February 2022 / GLOBAL FIXED INCOME

Strategic Allocation to Bank Loans May Enhance Value

The asset class offers a low duration profile, attractive yields.

Key Insights

- Perhaps best known for historically performing well in rising rate environments, floating rate bank loans provide a unique combination of high yield potential and low duration.

- We believe the long‑term historical performance of the asset class through a range of rate environments speaks to its durable nature and value as a strategic allocation.

- Collaboration between the firm’s Equity and Fixed Income Divisions is crucial to pursuing better outcomes for our clients over time.

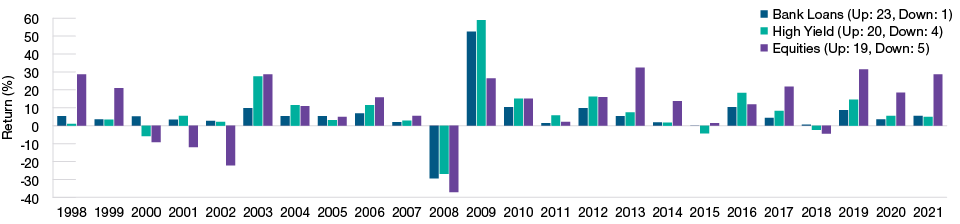

Many investors tend to focus on bank loans only when there is a broad consensus about the Federal Reserve raising interest rates in the short term. While loans have historically performed well under those conditions, we believe the asset class can potentially add value as a strategic allocation in various market environments within the economic and interest rate cycles. Loans have provided positive returns in 24 out of the last 25 years (Figure 1).1 This speaks to the historically durable nature of the asset class. Due to its unique low‑duration2 profile, the loan asset class has generally been negatively correlated with many fixed income alternatives. Therefore, we believe it can act as an effective diversifier in a broader fixed income portfolio.

A Compelling Long-Term Allocation

(Fig. 1) Bank Loan Annual Returns

As of December 31, 2021.

Past performance cannot guarantee future results.

Annual returns represented by the S&P/LSTA Performing Loan Index and J.P. Morgan Global High Yield Index. Equities represented by S&P 500 (see Additional Disclosures). We also show the number of periods that the asset classes were up and down.

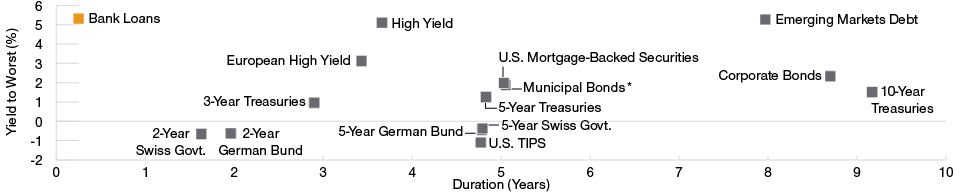

The current macro environment has led to an increase in intermediate‑ and long‑term Treasury yields. Duration risk is in the foreground with the Fed having pivoted to a more hawkish tone over tapering its asset purchases and signaling upcoming rate hikes to combat persistently high inflation. The floating rate feature of loans—where coupons adjust based on a short‑term benchmark rate such as the London Interbank Offered Rate (LIBOR) or the Secured Overnight Financing Rate (SOFR)—gives them a low‑duration profile. Therefore, loans may offer some protection from rising interest rates while providing the potential for attractive income (Figure 2).

Higher Income With Lower Duration

(Fig. 2) Duration and yield across fixed income sectors

As of December 31, 2021.

Past performance is not a reliable indicator of future performance.

*Taxable‑equivalent yield assuming a 40.8% tax‑rate.

Sources: J.P. Morgan Chase & Co., Bloomberg Index Services Ltd., Bloomberg Finance, L.P., and ICE BofAML (see Additional Disclosures).

Bloomberg Indices: Corporate Bonds: U.S. Corporate Investment Grade Index; Municipal Bonds: Municipal Bond Index; U.S. Mortgage‑Backed Securities: MBS Index; U.S. TIPS: U.S. Treasury: U.S. TIPS; 2 Year Swiss Govt.: Swiss Aggregate: Treasury 1–3 Years; 5 Year Swiss Govt.: Swiss Aggregate: Treasury 3–7 Years; J.P. Morgan Chase & Co. Indices: High Yield: Global High Yield Index; Bank Loans: Leveraged Loan Index; Emerging Markets Debt: EMBI Global Diversified Index; 2 Year German Bund: 2 Year German Bund benchmark; 5 Year German Bund: 5 Year German Bund benchmark. From Bloomberg Finance, L.P.: 3‑Year Treasuries represented by the U.S. 3‑Year Treasury Note in the U.S. Treasury Actives Curve; 5‑Year Treasuries represented by the U.S. 5‑Year Treasury Note in the U.S. Treasury Actives Curve; 10‑Year Treasuries represented by the U.S. 10‑Year Treasury Bond in the U.S. Treasury Actives Curve; European High Yield represented by the ICE BofA European Currency High Yield Constrained Excluding Subordinated Financials Index Hedged to USD.

Meaningful Income From Bank Loans

Given the current prevalence of higher‑quality assets with very low or negative yields, the loan asset class is one of the few fixed income segments where investors should be able to find relatively greater income. In 2020, after the global pandemic stalled new issuance, issuers incentivized investors to reengage in the loan market by offering favorable deal terms, including LIBOR floors—a minimum value imposed on the benchmark component of the floating rate coupon—and new issue discounts to par. Both features helped keep yields in the bank loan market at relatively attractive levels, while today, the yield is enhanced by the near‑term prospect of rising short‑term interest rates.

Persistently high inflation has led the Fed to signal an increasingly rapid tightening of monetary conditions. Bank loan coupons are poised to reset higher in 2022 as the central bank implements incremental short‑term rate increases. We believe that the potential resiliency of loan income in differing rate scenarios contributes to the attractive value of the asset class.

Relatively Lower‑Risk Way to Access Sub‑Investment‑Grade Credit

Loans generally have high yield credit ratings but provide a lower‑risk way to access the sub‑investment‑grade credit market relative to high yield bonds. As an asset class, loans have a higher repayment priority than high yield bonds if an issuer defaults. Historically, this has resulted in higher recovery rates in default situations. At the end of 2021, for example, the long‑term recovery rate for U.S. high yield bonds was around 40%, compared with roughly 65% for U.S. loans. The default rate was extraordinarily low (near 0%) given loose monetary conditions and improving fundamentals throughout the economic recovery.

Historically, loans have tended to yield less than high yield bonds due to their higher‑quality characteristics, but today, the two options have similar yields and credit spreads.3 Given their shorter‑duration profile and seniority in the capital structure, we believe the loan asset class provides investors a more defensive way to add exposure to the below investment‑grade market while also providing attractive income. Still, bank loans can become illiquid during periods of market stress, and the asset class is subject to credit risk. Therefore, selecting winners and avoiding troubled credits through active management is critical.

Collaboration May Foster Better Outcomes

Our long‑tenured team has significant experience and scale in the bank loan market. T. Rowe Price’s sub‑investment‑grade platform is a single research team covering high yield bonds and bank loans, which allows us to try to capture relative value and inefficiencies across both asset classes. Furthermore, our below investment‑grade analysts are part of a much broader research organization. The ability and willingness to share information and insights between the Equity Division and all fixed income teams are crucial in potentially generating better outcomes for our clients over time.

For example, collaboration with our equity colleagues recently enabled us to participate in a private credit offering by electric vehicle manufacturer Rivian.4 Our equity platform was a top shareholder of the company’s private equity, which allowed our team to conduct thorough due diligence as we underwrote the private credit. The company’s initial public offering in November also provided us with a meaningful cushion from subordinated capital.

Rivian is developing vehicles primarily targeting the attractive truck, sports utility vehicle, and commercial vehicle end market segments. Amazon is an owner and has a large business‑to‑business contract with Rivian to provide vans, which should help cushion demand volatility and support operating leverage. We have a favorable outlook on the potential for electric vehicles to take market share broadly, and this investment provided an opportunity to express that view outside of the syndicated loan universe.

What we’re watching next

The emergence of coronavirus variants that could delay the reopening of the economy from the impact of the pandemic is an important consideration. We are also closely monitoring the potential for robust demand for the asset class to cause a meaningful increase in repricing transactions as well as less favorable deal terms.

Important Information

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is no guarantee or a reliable indicator of future results.. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

USA—Issued in the USA by T. Rowe Price Associates, Inc., 100 East Pratt Street, Baltimore, MD, 21202, which is regulated by the U.S. Securities and Exchange Commission. For Institutional Investors only.

© 2024 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.

February 2022 / INVESTMENT INSIGHTS

February 2022 / ENVIRONMENTAL, SOCIAL, AND GOVERNANCE