May 2021 / INVESTMENT INSIGHTS

Lessons Learned: Repeat of Taper Tantrum Unlikely

The Fed may announce first asset tapering steps this summer.

Key Insights

- The Fed is likely to announce a tapering of its asset purchases well before it begins raising rates.

- With April’s pullback in job growth, a signal from the Fed that it is beginning to plan for tapering has likely been delayed until the summer.

- While some market volatility might be expected as the Fed begins to remove accommodation, we do not anticipate a repeat of 2013’s “taper tantrum.”

Should the health of the U.S. economy continue to improve at its current pace in the coming months, investors will have to prepare for a gradual normalization in Federal Reserve policy. Exactly how the Fed will respond remains uncertain, however, as does the strength of the economic recovery. Here, we outline our working assumptions on both questions, as well as how we are positioning our portfolios in response.

Tapering Well Before Rate Hikes

As the Fed gradually withdraws extraordinary monetary accommodation, it seems highly likely that policymakers will follow a similar sequence to the one used following the global financial crisis (GFC) of 2008–2009. We believe that well in advance of raising rates, the Federal Open Market Committee (FOMC) will first wind down the central bank’s massive monthly purchases of Treasuries (USD 80 billion) and agency mortgage-backed securities (USD 40 billion), removing some downward pressure on long-term interest rates.

The Fed has specified that these steps will be taken in response to realized economic outcomes: Asset purchases will not be reduced “until substantial further progress has been made toward the Committee’s maximum employment and price stability goals.” The Fed has also stated that achieving this progress will “take some time” but that the FOMC intends to communicate well in advance when it has judged the economy to be “on track” to substantial further progress.

Threshold Rate of Labor Market Progress

What rate of improvement, if sustained, would cumulate to something that the FOMC would consider “substantial further progress”? And how many months of such improvement might the committee have in mind when it judges that “some time” has elapsed?

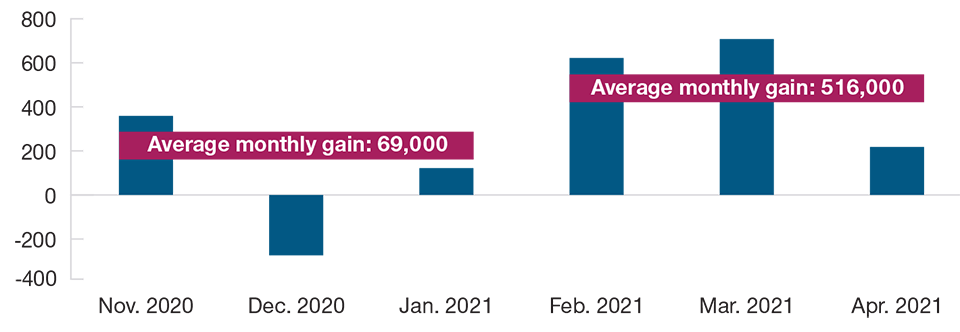

Job Growth Accelerated in February

(Fig. 1) Monthly change in private nonfarm payrolls (thousands)

As of April 30, 2021.

Source: U.S. Bureau of Labor Statistics, Haver Analytics

Chair Jerome Powell made clear in a March press conference that the pace of employment gains from November 2020 through January 2021—an average of 69,000 private sector jobs added per month—was not sufficient. February and March showed substantial improvement, with gains of 622,000 and 708,000, respectively. Powell spoke approvingly of the latter at April’s press conference, but he was surely less enthused by April’s 218,000 outturn.

Tapering Signal at July Meeting?

The Fed is basing policy on outcomes, not forecasts. Nonetheless, the FOMC’s latest Summary of Economic Projections suggests that a majority of participants anticipate the liftoff of rates in 2024. Working backward from there, the post-GFC timeline suggests that the Fed would want the option to begin tapering early next year:

If policymakers think that a rate hike in 2024 is more likely than not, the post-GFC template would have asset purchases completed by early 2023. Asset purchases were tapered to zero over the first 10 months of 2014, with the first rate hike coming in December 2015.

If the taper takes a year, it would have to be announced over the turn of the year to begin in early 2022.

Roughly six months’ lead time that tapering is coming into view suggests the first signal is likely to come in the months immediately ahead. Following the GFC, policymakers first signaled that the taper was coming into view in May 2013, when then Fed Chair Ben Bernanke mentioned the possibility of tapering the central bank’s USD 85 billion in monthly asset purchases over “the next few meetings.” This turned out to be seven months ahead of the FOMC’s announcement in December that tapering would commence in January.

Of course, this schedule is data-dependent, not date-dependent, and supposes that if private sector job gains return in May to a pace roughly in line with the February to March average of 665,000, the FOMC is likely to acknowledge that the labor market is “on track” to “substantial further progress” at its July 28 meeting.

This would give the Fed the option to begin tapering as soon as early next year, with eight to 10 months having constituted “some time” to achieve “substantial further progress.” Opening the door for an early-2022 taper would also reduce the risk that a faster inflation flare-up will compress the interval between the wind-down of asset purchases and the beginning of rate hikes.

Taper Tantrum Unlikely, but Risks Remain

To be sure, there are risks in this and any other approach the Fed might take. Bernanke’s comments in May 2013 were widely blamed for setting off a “taper tantrum” in the form of several months of high volatility in financial markets. While a government shutdown that October and other factors were probably also at work, Powell, who had recently joined the Fed, later remarked that the taper tantrum left “scars” on everybody working at the Fed.

A repeat seems unlikely, in part because investors have the 2013 precedent in mind. The strong consensus of the New York Fed’s survey of market participants and primary dealers is that tapering will begin in the first quarter of 2022. If this is an accurate reflection of market expectations, then a summer “progress report” is not likely to induce a taper tantrum of the kind seen in 2013. Investors will also probably remain mindful that it took the Fed two and a half years to begin raising rates after Bernanke’s first comments.

The Fed’s timing may still come under scrutiny, however. If policymakers announce the first steps toward tapering amid a more gradual pace of labor market improvement than had previously been expected, they risk being viewed as acting preemptively. They may also be seen as validating worries about underlying inflation, betraying their earlier assurances that any burst of higher inflation would prove temporary.

Alternatively, if they do not take the first steps in the months immediately ahead, they risk being seen as having waited too long. While April’s spike in consumer price index inflation had the hallmarks of temporary effects as the economy reopens, investors will be more concerned if readings fail to moderate in July and August.

Treasury Market Narrative: Tapering Signal in Summer

To some degree, the market for U.S. Treasuries—both nominal (not inflation-adjusted) and Treasury inflation protected securities (TIPS)—appears to anticipate a tapering signal from the Fed at either the July FOMC meeting or the central bank’s Jackson Hole conference in August. This market narrative incorporates the potential for strong economic data from May through July and the expectation that the process from taper talk to initial rate hike would cover at least 18 months.

In this scenario, where the next cycle of rate increases would begin in less than two years, we think that Treasury yields would move somewhat higher. We expect the largest yield increases in the five- to seven-year portion of the yield curve. With the yield on the 30-year Treasury bond likely anchored around 2.5%, this move would decrease the difference between 5- and 30-year yields—likely flattening that section of the yield curve—while shorter-end curves would probably steepen.

Yields in the TIPS market would likely follow nominal yields higher, although short-maturity TIPS yields could move somewhat more. Market expectations for inflation, known as breakevens and measured by the difference between yields on nominal Treasuries and similar-maturity TIPS, would probably remain range-bound.

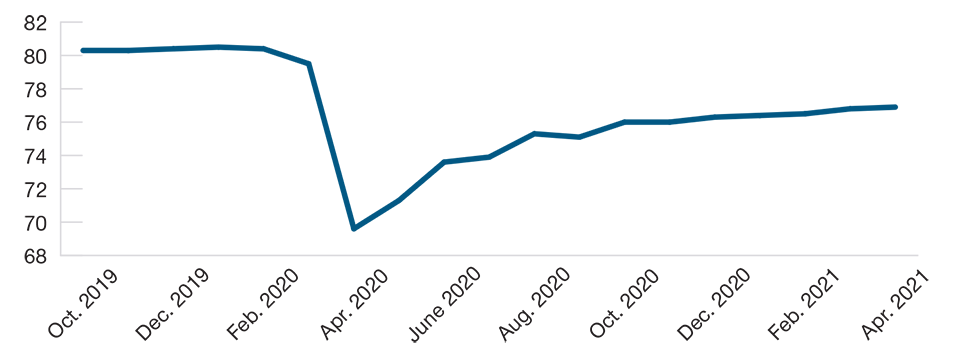

Progress Toward Full Employment Continues

(Fig. 2) Employment-population ratio, ages 25–54

As of April 30, 2021.

Source: U.S. Bureau of Labor Statistics, Haver Analytics

In this scenario, financial conditions1 would tighten marginally, and we would expect periods of market disruption and volatility as investors continue to work through the implications of the Fed’s gradual removal of accommodation. However, we anticipate that economic data will remain strong through the summer, helping to keep the disruption well managed and avoiding another taper tantrum.

Fed Could Wait to Talk Taper Even if Data Are Strong

However, even if economic data until July remain robust, the Fed could opt to not provide a definitive signal about tapering until the September FOMC meeting. The delay would strengthen the central bank’s commitment to let the economy boom until the labor market is more fully healed from the pandemic rather than removing accommodation to preemptively stave off inflation. In this scenario, we think that the 30-year Treasury yield would increase, breaking the 2.5% level and steepening the yield curve.

Shorter-term inflation expectations would probably rise, and the real (inflation-adjusted) yield curve would likely steepen strongly. Financial conditions would loosen in line with the Fed allowing the economy to run hot, further boosting growth.

Disappointing Data Could Cause Return to Post-GFC Patterns

If economic data are weaker than expected into the summer, Fed policymakers are likely to hold off on providing any sort of tapering statement or signal. This would probably cause the nominal Treasury yield curve to flatten as expectations for the strength of the economic recovery falter, the inflation risk premium erodes, and longer-term yields decrease. Real yields would likely decrease across the yield curve.

In this scenario, economic growth would begin to resemble the long recovery from the GFC rather than the widely expected rapid bounceback following the pandemic-related shutdowns of 2020 and early 2021. This would probably cause breakevens to return to their post-GFC pattern of trading in line with risk assets such as equities and corporate bonds, which has changed to some degree since the start of the pandemic.

Focus on Sustainability of Growth and Policy Reactions

The Fed and the fixed income markets will spend the next several months acclimating to the more fully reopened atmosphere as the headwinds from the pandemic hopefully continue to fade. There is still considerable uncertainty about the sustainability of growth, and the reactions of monetary and fiscal policy to variations in growth are untested. In this environment, we will focus on monitoring economic growth indicators as well as policy reaction functions. Our goal is to determine which Fed tapering scenario is most likely and to adjust the positioning of our portfolios to try to benefit from the likely market outcomes of that scenario.

What We're Watching Next

We will be tracking the political negotiations concerning the Biden administration’s American Jobs and American Families Plans and their proposals for stimulus spending and tax rate hikes. The talks, which we expect to continue well into the second half of 2021, could result in significant changes to the proposed legislation. The balance of stimulus and tax increases in the final bills is likely to impact the outlook for economic growth in 2022 and beyond.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

May 2021 / INVESTMENT INSIGHTS