June 2022 / MARKET OUTLOOK

Flexible Fixed Income

Bonds struggled to diversify against equity risk in the first half of the year, so how should investors approach fixed income?

U.S. Treasuries and other developed sovereign bonds did an exceptionally poor job of offsetting equity volatility in the first half. This suggests that investors may need to expand their search for diversification across fixed income sectors and geographic regions.

A key question, Page says, is whether the spike in stock/bond correlations seen in early 2022 was just temporary or reflected a structural “regime change” that could keep correlations high for an extended period. If the latter explanation is correct, alternatives to the traditional 60/40 stock/bond allocation that include dynamic hedging and other defensive strategies could offer advantages to some investors.

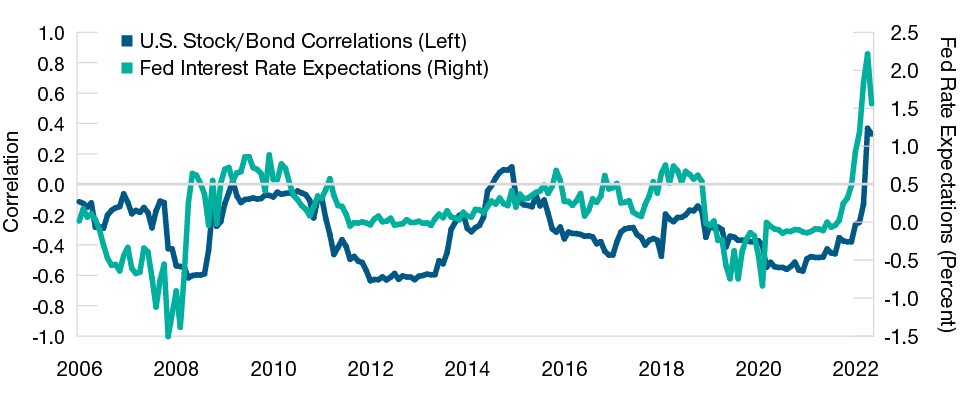

Stock/bond correlations have switched from positive to negative several times in recent years, Page notes (Figure 4). T. Rowe Price research suggests that these shifts typically were caused by economic shocks—sudden spikes in unemployment, inflation, or interest rates.

In a Rising Rate Environment, Bond Investors May Need More Diversification

(Fig. 4) Fed rate expectations vs. U.S. stock/bond correlations*

Past performance is not a reliable indicator of future performance.

January 2006 through May 2022.

*Fed interest rate expectations = yield on two‑year Treasury note minus federal funds target rate. U.S. stock/bond correlations = rolling two‑year correlation of monthly price changes for the S&P 500 Index and the 10‑year U.S. Treasury futures contract.

Sources: Standard & Poor’s, J.P. Morgan North America Credit Research (see Additional Disclosures), and Bloomberg Finance L.P. Data analysis by T. Rowe Price.

“I think Treasuries still have a role to play in portfolio allocations—especially if the next leg of the crisis is a recession,” Page says. “But I also think investors are going to want to consider other approaches to downside risk mitigation.”

Is It Time to Extend Duration?

A more immediate issue for fixed income investors is whether bond yields have reached a near‑term peak, creating a potential opportunity to lock in portfolio income.

“In our view, this is the most attractive point to buy bonds that we’ve seen for several years,” Husain says. “We think that over the next several quarters investors may want to consider adding duration.”

However, Husain also predicts that the Fed will continue tightening until it has pushed its key market rate, the federal funds rate, into positive territory in after‑inflation terms. With the nominal fed funds rate still under 1% at the end of May, that would seem to leave considerable room for further rate hikes. As of early June, he adds, “I don’t think we’re quite at the peak for yields.”

For U.S.‑based investors worried about rising rates, global markets could offer diversification potential, Husain suggests. While the Fed is tightening, other countries are further along in their interest rate cycles. Some have stopped raising rates. Others have even started cutting them.

“By taking advantage of monetary policy divergence, investors can seek to diversify their interest rate exposures on a currency‑hedged basis,” Husain explains. Recent valuation levels potentially make emerging markets (EM) U.S. dollar bonds particularly attractive, he adds, although both country selection and underlying security selection will be critical.

The Upside Potential of Higher Yields

If yields do continue to rise, Husain says, at some point they should reach levels that offer attractive income opportunities for investors who understand how to manage duration— or who can rely on skilled investment professionals to do it for them. “Over the medium term, I think yields will reach levels that will make clients happy with the income they’re getting from their bond portfolios,” he says.

Some credit sectors, such as high yield corporate bonds, may have reached that point, Husain suggests. “Looking at the high yield universe, I’ve seen yields in the 7% to 8% range, in some cases,” he says. “I’ve seen some BB rated bonds priced at 80 cents on the dollar. Those are levels that historically have proven to be good buying points.”

The caveat to the bullish case for high yield is the uncertain economic outlook, Husain notes. As of May, high yield default rates remained near historical lows, and rating upgrades were more than twice as high as downgrades. But a growth shock could quickly change that picture.

“The threat of recession is real,” Husain cautions. “So investors need to do their homework.” For T. Rowe Price fixed income portfolio managers, he adds, this will mean relying on the firm’s extensive research capabilities and independent credit ratings to help navigate risks.

In volatile markets, duration management and yield curve positioning also could be important tools for managing risk, Husain suggests. “Fixed income is a relatively liquid asset class, so I would argue that investors could potentially benefit by using that liquidity to stay active,” he says.

For illustrative purposes only. This is not intended to be investment advice or a recommendation to take any particular investment action.

Download the full 2022 Midyear Market Outlook insights

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.