November 2021 / INVESTMENT INSIGHTS

Change in Political Leadership and the Outlook for Japan

Prospects for stocks look bright amid expected policy continuity

Key Insights

- Given tentative moves toward economic reopening and supportive political developments, we believe the prospects for Japanese stocks look bright.

- Our positive outlook is predicated on social and economic normalization following the coronavirus pandemic and expectations of policy continuity under new leadership.

- The high degree to which Japanese corporate profits are levered to the global economic recovery adds to our optimism about the country’s stock market.

Japan has had a challenging year. After outperforming in 2020, the country has disappointed investors in 2021 due in part to the delayed rollout of its COVID‑19 vaccination program, as well as the public’s negative reaction to the government’s decision to host the Olympics amid concerns about the spread of the coronavirus. With his popularity hovering around all‑time lows, these factors ultimately contributed to the decision by Prime Minister Yoshihide Suga to resign in September.

Taking stock, however, the Olympics are now behind us, Japan’s vaccination drive has overtaken that of many developed market peers, and there have been some positive political developments—against this backdrop, Japan has started to outperform.

In a recent webinar, Portfolio Manager Archibald Ciganer shared his thoughts on the state of play in Japan—in particular, what the leadership change means for investors and whether it is likely to derail any of the positive reforms that the country has pursued in recent years. He also explained how he had been managing his portfolio in this challenging period and discussed where he sees future opportunities. The following is a summary of the question and answer session.

What is life in Japan currently like with respect to the pandemic?

Things are gradually returning to normal, and the economy should slowly reopen from here. The states of emergency were fully dropped for the first time in over six months at the end of September, and trains, shops, bars, and restaurants are already filling up.

Japan was late to roll out an effective COVID‑19 vaccination program due to challenges in gaining regulatory approvals for vaccines, securing sufficient supplies, and administering the rollout. However, since May, the country has caught up rapidly, and its vaccination rate (the percentage of the population that is fully vaccinated) is now higher than that of the U.S. and Europe, meaning that the impact on society and the economy of any new uptick in cases should be more manageable.

What impact is the recent change in leadership likely to have?

Following the resignation of Suga, former Foreign Minister Fumio Kishida was elected leader of the ruling Liberal Democratic Party (LDP) at the start of October after defeating vaccination minister Taro Kono and two other candidates in the leadership runoff, effectively becoming Japan’s new prime minister.

The result disappointed markets and the domestic populace, which had hoped for accelerating change under perceived reformer Kono. Kishida was viewed as the continuity candidate and a safe pair of hands, who was favored by the powerful group of LDP lawmakers who elected their new leader.

Elections for the powerful lower house of parliament were held on October 31, with the LDP retaining control given its large majority and single-digit support rates for Japan’s opposition parties. The party’s focus heading into the election had been on minimizing losses, following Suga’s resignation and perceptions that his government’s response to the pandemic had been badly managed. Elections for the upper house of parliament will be held before summer next year. We do not anticipate that there will be significant changes between now and then that could result in the loss of further support for the LDP.

Ultimately, we regard the election of Kishida as somewhat of a missed opportunity to accelerate change. The power structure within the LDP (which includes former Prime Minister Shinzo Abe among its key figures) is unchanged, and the “Abenomics” program of aggressive monetary easing, fiscal stimulus, and structural reform remains on track. The pace of reform is likely to be steady rather than spectacular from here, in our view. We are not concerned about recent media speculation about Kishida’s potential policies, such as an increase to the country’s capital gains tax (which he confirmed is not being considered).

Have you made any changes to the portfolio as a result of recent developments?

We have not made any substantial changes to the portfolio and continue to do what we have always done: bottom-up stock picking on an individual thesis basis.

In terms of positioning, we have moved toward less cyclical exposure as the recovery was priced in early and valuations reflected that. We introduced a lot of cyclicals in mid‑2020 ahead of the global recovery that came through and most of the stocks had outperformed significantly, moving to valuation levels we no longer deemed attractive in some cases.

Overall, given a more stable environment, most sectors appear priced in line with fundamentals. There are some pockets of weakness in services; however, if the domestic economy reopens quickly and foreign tourists come back soon, these sectors could still outperform this year.

What is your current view on small‑cap companies?

The relationship between small‑ and large‑cap stocks in Japan tends to be cyclical, so our typical approach is to be invested in both. Small‑cap stocks can offer the potential of outsized returns, while large‑cap stocks tend to offer transformation qualities and can provide a more stable return profile at a lower risk level.

We hold several small‑cap companies in the portfolio, and any uptick in small‑cap sentiment should help boost performance.

What have been the drivers of portfolio performance?

Portfolio performance this year has been disappointing (it is only the second year of underperformance since Archibald Ciganer started managing the strategy in December 2013, the first being 2014). Much of this year’s underperformance is a reversal of 2020 when growth outperformed value significantly and the portfolio registered sizable outperformance.

We have had a fairly unique scenario when the correlation between industrials and financials turned negative, which is extremely uncommon. We seek to structure the portfolio in such a way that it is not overly affected by a macro cycle. We have had an overweight position in industrials and an offsetting underweight position in financials, in the hope that when financial stocks outperform, industrials will too, in order to try to provide some protection from a macro upside.

While this approach has tended to benefit portfolio performance, this year, interest rate expectations rose on global reflation prospects, leading financials to outperform, while, at the same time, the spread of the delta variant of the coronavirus led to supply chain issues and brought industrial production to a halt in many parts of the world. We expect the correlation between industrials and financials to turn positive again as the delta wave subsides.

Are you still excited by Japan’s digital transformation?

We continue to seek out opportunities that can benefit from Japan’s digital reform. The country has woken up to the fact that it is behind its developed market peers when it comes to digitalization, and it is catching up quickly—this is a government priority, underpinned by the fact that digital reform is needed to move the economy forward. Given Japan’s shrinking workforce, growth will need to come from better productivity, including the more extensive use of digital technology.

The launch of Japan’s first Digital Agency in September was a significant step toward upgrading the archaic systems used by most local and public entities. The Digital Agency is a huge project that should set a standard for innovation in Japan and, we believe, push corporations to modernize more quickly.

The agency is being resourced from the private sector rather than being run by bureaucrats, which is a positive break from the past. We believe these measures will have a halo effect, accelerating the pace of digital transformation and creating ample multiyear investment opportunities. We do not believe the change in Japan’s leadership will alter this course in any way.

Has the pandemic derailed Japan’s corporate governance reforms?

We believe Japan’s corporate governance reforms remain on track, and we continue to see continued improvement in standards.

Capital allocation is changing and is likely to be a powerful driver of stock prices over the next stage of the cycle. Although we saw fewer buybacks over the past year as a result of cash flow shortages caused by the pandemic, the reduction is lower than we would have expected and much less than in previous crises. Japan might not reach the record level of share buybacks it registered in 2019 this year, but we expect companies to resume the pace of buybacks once the impact of the pandemic subsides.

We have seen fewer companies cutting dividends than we did compared with the 2008–2009 global financial crisis. Regarding return on equity (ROE), Japanese corporate earnings are highly geared to the global economy, more so than the European corporate sector, for example. Japan’s ROE lags Europe, but we expect it to catch up. It will be more difficult to reach U.S. levels of ROE, where the focus on shareholder return and shareholder pressure is greater and where there are simply more globally leading companies.

What is your view on Japanese equity valuations and the outlook for the market?

In our view, the consensus probably underestimates the earnings impact of the recovery and Japan’s operating leverage to the global economy. We think profits will surprise to the upside and the market will react to that, with consensus earnings moving up.

Japan’s accelerating COVID‑19 vaccination program is likely to continue lending support to the stock market, while added stimulus measures under new political leadership could provide a further tailwind. Improved governance is also contributing to our positive long‑term outlook.

We believe the anticipated global economic recovery will continue to build and broaden through 2021 and beyond and that we will slowly return to some semblance of normality. Given Japan is one of the most cyclical and open markets, highly levered to the health of the world economy, we believe it will be a major beneficiary of the prospective global recovery.

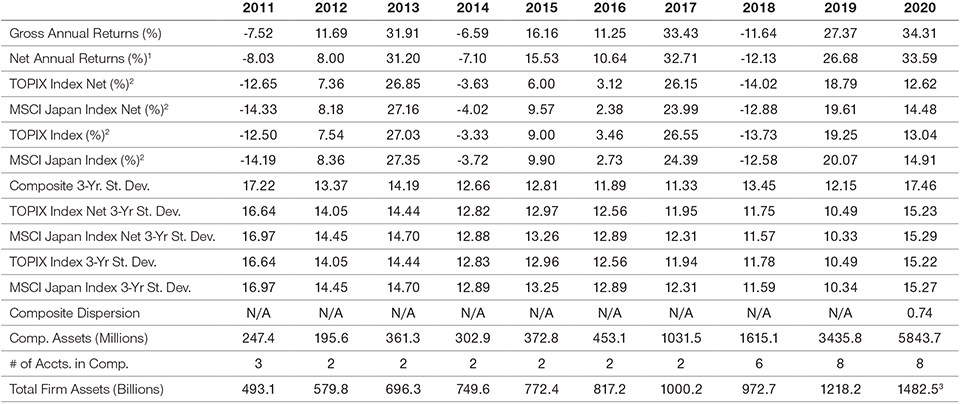

GIPS® Composite Report

Japan Equity Composite

Period Ended December 31, 2020

Figures Are Shown in U.S. dollar

1Reflects deduction of highest applicable fee schedule without benefit of breakpoints. Investment return and principal value will vary. Past performance is not a reliable indicator of future performance. Monthly composite performance is available upon request. See below for further information related to net of fee calculations.

2 Primary benchmark is TOPIX TSE First Section Index Net and secondary benchmark is MSCI Japan Index Net. Effective June 1, 2019, the composite’s benchmark changed from gross to net of withholding taxes. The change was made because the firm viewed the new benchmark to be more consistent with the tax impacts of the portfolios in the composite. Historical benchmark representations have been restated.

3 Preliminary—subject to adjustment.

T. Rowe Price (TRP) claims compliance with the Global Investment Performance Standards (GIPS®) and has prepared and presented this report in compliance with the GIPS standards. TRP has been independently verified for the 24-year period ended June 30, 2020 by KPMG LLP. The verification report is available upon request. A firm that claims compliance with the GIPS standards must establish policies and procedures for complying with all the applicable requirements of the GIPS standards. Verification provides assurance on whether the firm’s policies and procedures related to composite and pooled fund maintenance, as well as the calculation, presentation, and distribution of performance, have been designed in compliance with the GIPS standards and have been implemented on a firm wide basis. Verification does not ensure the accuracy of any specific composite presentation. TRP is a U.S. investment management firm with various investment advisers registered with the U.S. Securities and Exchange Commission, the U.K. Financial Conduct Authority, and other regulatory bodies in various countries and holds itself out as such to potential clients for GIPS purposes. TRP further defines itself under GIPS as a discretionary investment manager providing services primarily to institutional clients with regard to various mandates, which include U.S., international, and global strategies but excluding the services of the Private Asset Management group. The minimum asset level for equity portfolios to be included in composites is $5 million and prior to January 2002 the minimum was $1 million. The minimum asset level for fixed income and asset allocation portfolios to be included in composites is $10 million; prior to October 2004 the minimum was $5 million; and prior to January 2002 the minimum was $1 million. Valuations are computed and performance reported in U.S. dollars.

Gross performance returns are presented before management and all other fees, where applicable, but after trading expenses. Net of fees performance reflects the deduction of the highest applicable management fee that would be charged based on the fee schedule contained within this material, without the benefit of breakpoints. Gross and net performance returns reflect the reinvestment of dividends and are net of nonreclaimable withholding taxes on dividends, interest income, and capital gains. Effective June 30, 2013, portfolio valuation and assets under management are calculated based on the closing price of the security in its respective market.

Previously portfolios holding international securities may have been adjusted for after-market events. Policies for valuing portfolios, calculating performance, and preparing compliant presentations are available upon request.

Dispersion is measured by the standard deviation across asset-weighted portfolio returns represented within a composite for the full year. Dispersion is not calculated for the composites in which there are five or fewer portfolios.

Some portfolios may trade futures, options, and other potentially high-risk derivatives which generally represent less than 10% of a portfolio.

Benchmarks are taken from published sources and may have different calculation methodologies, pricing times, and foreign exchange sources from the composite.

Composite policy requires the temporary removal of any portfolio incurring a client initiated significant cash inflow or outflow greater than or equal to 15% of portfolio assets. The temporary removal of such an account occurs at the beginning of the measurement period in which the significant cash flow occurs and the account re‑enters the composite on the last day of the current month after the cash flow. Additional information regarding the treatment of significant cash flows is available upon request.

The firm’s list of composite descriptions, a list of limited distribution pooled fund descriptions, and a list of broad distribution pooled funds are available upon request. GIPS® is a registered trademark of CFA Institute. CFA institute does not endorse or promote this organization, nor does it warrant the accuracy or quality of the content contained herein.

A portfolio management change occurred effective December 27, 2013. There were no changes to the investment program or strategy related to this composite.

Some portfolios may trade futures, options, and other potentially high-risk derivatives which generally represent less than 10% of a portfolio.

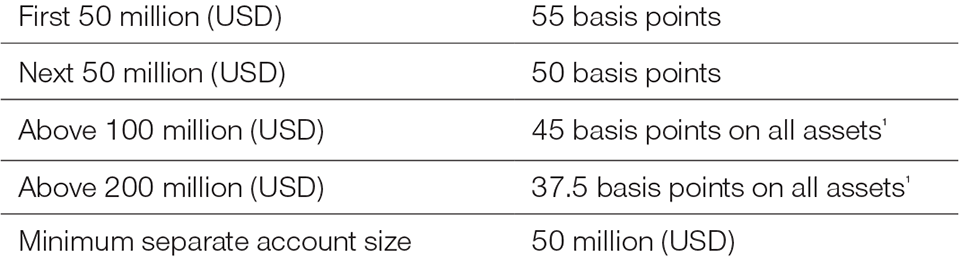

Fee Schedule

Japan Equity Composite. The Japan Equity Composite seeks long-term capital appreciation primarily through investment in large-, mid-, and small-cap companies traded in Japan markets, with faster earnings growth and reasonable valuation levels relative to market/sector averages. The market cap of holdings within these portfolios will typically be between $4 and $20 billion. (Created June 2006; incepted December 31, 1995.)

1A transitional credit is applied to the fee schedule as assets approach or fall below the breakpoint.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

November 2021 / INVESTMENT INSIGHTS