February 2022 / GLOBAL FIXED INCOME

Unlocking Impact Outside of ESG-Labeled Debt

Driving real change means investors should look beyond the label.

Key insights

- Although debt with an ESG‑related tag gain most of the attention, investing in vanilla, non‑labeled bonds can have a greater impact at both societal and financial levels.

- Broadening the opportunity set gives impact investors the chance to back companies making tangible effects while also avoiding paying a premium for labeled bonds.

- Analyzing the depth of impact, as well as implementing ongoing reporting, are keys to fostering long‑term change in non‑labeled markets.

Environmental, social and governance (ESG) considerations have become a cornerstone of the investing landscape. A bellwether for this has been the rapid growth of debt issued with an ESG‑related tag. These include green, social, and sustainable bonds—a range of debt instruments issued to fund projects that seek to have a positive effect on environmental and/or social issues, such as climate change or social inequality.

Yet, while these instruments have amplified investor interest and increased capital flows toward ESG‑conscious companies, they are not the only instrument for investors seeking to make a positive societal impact.

Indeed, assessing companies outside of ESG‑labeled bond markets can uncover significant opportunities in terms of delivering both positive impact and financial targets. Not only does this broaden the opportunity set, supporting companies directly—rather than being limited to funding specific projects—it can also help craft a portfolio that is better aligned with long‑term impact goals.

Why ESG Financing Goes Beyond Labels

ESG‑labeled debt has become a significant feature of the global bond market in recent years. According to T. Rowe Price analysis, green, social, sustainability, and sustainability‑linked issuance eclipsed the USD 1 trillion mark in 2021, compared with just USD 442 billion in 2020. This growth is one of many reasons why public debt markets play an increasingly important role in channeling the investment capital needed to make desired environmental and social impacts, such as those conveyed in the United Nations’ Sustainable Development Goals (UN SDG).

However, ESG‑labeled bonds do not have a monopoly in fixed income markets when it comes to impact investing. For many issuers, everyday activities—from energy resource transformation to lending decisions at a financial institution—can yield material and measurable environmental and social benefits. However, these companies choose not to tag their bonds with a label. And, given that last year corporates and governments raised more than USD 24 trillion in non ESG-labeled debt in bond markets, according to Bloomberg, it behooves impact investors to look broadly across the debt capital markets for compelling investment opportunities, let alone “impact” or “compelling impact” investment opportunities.

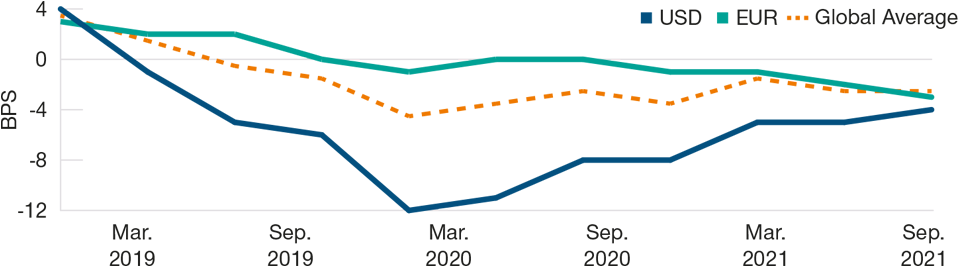

Investors Are Paying a Higher Price for ESG-Labeled Debt

(Fig. 1) Spread of non-green bonds to green bonds

Greenium for USD and EUR Investment Grade Corporates Over Time

As of September 30, 2021.

Source: Bloomberg Finance L.P. Analysis conducted by T. Rowe Price.

Broadening the Opportunity Set Improves the Potential to Make an Impact

On the one hand, widening the search area for impact investments may seem counterintuitive. Use‑of‑proceeds bonds are intrinsically linked to distinct projects, whether at an individual level or as part of an SDG framework. This means that the outcome, be it a project or target, can be clearly traced back to the initial ESG‑labeled investment, and the impact can therefore be quantified.

However, the notion that companies issuing ESG‑labeled bonds have more of an impact than those issuing non‑labeled bonds is flawed. In our view, confining impact investments to use‑of‑proceeds bonds would forgo the impact potential from funding issuers whose everyday activities contribute to the UN SDGs.

If we consider the desire to limit or slow the onset of climate change, for example, we may associate green bonds where proceeds fund projects such as electric vehicle research. However, looking at the SDG of combating climate change—measured partly by the pathway to reach “net zero” carbon emissions by 2050—a more holistic view of the fixed income space is required. For instance, it could be more impactful to invest in a renewable energy company, whose everyday activities are working to accelerate the decarbonization of the global economy by shifting energy production away from fossil fuels and toward low‑carbon alternatives.

Indeed, this scenario describes NextEra Energy Operating Partners (NEOP), a firm that operates a portfolio of wind, solar, and battery storage assets. On the surface, the company might go overlooked by impact investors purely focused on ESG‑labeled bonds as NEOP has not historically issued such instruments.

NEOP operates a portfolio of renewable energy assets comprising 6,250 megawatts of net capacity and, through its development pipeline, is targeting 17,300 megawatts by 2023–2024. So, although its bonds do not carry a “green” or ESG designation, investing in NEOP directly supports an issuer whose everyday activities are generating meaningful and measurable environment impacts.

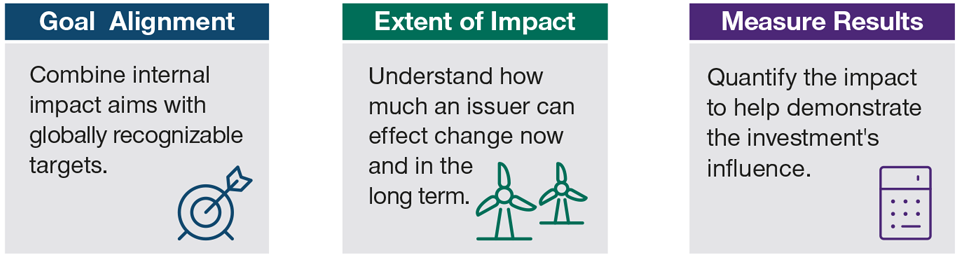

The Three Keys Behind Non-labeled Impact Investing

Attention to detail and accountability can drive positive change

Source: T. Rowe Price.

Making an Impact, Avoiding the “Greenium”

Non-‑labeled bonds have another advantage for impact investors: the fact that they trade at a discount compared with ESG‑labeled debt.

This so‑called “greenium”—the spread of an ESG‑labeled bond compared with the issuer’s non‑labeled curve—has widened over time in conjunction with rising demand for the asset class. ESG bonds denominated in euros, for example, have gradually become more expensive and, according to T. Rowe Price analysis, are trading at roughly a three‑basis point premium over vanilla bonds. And while U.S. dollar‑denominated ESG‑labeled debt has cheapened in relative terms since last year, nine months into 2021, they were still priced, at an average, five basis points more expensive than non‑ESG equivalents.

This makes sense at first glance, given that the point of ESG‑labeled bonds is to reduce the cost of capital for green and social projects by preferentially allocating capital to them. However, looking deeper, if impact investors can achieve the desired environmental or social effect without paying the usual premium associated with an ESG label, it is likely that investment will drift toward the non‑labeled segment.

Bigger Market Demands Deeper Research

Wading into non‑labeled bonds from an impact perspective is not necessarily simple. Debt with a green, social, or sustainability moniker provides a direct linkage from investment capital to measurable outcomes. In non‑labeled bonds, however, investors need to engage directly with the company on a forensic basis to ascertain whether the issuer is heading toward an impact that they are willing to finance.

Achieving this requires a methodical approach that appreciates impact investing outside of predefined, labeled bonds and necessitates deep research as well as long‑term commitment. In our view, there are three key steps along the way:

Align with impact goals: Impact measurement is complex. A present‑day analysis of the company’s activities, as well as a conceptualization about its potential influence, can help shape views on possible outcomes from an impact perspective. At T. Rowe Price, this decision‑making is shaped around our own proprietary impact pillar framework, a set of three overarching aims that are linked to the UN’s Sustainable Development Goals.

Understand the level of impact: While alignment is a good starting point, it’s also important to conduct impact due diligence on an issuer to gain a deeper understanding of its impact footprint. Our research and investment teams apply a five dimensions of impact framework to help us formalize an impact thesis, highlight negative externalities and risks, and define key performance indicators for each security to assist in the measurement of a company’s impact in the present and over longer time periods.

Measure and report on outcomes: Quantifying tangible results of an impact investment is vital to demonstrate how investment decisions have direct positive consequences. This needs to be undertaken through quantitative, external data, where possible, to help demonstrate an objective reflection of an investment’s impact.

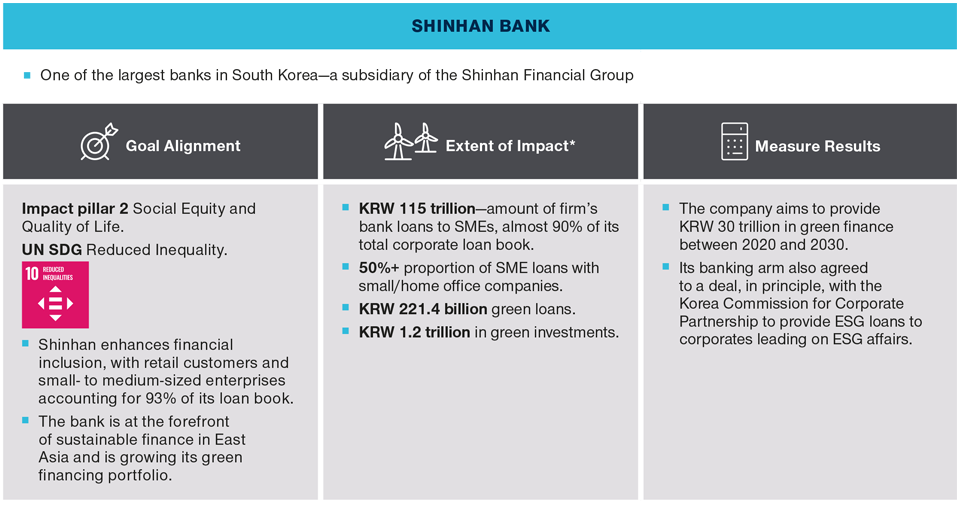

Inside the Life of a Non-labeled Impact Investment

*Data from company third‑quarter results report.

Source: Shinhan Financial Group Business Results, 3Q 2021.

The specific securities identified and described are for informational purposes only and do not represent recommendations.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

February 2022 / MARKETS & ECONOMY

February 2022 / GLOBAL FIXED INCOME