North American Trade Pact: More Certainty, Muted Impact

Since the beginning of his 2016 presidential campaign, President Donald Trump has vowed to abandon trade agreements he believes hurt the U.S. economy. By replacing the North American Free Trade Agreement (NAFTA) with the U.S.‑Mexico‑Canada Agreement (USMCA), the president can state that he fulfilled his commitment to eliminate, in his words, “the worst trade deal of all time”—another step in his “Promises Made, Promises Kept” campaign.

But the new agreement—while perhaps having an only limited economic impact—offers talking points for those across the political spectrum.

In Trade, Much Like Politics, Timing Is Everything

Given the proximity of 2020 elections, U.S. politicians from both parties felt pressure to tout USMCA as an opportunity to help their constituents.

The president, beyond the headline fulfilling a key campaign promise, can say he’s cut a better deal for American companies, agriculture, and workers. His chief trade negotiator, Robert Lighthizer, claims that bipartisan support for the USMCA shows “you can have a permanent trade policy if you get the balance right.”

Democrats especially were eager to get on board with the agreement. In 2018, they took control of the House by winning some swing districts that are suburban and more politically moderate. Passing the USMCA allows the party to demonstrate that it engaged in bipartisan negotiations and action during a legislative session defined by impeachment.

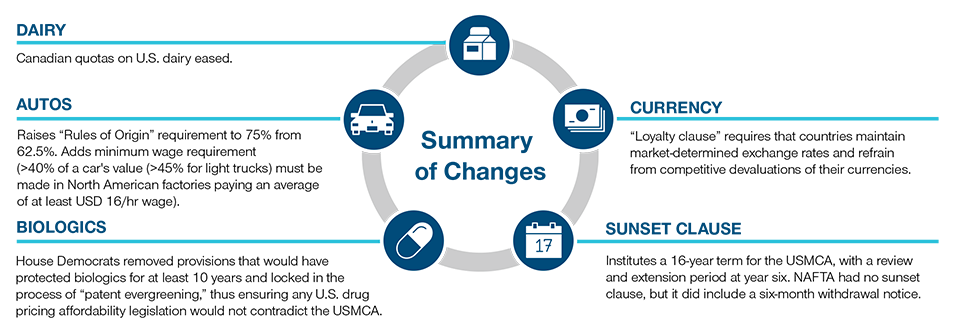

By touting that they achieved more stringent labor provisions within the USMCA, Democrats also can argue that they pushed through changes that will improve economic prospects for working Americans. Notably, the AFL‑CIO, the nation’s largest union federation, reluctantly signed off on the pact. Democrats also forestalled extended patent protections for biologic drugs, which will enable less‑expensive, generic competition in the marketplace.

As of mid‑January, the USMCA had been approved by both houses of the U.S. Congress and by the Mexican government. Canada’s passage of the accord will be required for full ratification.

Though the USMCA provides more trade certainty, the new accord between the United States and its two largest trading partners only incrementally alters the status quo.

Though the USMCA provides more trade certainty, the new accord between the United States and its two largest trading partners only incrementally alters the status quo.

The USMCA’s Incremental Impact

Both Republicans and Democrats can claim victories in the new North American trade deal.

Source: T. Rowe Price.

Modest Changes

Though the USMCA provides more trade certainty, the new accord between the United States and its two largest trading partners only incrementally alters the status quo. An International Monetary Fund (IMF) analysis found that the USMCA’s impact on the U.S. gross domestic product would be negligible in its current form, though the IMF said it would result in some material gain on specific industries, “mostly driven by improved market access.”

Among the changes: 75% of automotive parts will have to be manufactured in the U.S. to qualify for duty‑free treatment, up from 62.5% in NAFTA; 40% of cars’ values (45% for light trucks) must be assembled by workers earning a minimum USD 16‑an‑hour wage. (While this change will result in higher costs for U.S. manufacturers, T. Rowe Price auto analyst Joel Grant expects the U.S. auto industry to adjust.)

Moreover, the deal also will remove the Trump administration’s tariffs on steel and aluminum imported from Canadian and Mexican firms. The Canadian dairy market, long closed to U.S. farmers, also will be more accessible. And the pact gives U.S. technology companies the freedom to transfer and store data across North American borders.

While the USMCA makes modest changes to NAFTA, we believe it could be a significant contribution toward greater stability in North American trade by giving U.S. businesses more confidence to invest...

Pact Could Boost Confidence

While the USMCA makes modest changes to NAFTA, we believe it could be a significant contribution toward greater stability in North American trade by giving U.S. businesses more confidence to invest—even if that benefit comes from the reversal of uncertainty created by the Trump administration’s initial threat to withdraw from NAFTA.

Important Information

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

Australia—Issued in Australia by T. Rowe Price Australia Limited (ABN: 13 620 668 895 and AFSL: 503741), Level 50, Governor Phillip Tower, 1 Farrer Place, Suite 50B, Sydney, NSW 2000, Australia. For Wholesale Clients only.

Brunei—This material can only be delivered to certain specific institutional investors for informational purpose upon request only. The strategy and/or any products associated with the strategy has not been authorised for distribution in Brunei. No distribution of this material to any member of the public in Brunei is permitted.

Canada—Issued in Canada by T. Rowe Price (Canada), Inc. T. Rowe Price (Canada), Inc.’s investment management services are only available to Accredited Investors as defined under National Instrument 45-106. T. Rowe Price (Canada), Inc. enters into written delegation agreements with affiliates to provide investment management services.

China—This material is provided to specific qualified domestic institutional investor or sovereign wealth fund on a one-on-one basis. No invitation to offer, or offer for, or sale of, the shares will be made in the People’s Republic of China (“PRC”) (which, for such purpose, does not include the Hong Kong or Macau Special Administrative Regions or Taiwan) or by any means that would be deemed public under the laws of the PRC. The information relating to the strategy contained in this material has not been submitted to or approved by the China Securities Regulatory Commission or any other relevant governmental authority in the PRC. The strategy and/or any product associated with the strategy may only be offered or sold to investors in the PRC that are expressly authorized under the laws and regulations of the PRC to buy and sell securities denominated in a currency other than the Renminbi (or RMB), which is the official currency of the PRC. Potential investors who are resident in the PRC are responsible for obtaining the required approvals from all relevant government authorities in the PRC, including, but not limited to, the State Administration of Foreign Exchange, before purchasing the shares. This document further does not constitute any securities or investment advice to citizens of the PRC, or nationals with permanent residence in the PRC, or to any corporation, partnership, or other entity incorporated or established in the PRC.

DIFC—Issued in the Dubai International Financial Centre by T. Rowe Price International Ltd. This material is communicated on behalf of T. Rowe Price International Ltd. by its representative office which is regulated by the Dubai Financial Services Authority. For Professional Clients only.

EEA ex-UK—Unless indicated otherwise this material is issued and approved by T. Rowe Price (Luxembourg) Management S.à r.l. 35 Boulevard du Prince Henri L-1724 Luxembourg which is authorised and regulated by the Luxembourg Commission de Surveillance du Secteur Financier. For Professional Clients only.

Hong Kong—Issued in Hong Kong by T. Rowe Price Hong Kong Limited, 6/F, Chater House, 8 Connaught Road Central, Hong Kong. T. Rowe Price Hong Kong Limited is licensed and regulated by the Securities & Futures Commission. For Professional Investors only.

Indonesia—This material is intended to be used only by the designated recipient to whom T. Rowe Price delivered; it is for institutional use only. Under no circumstances should the material, in whole or in part, be copied, redistributed or shared, in any medium, without prior written consent from T. Rowe Price. No distribution of this material to members of the public in any jurisdiction is permitted.

Korea—This material is intended only to Qualified Professional Investors upon specific and unsolicited request and may not be reproduced in whole or in part nor can they be transmitted to any other person in the Republic of Korea.

Malaysia—This material can only be delivered to specific institutional investor upon specific and unsolicited request. The strategy and/or any products associated with the strategy has not been authorised for distribution in Malaysia. This material is solely for institutional use and for informational purposes only. This material does not provide investment advice or an offering to make, or an inducement or attempted inducement of any person to enter into or to offer to enter into, an agreement for or with a view to acquiring, disposing of, subscribing for or underwriting securities. Nothing in this material shall be considered a making available of, solicitation to buy, an offering for subscription or purchase or an invitation to subscribe for or purchase any securities, or any other product or service, to any person in any jurisdiction where such offer, solicitation, purchase or sale would be unlawful under the laws of Malaysia.

New Zealand—Issued in New Zealand by T. Rowe Price Australia Limited (ABN: 13 620 668 895 and AFSL: 503741), Level 50, Governor Phillip Tower, 1 Farrer Place, Suite 50B, Sydney, NSW 2000, Australia. No Interests are offered to the public. Accordingly, the Interests may not, directly or indirectly, be offered, sold or delivered in New Zealand, nor may any offering document or advertisement in relation to any offer of the Interests be distributed in New Zealand, other than in circumstances where there is no contravention of the Financial Markets Conduct Act 2013.

Philippines—THE STRATEGY AND/ OR ANY SECURITIES ASSOCIATED WITH THE STRATEGY BEING OFFERED OR SOLD HEREIN HAVE NOT BEEN REGISTERED WITH THE SECURITIES AND EXCHANGE COMMISSION UNDER THE SECURITIES REGULATION CODE. ANY FUTURE OFFER OR SALE OF THE STRATEGY AND/ OR ANY SECURITIES IS SUBJECT TO REGISTRATION REQUIREMENTS UNDER THE CODE, UNLESS SUCH OFFER OR SALE QUALIFIES AS AN EXEMPT TRANSACTION.

Singapore—Issued in Singapore by T. Rowe Price Singapore Private Ltd., No. 501 Orchard Rd, #10-02 Wheelock Place, Singapore 238880. T. Rowe Price Singapore Private Ltd. is licensed and regulated by the Monetary Authority of Singapore. For Institutional and Accredited Investors only.

South Africa—T. Rowe Price International Ltd (“TRPIL”) is an authorised financial services provider under the Financial Advisory and Intermediary Services Act, 2002 (FSP Licence Number 31935), authorised to provide “intermediary services” to South African investors.

Switzerland—Issued in Switzerland by T. Rowe Price (Switzerland) GmbH, Talstrasse 65, 6th Floor, 8001 Zurich, Switzerland. For Qualified Investors only.

Taiwan—This does not provide investment advice or recommendations. Nothing in this material shall be considered a solicitation to buy, or an offer to sell, a security, or any other product or service, to any person in the Republic of China.

Thailand—This material has not been and will not be filed with or approved by the Securities Exchange Commission of Thailand or any other regulatory authority in Thailand. The material is provided solely to “institutional investors” as defined under relevant Thai laws and regulations. No distribution of this material to any member of the public in Thailand is permitted. Nothing in this material shall be considered a provision of service, or a solicitation to buy, or an offer to sell, a security, or any other product or service, to any person where such provision, offer, solicitation, purchase or sale would be unlawful under relevant Thai laws and regulations.

UK—This material is issued and approved by T. Rowe Price International Ltd, 60 Queen Victoria Street, London, EC4N 4TZ which is authorised and regulated by the UK Financial Conduct Authority. For Professional Clients only.

USA—Issued in the USA by T. Rowe Price Associates, Inc., 100 East Pratt Street, Baltimore, MD, 21202, which is regulated by the U.S. Securities and Exchange Commission. For Institutional Investors only.

© 2020 T. Rowe Price. All rights reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the bighorn sheep design are, collectively and/or apart, trademarks or registered trademarks of T. Rowe Price Group, Inc.

202001-1067409