S. default rates could rise to slightly under 3% for high yield bonds and just over 3% for floating rate bank loans in 2023, significantly less than current credit spreads. This forecast assumes that the U.S. economy passes through a mild recession, McCormick adds.

The outlook for European high yield is more guarded, McCormick cautions. While yields also have improved in those markets, the value proposition is less compelling because of the economic backdrop, he says.

Illiquid Markets Could Be Volatile

Market liquidity deteriorated in 2022 as monetary tightening accelerated, McCormick notes. As central banks shrink their balance sheets in 2023, new buyers will be needed. But stricter capital rules put in place after the global financial crisis have made it harder for bond dealers to function as liquidity providers.

“We’ve already seen bouts of illiquidity in some high‑quality markets, like UK gilts and U.S. Treasuries,” McCormick notes. “We believe the risk of further episodes remains elevated.”

But poor liquidity and price volatility also can create opportunities for longer‑term investors, McCormick notes. The U.S. municipal bond market, for example, experienced several months of outflows in late 2022 as investors harvested tax losses and repositioned for higher rates.

Credit conditions in the muni market appear strong, McCormick says. State and city governments received federal support during the pandemic shutdown, he notes, and saw tax revenues rise when businesses reopened. Given these fundamentals, muni yields and spreads remained attractive by most historical standards as of late November, which was attracting buyers back to the market.

Diversification in an Inflationary World

Higher volatility also has big implications for portfolio construction, Page says. But the key issue is the source of that volatility and its impact on asset correlations.

Historically, Page says, returns on stocks and on U.S. Treasuries have tended to move in the same direction when worries about inflation and interest rates have been high—as they were in 2022. This can destroy the diversification benefits of Treasuries.

But, when concerns about economic growth are uppermost, returns can move in opposite directions, increasing the diversification benefits of Treasuries.

If 2023 is dominated by concerns about growth, Treasuries could resume their traditional role as portfolio diversifiers, Page predicts. But, over the longer run, he says, different tools may be needed. These could include:

- “Barbell” structures that divide bond allocations between long Treasuries and fixed income diversifiers such as high yield, floating rate, and EM debt.“Barbell” structures that divide bond allocations between long Treasuries and fixed income diversifiers such as high yield, floating rate, and EM debt.

- Alternative strategies that seek to deliver positive absolute returns.

- Real assets equities, such as energy, real estate, and metals and mining stocks.

- Equity strategies that potentially offer downside risk mitigation in inflationary environments when Treasuries fail.

For illustrative purposes only. This is not intended to be investment advice or a recommendation to take any particular investment action.

Download the full 2023 Global Market Outlook insights here

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.