July 2021 / INTERNATIONAL EQUITIES

Japan Ups the Ante on Corporate Governance and Regulatory Reform

Revised governance codes provide framework for corporate improvement.

Key Insights

- The prioritizing of corporate sector and regulatory reform in Japan has been reflected in improved company performance and returns for investors.

- Revised stewardship and governance codes in Japan provide a road map for companies to become more economically productive and globally competitive.

- The quality of Japanese companies in terms of governance, profitability, and, ultimately, returns paid to investors has continued to visibly improve.

One of the most significant achievements of former Prime Minister Shinzo Abe’s “Abenomics” economic reform strategy has been the improvement in Japanese corporate governance standards. The government’s prioritizing of corporate sector reform—a policy pursued with equal vigor by new Prime Minister Yoshihide Suga—has been an important influence in boosting Japanese corporate performance, as well as returns for investors. Moreover, the concepts of best practice; robust environmental, social, and governance (ESG) disclosure; and improved stakeholder engagement have been recently highlighted as central to long‑term sustainability.

Measuring the impact of governance and regulatory reform is no exact science, but a key aspect of the improvement seen in Japan has been the introduction of stewardship and corporate governance codes, in 2014 and 2015, respectively. These regulatory guidelines have effectively provided a framework for improvement for Japanese companies—a road map to becoming more economically productive, globally competitive, and better positioned to attract international investment. The recent revision of Japan’s Stewardship Code and Corporate Governance Code, in 2020 and 2021, respectively, provides an opportune time to revisit the progress made to date, expectations moving forward, as well as some of our own firsthand engagement experiences with Japanese companies and regulatory bodies alike.

With this in mind, it is worth delving deeper into some of the key areas of regulatory changes, as targeted in the 2020 revision of the Japanese Corporate Governance Code.

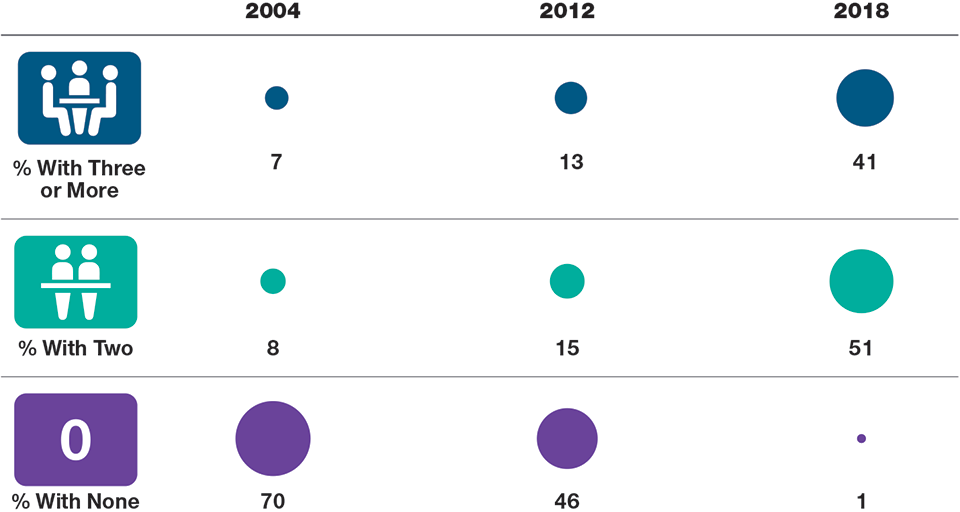

Boardroom Independence in Japan Has Improved

(Fig. 1) Percentage of TOPIX‑listed companies with independent directors

As of December 2019.

Sources: Corporate Reports, Japan Exchange Group. Data analysis by T. Rowe Price. Most recent data available.

1. Independent Directorship

Board independence levels continue to be an area of increasing importance in Japan. Governance codes currently include increased external director representation on Japanese company boards (at least two independent directors required, with a recommended level of one‑third representation) and improved diversity at both senior management and boardroom levels.

Certainly, where director independence is concerned, clear progress has been made, with more than 90% of TOPIX‑listed companies boasting two or more independent directors on their boards more recently. Companies are recognizing the value of appointing independent directors, bringing fresh ideas and new skills, and providing a wider, more diverse, range of experience and knowledge. The increase in outside representation is certainly positive and signifies crucial progress in moving Japan closer to global best practices. However, it is not enough on its own. We believe a more holistic approach is necessary, looking at a company’s whole governance structure, the separation of powers, and a board that is acting in the best long‑term interests of shareholders.

2. Board Diversity

The Japanese Corporate Governance Code includes a direct reference to diversity, stating that boards must have a level of gender and international diversity to ensure they can operate effectively. For our part, at T. Rowe Price, we have also formalized our position on gender diversity within our Proxy Voting policy, a central tenet of which is to generally vote against any Japanese company with no female board representation.

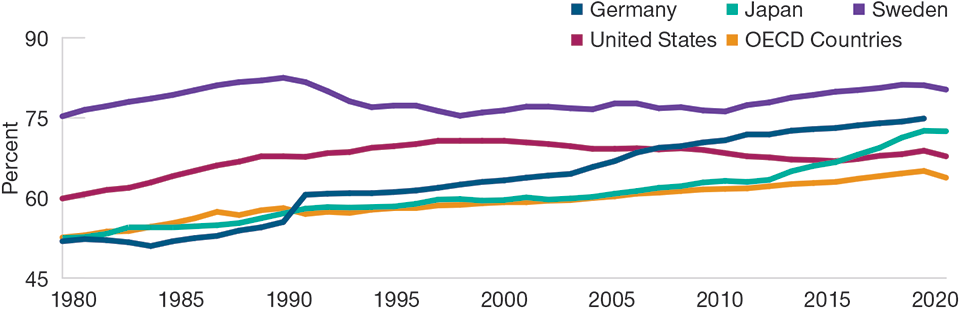

Five years ago, in 2016, the percentage of women directors represented on Japanese company boards was just 4.8%.1 However, the government has vowed to rectify this situation, targeting certain industries in particular. Greater regulatory demands have been placed on the energy and utilities sectors, for example, where companies continue to lag behind global market peers when it comes to boardroom diversity. Progress is slow, but inroads are clearly being made. In 2020, the percentage of female company directors in Japan has more than doubled, to 10.7%.1

Japan’s Female Labor Participation Rate (%)

(Fig. 2) Efforts to boost the number of women in the workforce are working

As of December 2020.

Source: OECD. OECD Stat database. 15–64 year age group female labor force participation. Data analysis by T. Rowe Price.

Beyond the boardroom, greater representation of women in senior management is also being championed by the government, seeing increased female workforce participation as a potential solution to Japan’s demographic shrinkage and a potential boost to productivity (Figure 2). Diversity is an issue that we continue to engage with companies we are invested in about extensively, providing guidance on best practices and the potential benefits to long‑term performance, as well as pushing for improved levels of disclosure.

3. Cross‑Shareholdings

Corporate cross‑shareholdings have been directly referenced in the most recent update of the Stewardship Code, calling for additional corporate disclosure on the practice. Capital misallocation and reduced market discipline resulting from complicated company cross‑shareholdings have long been viewed as among the most serious corporate governance problems in Japan. It is not uncommon for Japanese companies to own large shareholdings in other companies for reasons unrelated to pure investment purposes, for instance, in order to strengthen relationships with customers, suppliers, or borrowers. The practice, which is often criticized for supporting underperforming companies, reducing company returns on equity through inefficient capital allocation, and insulating management teams from shareholder interests and engagement, has been under regulatory scrutiny for years. And definite progress has been made. Cross‑shareholdings as a percentage of total market capitalization were well above 30% at their peak in the early 1990s, but this level has progressively declined since then and today sits at around 10%.2 This positive trend should continue to reduce the protection of underperforming management teams and free locked‑up capital so that it can be more efficiently deployed elsewhere.

In our engagement with companies on the cross‑shareholding issue, some continue to justify the practice, suggesting that such holdings are essential to maintaining relationships with customers or strengthening relations with key stakeholders. However, Japan’s updated governance codes specifically state that business relationships are no longer a valid rationale for strategic cross‑shareholdings.

Notably, the Tokyo Stock Exchange has deliberately restructured in order to force directors of companies involved in these cross‑shareholding networks to sell down these holdings. Similarly, leading proxy research provider, International Shareholder Services, is implementing strict new voting guidelines against companies that continue to engage in the practice. It has recently detailed plans to vote against management of any companies with more than 20% of net asset value tied up in cross‑shareholdings. This marks a step up in action against the practice. Where previously companies just had to disclose cross‑shareholding data, they are now being held to account.

While it will take time to eliminate cross‑shareholdings completely, with pressure from industry bodies and a regulatory focus on challenging vested interests likely boosting capital efficiency and improving returns potential, the direction of travel is positive.

4. Climate Change and Improved ESG Disclosure

Large institutional investors, and a growing number of activists, are placing ever greater emphasis on climate change in 2021, not only in Japan, but globally. With this in mind, in October 2020, the Japanese government pledged that the country would achieve net zero carbon emissions by 2050. This ambition is similarly reflected in the corporate governance regime. As a result, we are seeing an increase in carbon emissions disclosure from Japanese companies, not yet to the levels displayed in Europe, for example, but a clear improvement, nonetheless. That said, our own engagement with Japanese companies on ESG disclosure reveals an interesting paradox. While Japan leads the world in terms of the number of companies signed up to the Task Force on Climate‑Related Financial Disclosures—the globally recognized benchmark—until the recent net zero announcement, most companies’ disclosure reporting was actually fairly average, both in terms of level of detail as well as a lack of actionable items.

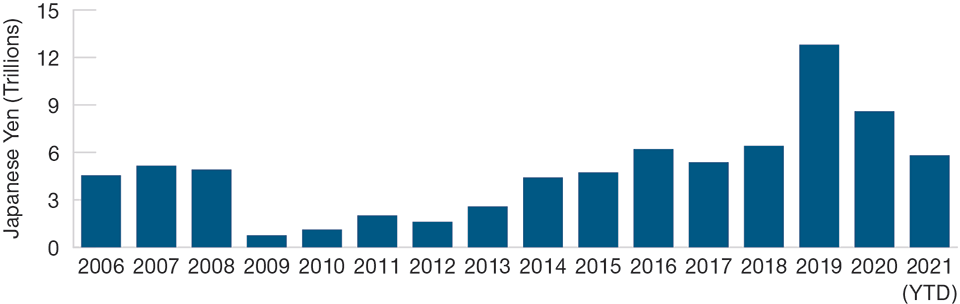

Improved Shareholder Returns

Japanese Companies Have Delivered Increased Shareholder Returns

(Fig. 3) Share buybacks announced by TOPIX‑listed companies*

As of March 31, 2021.

*Data exclude financials and utilities. Shows cumulative share buybacks net of share issuance. Based on governance reports submitted by mid‑July.

Sources: Corporate Reports, TOPIX Index: TOPIX—Tokyo Stock Exchange, Inc. Data analysis by T. Rowe Price.

The focus on corporate sector reform has been a key influence in the rise in company earnings and profitability seen in recent years. Japanese companies are allocating capital more efficiently; instead of maintaining inefficient balance sheets with high cash stockpiles, companies are putting their sizable reserves to work by buying back shares and paying higher dividends.

And evidence of the improvement in shareholder returns is plain to see. The level of share buybacks by Japanese companies reached a record high in 2019, as both regulators and management teams looked to deliver higher returns to shareholders.

A Final Word

The quality of Japanese companies, in terms of governance standards, profitability, and, ultimately, returns paid to investors, has continued to visibly improve, closing the gap with European and U.S. equity markets. Companies have been allocating capital more efficiently, paying higher dividends, and increasing share buybacks, and these improved returns have been attracting greater foreign investment.

We believe this focus on improvement will only gather pace, creating both risks and opportunities for companies as they respond to, or fall behind, the pace of change. We believe that an active management approach can be quick to identify these potential winners and losers and allocate investment accordingly within an investment portfolio.

At T. Rowe Price, our company engagement programs have always been driven by our fundamental research and supported by local market expertise. In recent years, our research platform has been bolstered by substantial investment in our dedicated ESG research team, which provides proprietary analysis to integrate into our investment decision‑making. This provides us with a deeper understanding of potential ESG risks or opportunities in our investment universe and identifies prospects for engagement among our portfolio holdings. Combined with the deep expertise of our nine‑member Japanese equity research team, we believe this positions us well to actively respond to the ever‑evolving investment needs of our clients.

Important Information

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

USA—Issued in the USA by T. Rowe Price Associates, Inc., 100 East Pratt Street, Baltimore, MD, 21202, which is regulated by the U.S. Securities and Exchange Commission. For Institutional Investors only.

© 2025 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.