September 2021 / INVESTMENT INSIGHTS

Regulatory Actions in China: Short-Term Pain, Long-Term Gain

Beijing’s tightening grip bodes well for China Inc.'s health

Key Insights

- China’s policy objectives have expanded from financial deleveraging to include national security and social objectives.

- The new laws and regulations reflect the government’s agenda and are seen as fostering sustainable growth potential and, ultimately, more stable cash flows for firms.

- Regulatory actions have been the driving force for credit spread differentiation. Fundamental research and security selection can help investors in Asian credit navigate through the turbulence.

China’s regulatory actions, driven by Beijing’s financial, security, and social objectives, have injected volatility into the credit market over the past year. Key themes such as the mantra of housing for living in, not speculation; reducing the education cost burden for families; and tightening data security issues for technology companies have become important considerations within the investment process.

The announcement of a new five-year plan makes clear that regulatory oversight will remain tight in the medium term. But despite the uncertainty around implementation, this does not dampen prospects for the asset class more broadly. Against this backdrop, there will continue to be periods of volatility that may present attractive buying opportunities. The current wave of selling in Chinese assets on the back of regulatory crackdowns may well be a case of throwing the baby out with the bathwater. We think irrational price dislocations have occurred that could present an opportunity for discerning investors who have a sound security selection strategy.

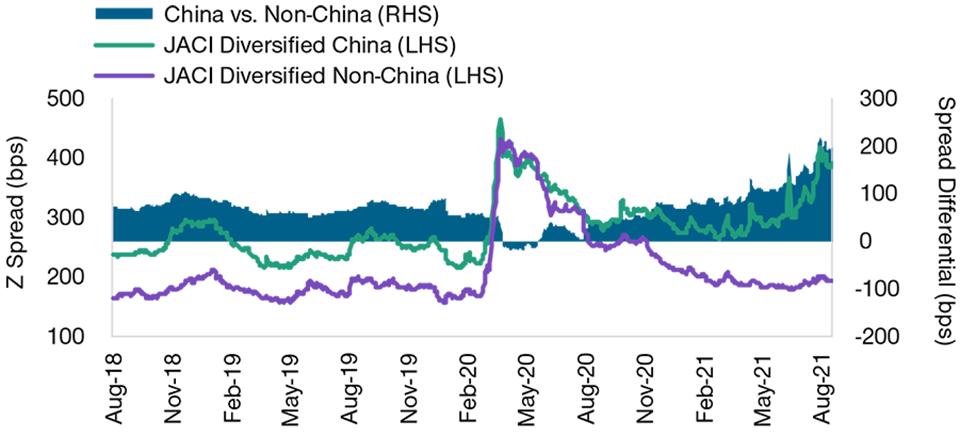

Prices of Chinese corporate dollar bonds have come under strong pressure after Beijing embarked on its campaign of regulatory overhaul. These moves, which first began with leverage regulations in the property sector last year, later spread to crackdowns on big tech companies and have now shown up in the education sector. The government’s new education rules have dealt a big blow to corporate profitability prospects for listed private sector education companies. Reflecting the damage in the credit market, the J.P. Morgan Asia Credit Index (JACI) fell 0.42% in July and as of August 10 is -0.29% year-to-date (YTD). In contrast, the JACI Diversified rose 0.02% in July, and as of August 10, YTD returns are positive at 0.44%. This benchmark, against which the T. Rowe Price Asia Credit Bond Strategy performance is measured, outperformed the JACI because of its more balanced allocation to China.

China Credits Remain Cheap Relative to Rest of Asia

(Fig. 1) Spreads have widened in the past year

Past performance is not a reliable indicator of future performance.

As of August 19, 2021.

Source: J.P. Morgan Chase & Co. (See Additional Disclosure.)

Social Priorities Tighten Regulatory Leash

These steps are driven by the government’s social agenda in housing, education, and tech monopolies at a time when China is keen to offset the negative impact generated by competitive capitalism and also wishes to rein in the high costs of child raising. China’s demographic profile has added to concerns the country would grow old before it gets rich, spurring the authorities to take more active measures.

Ahead of next year’s Party Congress, Beijing’s regulatory crackdown is also aimed at addressing the issue of income inequality, in our view. By removing anticompetitive practices and lowering barriers to entry, some of that gap could be bridged. The recent document published by the top level of Chinese authorities makes clear that regulatory oversight will remain a persistent theme through 2025 and so should remain top of mind for investors over the medium term.

Maturing Economy Calls for a Shift in Approach

Beijing is also reviewing the overseas listing variable interest entities (VIE) structure, widely used by Chinese technology and education companies to bypass restrictions on direct foreign ownership when raising overseas funding. Chinese companies looking to list offshore will need approval from the relevant ministry, as opposed to in the past when no formal go‑ahead was required. This signaled discomfort with offshore listings, especially via the VIE structure, which are not strictly recognized legally but which have been tolerated for many years.

The regulatory measures in themselves are from a familiar playbook, and we are not surprised. The move to regulate large internet platform companies that have grown into quasi‑monopolistic positions or that have access to large amounts of user data follows a historical pattern. In the past, we have seen companies deploying new technologies and being allowed to grow for many years. But as the technology becomes more mature and other users come to depend on it, regulation steps in.

In our opinion, by making such regulations in the internet and e-commerce sectors, Beijing is limiting these firms’ ability to exploit the information they have acquired for themselves. It is also a means of plugging any source of potential data leakage overseas in a way that could compromise national security. The moves against VIEs seems to be aimed at exerting more control over China’s technology and education companies by encouraging some of these structures to unwind.

The aftershocks are still being felt as investors study the implications of the recent moves—but we think these regulatory pressures have always existed and in themselves are not new. We see the regulators taking administrative measures aimed at promoting social stability and government authority, and applying more regulatory oversight may dampen risk-taking behavior to some degree. We also think that, going forward, the government will be mindful about financial market stability following the sharp correction in July.

Familiar Playbook—Two Steps Forward, One Step Back

While the latest abrupt regulatory changes have had a negative effect on business confidence, it is important to remember that we have seen the implementation of policies move in cycles that lead to initial negative reactions and hits to confidence that are then followed by efforts to stabilize sentiment—a case of two steps forward, one step back.

Instances of such cyclical approaches include the period in 2015–2016 when private firms were first allowed to default and again in 2018 when several highly leveraged conglomerates were taken over as the private company owners who had pledged their shares as collateral for loans were forced to sell to state-backed entities when a falling market triggered margin calls.

China’s authorities have applied regulatory pressure on technology firms in the past, though their aims then were more limited. In these instances, after initial application of strong pressure lasting several months, the authorities responded with some easing plus modest macro stimulus to stabilize sentiment.

Within the past few weeks, there have been steps taken to provide reassurance to investors and market participants. The China Securities Regulatory Commission held a meeting with foreign banks operating in China, telling them not to “overinterpret” recent actions as implying a decoupling of U.S.‑China financial markets. The People’s Bank of China has also injected incremental liquidity into the financial system to help calm markets.

Credit Selection Is the Key Differentiator

Our exposure to the China education sector was limited during July 2021, and the portfolio owns a name that, in our view, has a strong liquidity position and whose revenues should be little impacted by the regulatory changes.¹ In the property sector, our focus has been on high-quality names while maintaining a risk-neutral position—weaker sentiment may open up selective pockets of value in the coming quarters.

The crackdown on the internet sector has not changed our view on our credit picks, which we believe have strong balance sheets and solid net-cash positions. We believe regulatory changes are unlikely to damage their credit profiles in the short to medium term, and the divergence in valuations versus their developed market peers has largely been in equities with very little spillover into credit.

The quick responses made by some tech companies have shown their willingness to rein in aggressive growth plans and adhere to a more disciplined financial model. While this may reduce profitability in the face of the likely increase in competition, it also suggests a more sustainable growth trajectory and potentially greater stability in cash flows. These conditions, in our view, are positive for investing in credit markets. The new regulatory changes have also motivated tech companies to rethink their strategies to create value to all stakeholders, not just shareholders, which should improve their environmental, social, and governmental standing over time.

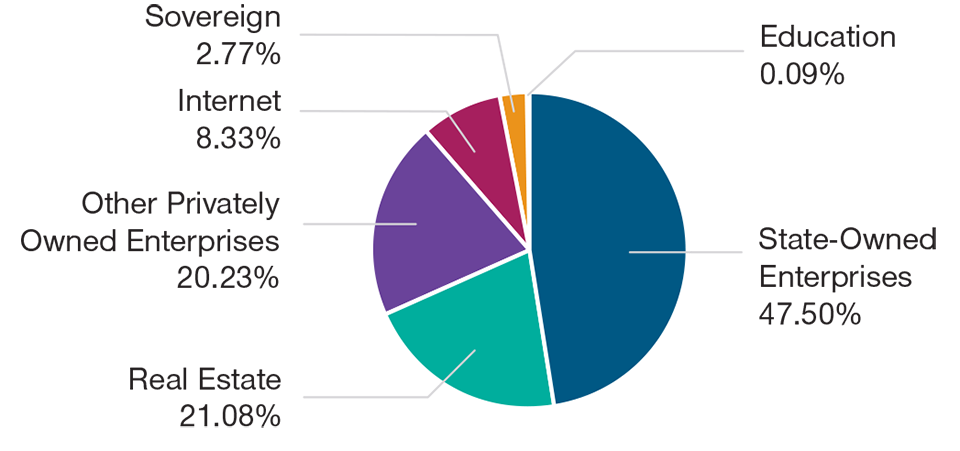

China Composition in J.P. Morgan Asia Credit Index Diversified

(Fig. 2) State-owned enterprises and real estate are the heavyweights

As of July 31, 2021.

Source: J.P. Morgan Chase & Co. (See Additional Disclosure.)

Turning to the property sector, we believe the implementation of Beijing’s “three red lines” policy targeted at curbing property developers’ leverage would ultimately lead to a healthier sector backdrop and more sustainable balance sheets in the medium term. Along the way, some accidents may occur and some developers may run into default, which may create some contagion and volatility. At the same time, we don’t expect fundamentally sound Chinese issuers to face sustained credit stress, and they would likely end up with healthier balance sheets in the medium term.

Investors have also acknowledged the benign impact of these regulations in the stronger segment of the credit market. For example, the spreads of China’s tech giants Alibaba and Tencent continue to trade tight versus the index, reflecting their immense market power and influence. The market seems to take comfort in owning the highest-quality Chinese credits. We have also applied our proprietary framework in assessing the regulatory risks against individual credits and prudently invest in those with what we view as, superior regulatory risk‑adjusted return potential.

Still, we believe the current environment of regulatory crackdowns could throw up some interesting investment opportunities in China’s credit market, and we hold some cash to try to take advantage of such situations if and when they arise.

The Chinese government has been supportive of the internet and property sectors for the past two decades, both in terms of favorable regulations and the buildup of infrastructure, as developing these key sectors promoted economic prosperity. The focus has now shifted to achieving more equitable objectives like social stability and reinforcing government authority.

Additional policy steps toward furthering social objectives—such as repositioning housing as living spaces rather than speculative investments, reducing the education cost burden for families, or deriving better value from the big tech firms and promoting greater profit sharing with small and medium enterprise vendors and employees—have the potential to move markets. We are mindful of how companies in our portfolio are positioned in such a dynamic backdrop.

The focus may have moved to tightening government authority and improving social stability in the medium term, but we believe the long‑term goal of promoting economic prosperity remains intact.

Composite Standard Annualized Asia Credit Bond Composite

Asia Credit Bond Composite

As of August 31, 2021

Figures are Calculated in U.S. Dollars

Past performance is not a reliable indicator of future performance.

Source: J. P. Morgan Chase & Co. (See Additional Disclosure.).

Gross performance returns are presented before management and all other fees, where applicable, but after trading expenses. Net of fees performance reflects the deduction of the highest applicable management fee that would be charged based on the fee schedule contained within this material, without the benefit of breakpoints. Gross and net performance returns reflect the reinvestment of dividends and are net of all non-reclaimable withholding taxes on dividends, interest income, and capital gains.

Source for J.P. Morgan Chase: Information has been obtained from sources believed to be reliable but J.P. Morgan does not warrant its completeness or accuracy. The index is used with permission. The Index may not be copied, used, or distributed without J.P. Morgan’s prior written approval. Copyright © 2021, J.P. Morgan Chase & Co. All rights reserved.

*Net of fees performance reflects the deduction of the highest applicable management fee that would be charged based on the fee schedule appropriate to you for this mandate, without the benefit of breakpoints. Past performance is not a reliable indicator of future performance.

Risks – the following risks are materially relevant to the portfolio:

China Interbank Bond Market risk – market volatility and potential lack of liquidity due to low trading volume of certain debt securities in the China Interbank Bond Market may result in prices of certain debt securities traded on such market fluctuating significantly.

Contingent convertible bond risk – contingent convertible bonds have similar characteristics to convertible bonds with the main exception that their conversion is subject to predetermined conditions referred to as trigger events usually set to capital ratio and which vary from one issue to the other.

Country risk (China) – all investments in China are subject to risks similar to those for other emerging markets investments. In addition, investments that are purchased or held in connection with a QFII licence or the Stock Connect program may be subject to additional risks.

Credit risk – a bond or money market security could lose value if the issuer’s financial health deteriorates.

Currency risk – changes in currency exchange rates could reduce investment gains or increase investment losses.

Default risk – the issuers of certain bonds could become unable to make payments on their bonds.

Emerging markets risk – emerging markets are less established than developed markets and therefore involve higher risks.

Frontier markets risk – small market nations that are at an earlier stage of economic and political development relative to more mature emerging markets typically have limited investability and liquidity.

High yield bond risk – a bond or debt security rated below BBB- by Standard & Poor’s or an equivalent rating, also termed ‘below investment grade’, is generally subject to higher yields but to greater risks too.

Interest rate risk – when interest rates rise, bond values generally fall. This risk is generally greater the longer the maturity of a bond investment and the higher its credit quality.

Issuer concentration risk – to the extent that a portfolio invests a large portion of its assets in securities from a relatively small number of issuers, its performance will be more strongly affected by events affecting those issuers.

Liquidity risk – any security could become hard to value or to sell at a desired time and price.

Sector concentration risk - the performance of a portfolio that invests a large portion of its assets in a particular economic sector (or, for bond portfolios, a particular market segment), will be more strongly affected by events affecting that sector or segment of the fixed income market.

General Portfolio Risks

Capital risk – the value of your investment will vary and is not guaranteed. It will be affected by changes in the exchange rate between the base currency of the portfolio and the currency in which you subscribed, if different.

ESG and Sustainability risk - may result in a material negative impact on the value of an investment and performance of the portfolio.

Counterparty risk – an entity with which the portfolio transacts may not meet its obligations to the portfolio.

Geographic concentration risk – to the extent that a portfolio invests a large portion of its assets in a particular geographic area, its performance will be more strongly affected by events within that area.

Hedging risk – a portfolio’s attempts to reduce or eliminate certain risks through hedging may not work as intended.

Investment portfolio risk – investing in portfolios involves certain risks an investor would not face if investing in markets directly.

Management risk – the investment manager or its designees may at times find their obligations to a portfolio to be in conflict with their obligations to other investment portfolios they manage (although in such cases, all portfolios will be dealt with equitably).

Operational risk – operational failures could lead to disruptions of portfolio operations or financial losses.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

September 2021 / INVESTMENT INSIGHTS