August 2022 / INVESTMENT INSIGHTS

Are Frontier Markets Still the Great Untapped Opportunity?

This dynamic part of the global equity market remains significantly neglected

Key Insights

- Frontier markets are highly inefficient, with good opportunities to find companies that benefit from strong structural growth.

- The region is a natural risk diversifier, as frontier market returns have a low correlation to those of developed and emerging markets.

- An allocation to frontier markets completes an investor’s global exposure, providing unique access to 36%1, 2 of the world’s population and 15%2 of its GDP.

Amid a backdrop of heightened financial market uncertainty, we sat down with Johannes Loefstrand, portfolio manager of the T. Rowe Price Frontier Markets Equity Strategy, to ask seven key questions about this dynamic, yet underinvested, part of the global equity market.

Why consider investing in frontier markets?

Frontier markets generally are at earlier stages of macroeconomic and capital market development than developed and emerging markets. As a group, these bourgeoning economies tend to have lower labor costs and younger populations and are less burdened by debt. Individually, they offer a diverse landscape, with almost every frontier country offering its own blend of opportunities and risks. Demographics; infrastructure investment; macroeconomic reform; political stability; regulatory framework; and environmental, social, and governance (ESG) advancement—all are typically long‑term structural growth drivers that should continue to play out in frontier market countries over a multi‑decade time frame.

Frontier markets in our investible universe also account for 36%1, 2 of the world’s population and 15%2 of its total gross domestic product (GDP), yet they make up just 0.3%2 of the total global market capitalization (Figure 1). The United Nations also estimates that nearly half of the global population will reside in frontier markets by the middle of this century.2 For investors looking for complete global investment exposure, this represents a dynamic and growing portion of the global universe that is not covered by the main market indexes.

Frontier Markets Are Underrepresented in Terms of Global Market Capitalization

(Fig. 1) Compared with GDP/population weightings, this imbalance is striking

As an asset class, frontier markets have historically provided solid long‑term performance, broadly comparable with the returns from longer‑established, more mature equity markets. Importantly for global capital allocators, frontier market performance tends to have a low correlation with the returns from developed and even emerging markets. For example, in 2021, the MSCI Frontier Markets Index returned 20% for the year, compared with a -2% return from the MSCI Emerging Markets Index (both in USD).3

This is partly due to lower levels of foreign investment as well as minimal allocations of passive investment. This means that frontier markets are one step removed from the powerful forces of global investment flows and, therefore, should be less impacted by large risk‑on/risk‑off allocation moves. Consequently, an allocation to frontier markets as part of a broader global portfolio can help lower overall portfolio risk and volatility since these markets tend to perform more independently.

How do you approach the construction of your portfolio?

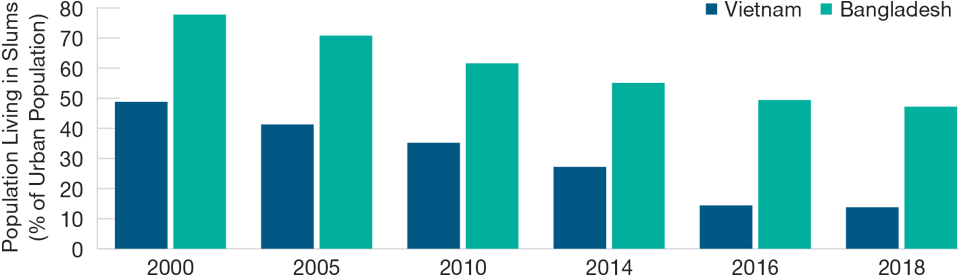

The macro environment is hugely important in managing risks within frontier markets, as a range of contrasting inputs must be evaluated. Global poverty, for example, is steadily falling, resulting in material improvement to living standards in many frontier market countries (Figure 2). At the same time, however, it is estimated that some 700 million people around the world are still living in extreme poverty.4

Living Standards Have Been Materially Improving in Many Frontier Countries

(Fig. 2) Proportion of urban population living in slums (%)

As of December 31, 2018. Latest data available.

Sources: World Bank/Haver Analytics.

Once a structurally attractive country is identified, we look for structural themes underpinning a particular industry, or sector, that can potentially drive sector growth at a faster rate than GDP. From here, detailed fundamental analysis informs our decision‑making at the individual company level. By going out into the field, seeing the companies operate firsthand, and speaking with management teams in person, our aim is to find robust, well‑managed businesses that are sustaining or taking market share.

Meanwhile, our valuation process is rigorous. Positively for stock‑picking investors, frontier markets tend to trade at substantial discounts, relative to global developed and emerging market peers. And within this opportunity set, we consistently find stocks that are mispriced—in our view, often extremely so.

Ultimately, we believe that this process helps us to build a portfolio that reflects both the long‑term opportunity of frontier markets and the pricing inefficiency that tends to characterize frontier companies.

Can you explain how your macro framework filters down to the individual stock level?

There is a general misconception within frontier markets—specifically that people tend to underestimate just how strong many of these economies are. In fact, 18 of the 20 fastest‑growing economies in the world over the past decade were frontier countries,5 offering an exciting investment opportunity. Indeed, many of the world’s weakest, more unstable, economies are also to be found among frontier countries, such as Nigeria and Sri Lanka; however, we do not have exposure to these countries.

To help us focus on the strong and avoid the weak economies, we use a macro framework to help us navigate risk from the outset. This is built around three key anchors, with each frontier country assessed for:

(1) Fiscal strength—countries are not spending more than they can afford.

(2) External strength—countries’ debt levels are manageable.

(3) Institutional strength—sufficient checks and balances are in place to sustain a country’s economic path.

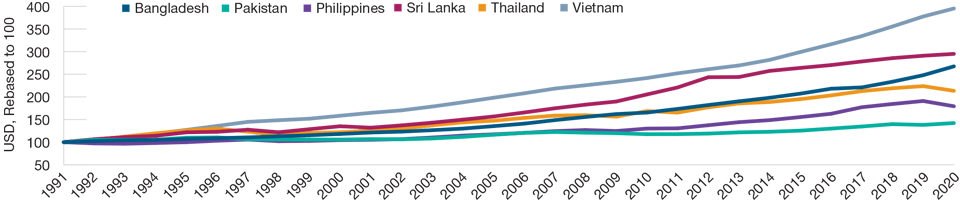

Productivity Growth in Vietnam Has Exceeded ASEAN Nations

(Fig.3) This is underpinning a rapidly expanding middle class

As of December 31, 2020, latest data available.

Productivity is depicted as GDP per person employed.

Source: International Labor Organization: Key Indicators of the Labor Market database/Haver Analytics. Data analysis by T. Rowe Price

We classify each frontier country in our universe into one of four categories: frontier tigers, regular frontiers, unanchored frontiers, and wealthy frontiers. Those countries that are supported by solid anchors and show evidence of a sustained takeoff in growth—classified as “frontier tigers”—are where we tend to focus most of our efforts.

Can you highlight a particular frontier tiger country that you currently like?

Vietnam is in many ways the epitome of a frontier tiger country. It is a deep and liquid market, boasting nearly 1,700 listed companies and trades, on average, more than USD 1 billion every day.

The dynamic economy has shown clear evidence of being on a path of sustained structural growth. Vietnam joined the World Trade Organization in 2007, and strong growth in exports has seen the country make significant progress on the path to international integration.

Growth in productivity has also exceeded other ASEAN countries over the past decade (Figure 3), underpinning a rapidly expanding middle class. Vietnam is evolving into a classic consumer economy, characterized by youthful demographics, accelerating urbanization, and rising per capita disposible income. Vietnam’s high level of education, with an above‑OECD-average literacy rate, is feeding through to higher‑skilled jobs in specialized sectors and industries.

Currently, the Vietnam Ho Chi Minh Index is trading at a 10.5x forward price/earnings (P/E) ratio (as of June 30, 2022) versus a historical average of a 13x forward P/E ratio,6 despite what we believe are above‑average growth prospects. GDP growth is forecast to rebound to approximately 7% this year, while inflation is still at a manageable 4% level. In contrast to many other countries, the government was not compelled to stimulate the economy during the pandemic, so we have not seen the same buildup of imbalances or debt burdens experienced in some countries.

What are some of the key risks of investing in frontier markets?

Frontier markets are inherently riskier than developed and advanced emerging markets, given the earlier stage of their economic and capital market development. This is why the application of a macro framework at the outset is an essential part of our process.

Meanwhile, there is an argument to be made that frontier markets are potentially less volatile than emerging markets. This is due to the large number of countries within the frontier market universe, all at different stages of economic development and growth and powered by different industries and structural drivers. This makes for a diverse, domestically driven universe that is less affected by global investment flows than emerging markets. As such, performance also tends to have a low correlation.

Poor liquidity is the criticism most often leveled at frontier markets. And given the more limited investment flows, frontier markets do tend to be less liquid than their developed and emerging market peers. However, less liquid is a long way from being problematic or constrained. With liquidity continually improving in these markets, a lot of the noise around “liquidity risk” seems to be rooted in history and perception rather than today’s reality.

How advanced are frontier markets in terms of ESG progress? Does this enter into your decision‑making?

ESG considerations have long been a central component of our investment process, given the fact that regulatory regimes and legal structures in frontier market countries are generally less established.

There is also wide divergence in the level of ESG progress and ambition between frontier market countries as well as individual companies. And the impact on performance of good ESG actors, compared with laggards, tends to be magnified in frontier markets.

At a broad level, we actively seek companies that are participating in the betterment of society. This focus naturally steers us toward more ESG‑progressive sectors and industries, such as health care, renewable energy, financial inclusion, and information technology services and digitalization.

Providing capital to frontier market companies can have a meaningful, even transformational, effect, not only on the businesses themselves, but also on the communities they operate in, positively impacting livelihoods. For example, a bank that we own in Bangladesh has potentially supported the financial inclusion of millions of people through its core and subsidiary business operations—from enabling people to send money electronically in times of distress through to providing microloans to those looking to capitalize on a particular idea or opportunity.

What is your view on the near‑term outlook for frontier markets?

The outlook for frontier markets is nuanced and demands close attention to the dynamics of each country. Countries such as Kenya, Sri Lanka, Nigeria, and Pakistan, for example, face a more challenging environment at a time when their respective outlooks are weakening. For various reasons, these countries have come under pressure in recent years, and the soaring cost of energy and other commodity prices has heightened their vulnerability. With the Russia‑Ukraine crisis set to keep upward pressure on commodity prices for the foreseeable future, the impact will be deeply felt by many frontier market countries.

In contrast, stronger, more stable economies, such as Vietnam, Bangladesh, the Philippines, and Romania, are expected to do well relative to most frontier peers amid a challenging global environment over the next 12 to 18 months. They should benefit from generally low levels of debt and robust economic growth keeping their currencies stable.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

August 2022 / INVESTMENT INSIGHTS