December 2020 / Market Outlook

Investment Ideas for the Next 12 Months

Positioning your portfolio for the challenges and opportunities ahead

Key Insights

- The year 2020 proved to be particularly challenging for investors as the coronavirus pandemic upended growth expectations and generated unprecedented policy responses.

- We have identified five themes for 2021: Post‑pandemic recovery, politics and the pandemic, policy and low yields, parting styles, and pricey safety.

- As these dynamics play out, we have identified a range of investment ideas we believe may be effective in helping to navigate the period ahead.

Investors will remember 2020 with mixed emotions. On one hand, it was the year of the catastrophic coronavirus pandemic, with its devastating human and economic tolls. On the other hand, it was a year that delivered strong positive returns across a wide range of financial markets—an extraordinary outcome given the destructive economic backdrop. Against such wildly contrasting dynamics, what lies ahead for 2021, and how might investors position their portfolios in response?

Trying to imagine the future is a difficult task in normal times. As the times we are living through are anything but normal, marked as they are by a very high degree of uncertainty, identifying the likely direction of events is even more challenging. Nonetheless, we have identified five key themes we believe will drive the performance of economies and markets over the coming 12 months and beyond:

- Post‑pandemic road to recovery

- Politics and the pandemic

- Policy and low yields

- Parting styles amid disruption

- Pricey safety

1. Post‑Pandemic Road to Recovery

The pandemic is impacting markets in multiple ways. One is through its effect on the global economy—both in terms of the current slowdown and the eventual shape of the recovery. We believe the economy will continue to mend, but the recovery is likely to be choppy, potentially including a double‑dip contraction, before the rollout of vaccines is underway. Then, we hope, will we commence a slow return to some normality.

A second way in which the coronavirus is affecting markets is through its impact on behaviours. Policymakers appear set to do whatever they can to stimulate the economy, but corporations and consumers may remain cautious if the economic hardship drags on and the pandemic gets worse before it gets better. As we have seen during 2020, sentiment may pulse with bursts of optimism and pessimism, adjusting to rising and falling rates of infection, government efforts to control outbreaks, and news about vaccines.

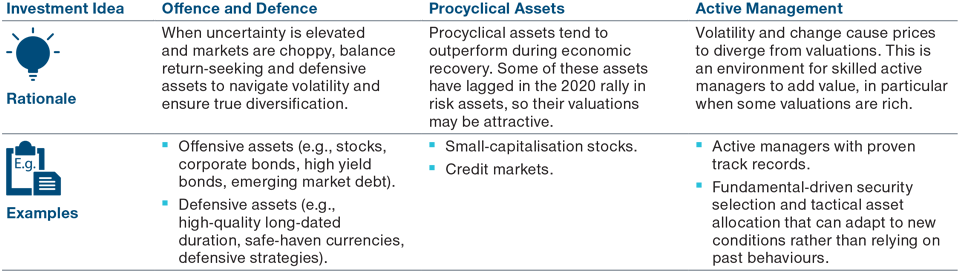

One certainty is uncertainty: professional investors are trained to make sense of finance and economics, not of viruses and epidemiology. With this in mind, our first investment idea in this theme is to split portfolios into return‑seeking and conservative assets. When markets are driven by unfamiliar factors and emotions, portfolios should balance offensive and defensive characteristics to benefit from any upsides and protect against downsides.

Our second investment idea is to include procyclical assets in portfolios. Those assets tend to outperform during economic recoveries, and they have lagged in the 2020 rally of risk assets, so their valuations may be attractive.

Our third investment idea is to identify and use skilled active management. The shift from the pre‑pandemic, relative benign environment, through the shock of the crisis, to the post‑pandemic recovery have caused considerable volatility and divergence between prices and intrinsic values. This environment is ripe for active management to add value, especially as some asset valuations are stretched, making it harder for passive investing to generate attractive returns.

2. Politics and the Pandemic

In normal times, geopolitics are mostly background noise for markets. However, such ‘normal’ times have not existed for more than a decade. The pandemic has accelerated a series of secular changes, including the widening wealth gap, rising social discontent, growing populism, increased protectionism, and the rise of China. Although we expect President‑elect Joe Biden to be less confrontational than President Donald Trump, and the terms of the UK’s exit from the EU to be substantively resolved, we believe geopolitical tensions are here to stay.

Geopolitical disorder and change impact every region of the world. The US must adapt to a new president and new administration’s policies while facing the possibility that a divided Congress will lead to regulatory gridlock. The ‘Japanification’ of Europe is underway, putting strain on the EU and its unity. In Russia, the leadership may change. China is emerging economically stronger from the pandemic, lifting tensions with the US in what we call Cold War II.

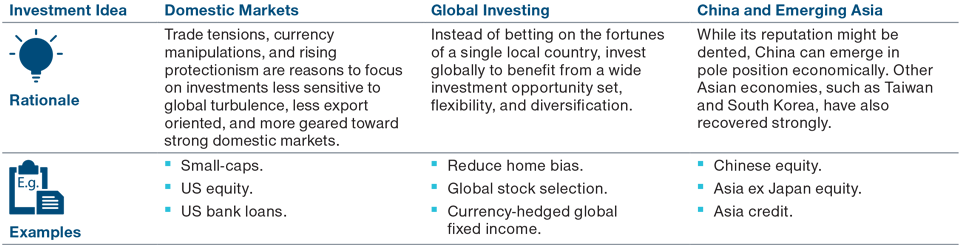

Our first investment idea here is to focus on assets in domestic markets with lower sensitivity to global turmoil, currency swings, and changes to globalised business models and supply chains. Another idea is to diversify and invest globally, searching for opportunities wherever they are in equity and fixed income markets, thereby reducing the risk of a major geopolitical development adversely affecting the domestic market.

Our third idea in this theme is to invest in China and emerging Asia. This group of countries compose about 80% of the MSCI Emerging Markets Index and may emerge as winners as they have been less impacted by the pandemic. Luckily, China needs to export its produce to the US and find a home for its domestic savings, while the US needs to import goods from China and finance its trade and government deficits, keeping a balance between the two superpowers.

3. Policy and Low Yields

The pandemic and geopolitical tensions have driven policymakers to stimulate the regions under their responsibility. If unconventional monetary policy and the expansion of central banks’ balance sheets became the new normal over the past decade, fiscal stimulus and expansion of public deficits will become the new new normal of the next decade.

In nearly all developed economies, firms and consumers will continue to benefit from record‑low interest rates. Quantitative easing will continue if it is needed, leaving governments with no choice but to borrow and spend. Adam Smith’s invisible hand has disappeared.

The economic slowdown, combined with ultra‑accommodative policies, is likely to keep downward pressure on bond yields. Yields may rise from their 2020 historic lows, but material increases are unlikely. One reason for this is the likelihood of continued weak economic growth and inflation. Inflation might rise, but not significantly in the next 12 months before the economic recovery is on a strong footing. Another reason is persistent asset purchase programmes by central banks—‘fighting the Fed’ has proved to be a loser’s game over the past decade or more. A third reason why yields are likely to remain low is that when bond yields rise, investors such as pension funds rush to buy government bonds at slightly better prices, putting renewed downward pressure on yields. For all these reasons, yields and income are likely to remain scarce in 2021.

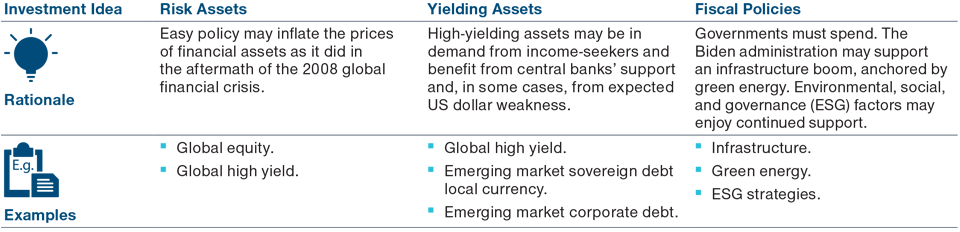

In this environment, one investment idea is to invest in risk assets despite the discomfort of uncertainty and rich valuations. Risk assets should continue to receive support from central banks, which are likely to support markets if data deteriorate.

A second idea is for income‑seekers to expand their opportunity set in the search for yield. Some assets, such as high yield, enjoy explicit support from central banks; others, such as emerging market debt, may benefit from recent US dollar weakness, which we expect to be a continued trend in the medium term. Although default rates could rise due to the pandemic, policies should support some firms, effectively bailing them out, keeping default rates at bay and spreads narrower than where they would be without policy intervention. Skilled active management and credit research can help to mitigate exposure to defaulting issuers.

Our third idea here is to seek assets that may benefit from fiscal spending and potential new policies of US President‑elect Biden.

4. Parting Styles Amid Disruption

Another key theme for 2020 is the diverging fortunes of different segments of the economy and markets. Volatility and the dispersion between losers and winners can create both risks and opportunities—while some areas keep suffering, such as hospitality and bricks‑and‑mortar retail, others may keep benefitting, such as technology and e‑commerce.

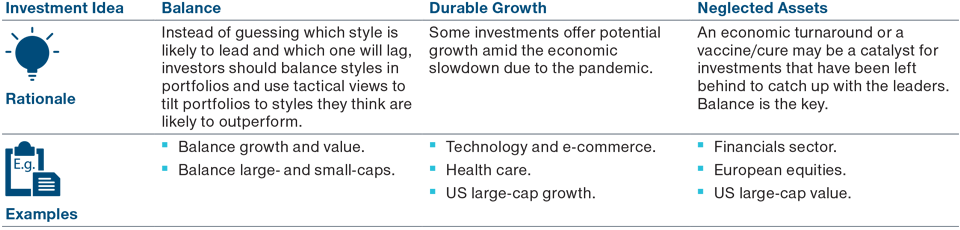

The investment environment ahead is likely to be characterised by switching leaders and laggards. Rising infections and continued curbs on activity may cause a ‘risk‑off, COVID‑on’ environment with outperformance of growth, large‑caps and US dollar strength; news about vaccines and the easing of lockdowns may introduce a ‘risk‑on, COVID‑off’ environment, where value and small‑caps take the lead and the dollar lags. Our first investment idea here is to maintain a balance in portfolios between potential winners and losers while using active management to lean into cycles of outperformance.

While the pandemic is destructive, destruction is constructive in some cases. As we adapt to life with the virus, some areas will flourish and disrupt, while others will wither and be disrupted. Our second investment idea in this theme is to select investments offering durable growth despite the pandemic.

Finally, the pandemic has led to diverging asset valuations. The price of some, such as technology and government bonds, rallied and their valuations now look like a headwind; the prices of others, such as financial and European equities, have lagged and their valuations now appear to be a tailwind. Although cheap valuations are not enough, a steadier economic recovery or a vaccine/cure, potentially leading to a market melt‑up, may see some rotation to the laggards. Our third investment idea is to balance likely winners and neglected losers.

5. Pricey Safety

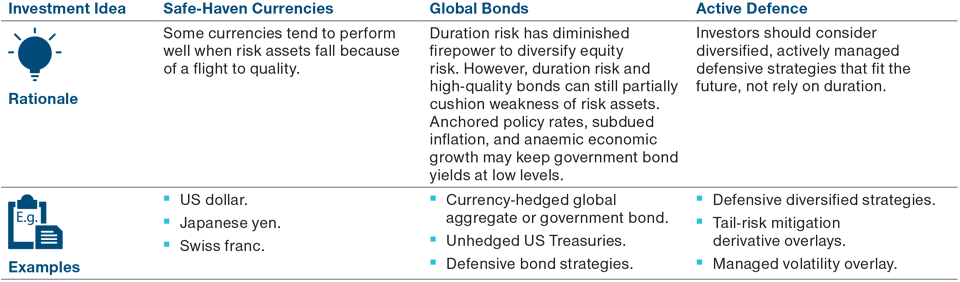

Ultra‑accommodative policy and pressured yields have pushed the prices of traditional conservative assets upward. The traditional way to diversify equity risk has been duration risk, but government bonds are currently expensive, with yields close to all‑time‑low levels. When yields are low, their scope to fall during sell‑offs of risk assets is reduced, limiting government bonds’ defensive power. The US dollar, another proven way to mitigate downside risk, is not cheap: Safety has become pricey. Because of uncertainty due to the pandemic and geopolitical tensions, safety is likely to remain expensive.

One investment idea here is to include safe‑haven currencies in portfolios, expanding from the US dollar to include the Japanese yen and Swiss franc. A second idea is to use active strategies to tap in to the global bond market and use other ways to mitigate downside risk. Our third idea is to use every weapon in our arsenal to create an active, diversified defensive strategy, using both traditional and innovative techniques, such as derivative strategies with defensive characteristics.

One key theme for 2021 is balance. Few investors can afford to retreat to less risky assets, especially when many of these are looking expensive relative to history. Portfolios should balance investments that can tap the upside if markets continue to do well and investments that can mitigate downside risk if markets retreat. When the future is murky, portfolios should be prepared for either good or bad outcomes.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.