January 2021 / INVESTMENT INSIGHTS

End of the Fed’s Credit Support Facilities Is Positive

Risk of unintended imbalances in the credit market is lower

Key Insights

- We believe the Fed’s credit facilities met the goal of restoring liquidity and their end is positive for the long‑term health of the corporate credit market.

- Fiscal policy has taken the leading role in supporting the broader recovery in the economy and in corporate fundamentals.

- Spread dispersion across industries remains, which presents opportunities for credit selection, particularly as an uneven recovery likely takes hold throughout 2021.

The success of the Federal Reserve’s emergency intervention in March 2020 played a crucial role in stabilizing and improving liquidity in U.S. credit markets. The cessation of the Fed’s corporate credit facilities, in our opinion, lowers the risk of unintended imbalances within credit markets that could potentially become a larger problem in the future if left unchecked. With the Fed stepping back on direct corporate credit market support, fiscal policy has taken the leading role in supporting the broader recovery in the economy and in corporate fundamentals. There is still meaningful credit spread1 dispersion within the investment‑grade corporate bond market, presenting attractive opportunities for credit selection, particularly as an uneven recovery likely takes hold through 2021.

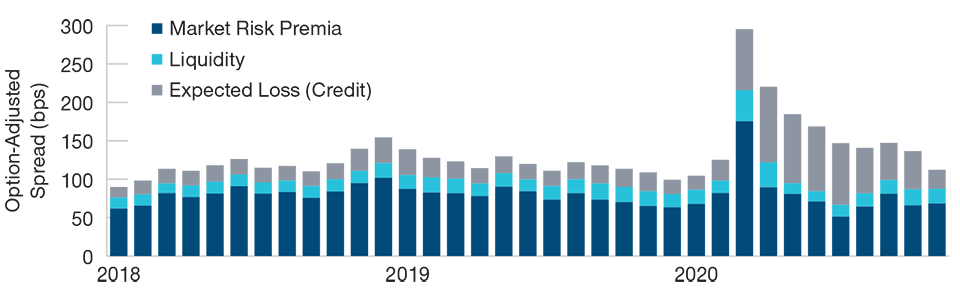

Components of Total Spread

With the magnitude of the COVID‑19 crisis still unfolding, the credit markets faced enormous pressure and to a large extent nearly ground to a halt in mid‑March 2020. On March 23, the Fed announced that it would establish primary and secondary corporate credit facilities to acquire investment‑grade corporate bonds with five years or less to maturity as well as exchange‑traded funds (ETFs) that hold investment‑grade corporates.

Our quantitative team analyzed the composition of credit spreads prior to the onset of the pandemic, categorizing total spread into three key risk premium components: liquidity, credit, and market.2 These three risk premiums help enhance our understanding of how credit spreads are compensating investors and proved insightful for evaluating the effects of the Fed’s corporate credit facilities. The components of total spread each behave differently at different points in a credit cycle, vary in length, and are impacted by different market forces. In our work, we have found that Fed actions taken to alleviate market stress primarily influence the liquidity risk premium.

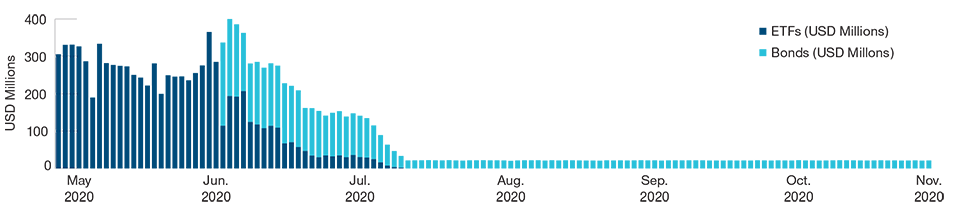

As shown in Figure 1, the liquidity risk premium peaked in March 2020. It had largely returned to normal by June after the Fed implemented the credit facilities and started actively participating in the market (see Figure 2). Since June, the credit risk premium has continued to compress as the economy started to recover and the outlook for corporate fundamentals improved. In the end, the Fed proved to be a very small buyer in the credit markets; nevertheless, we believe the central bank achieved its objectives.

March 2020 Liquidity Risk Premium Peak

(Fig. 1) Corporate bond index1 credit spread decomposition

As of November 30, 2020.

For illustrative purposes only.Source: Calculated by T. Rowe Price. Data used in calculation is sourced from Bloomberg Index Services Ltd. Copyright 2020, used with permission. (See Additional Disclosure.)Spread decomposition based on default rates, liquidity indicators such as bid and ask prices, and volatility of index components.

1 Bloomberg Barclays U.S. Corporate Index.

Corporate Credit Facilities Allowed to Expire

In November 2020, the Treasury instructed the Fed to let the corporate credit facilities expire on December 31. The Treasury allowed the Fed to continue its commercial paper, money market, and bank collateral facilities until March 31, 2021.

Some market participants have suggested that the Treasury and the Fed extend all support facilities. We, however, believe the cessation of corporate credit facilities is a good outcome for both the short and long terms. The elimination of these programs reduces the risk of exogenous influences on market pricing sending false signals to both issuers and investors. A prolonged period of this type of misinterpreted activity could potentially lead to capital misallocation and rising credit imbalances. If left unchecked, this could have the unintended consequence of potentially increasing credit market fragility and the risk of another extreme event that damages market function.

Fed Buying Slowed After June 2020

(Fig. 2) Daily pace of SMCCF1 bond and ETF purchases

As of November 12, 2020.

Source: Federal Reserve.

1 Secondary Market Corporate Credit Facility.

Outlook for 2021

With the Fed’s more limited role, fiscal policy actions will take on greater significance in the broader economic revival that we expect in 2021. We believe fiscal actions, such as the USD 650 billion Paycheck Protection Program, have already had a greater impact on the recovery than the Fed’s corporate credit facilities.

We are seeing material improvements in third‑quarter corporate profitability, which has reduced corporate solvency risk. According to J.P. Morgan, third‑quarter corporate revenues (excluding the energy sector) were up 0.6% from the previous quarter and 0.4% from the period a year earlier. In addition, overall profitability was a steady 30.4%, a 0.6% increase from 2019’s third quarter. These metrics indicate a rebound from the trough levels of the second quarter of 2020.

It is encouraging that a USD 900 billion relief act was implemented in December with bipartisan support. As part of the stimulus agreement, the Fed will not be permitted to restart its emergency lending programs—including the corporate credit facilities—without approval from Congress. We expect the new U.S. administration will lead action toward further fiscal stimulus in the first half of 2021.

Dispersion in Spreads Across Industries

We expect credit market technicals to improve from 2020 as we anticipate lower net new issue volume and ongoing support for higher-yielding corporate securities versus government bonds with lower—or even negative—yields. There is still meaningful dispersion in credit spreads across certain investment‑grade corporate industries and issuers, which presents attractive opportunities for credit selection. An uneven recovery from the COVID-19 pandemic in 2021 could create more opportunities to find relative value in the asset class.

We currently find select bonds in the real estate investment trust (REIT), energy, and travel and leisure segments attractive. We believe these industries still have not fully recovered and anticipate they will benefit from improving 2021 fundamentals. In REITs, we prefer bonds issued by companies focusing on apartments as well as industrial and health care-related commercial properties. In energy, our credit analysts have been finding opportunities in higher‑quality credits in the exploration and production industry, where expected consolidation should support fundamentals. As always, we will rely on our deep fundamental research platform to uncover opportunities moving forward.

WHAT WE’RE WATCHING NEXT

While we focus on credit research and selection to inform broad positioning in our investment‑grade corporate portfolios, we also consider positioning along the yield curve. We currently see limited room for spread compression in shorter‑maturity notes, although they offer some defensive characteristics. Longer‑term bonds, including 10‑year paper, provide more potential for appreciation from narrowing spreads at the expense of higher interest rate risk.

Key Risks—The following risks are materially relevant to the strategy highlighted in this material:

Debt securities could suffer an adverse change in financial condition due to a ratings downgrade or default, which may affect the value of an investment. Fixed income securities are subject to credit risk, liquidity risk, call risk, and interest rate risk. As interest rates rise, bond prices generally fall.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.