June 2022 / GLOBAL ASSET ALLOCATION

Global Asset Allocation: June Insights

Discover the latest global market themes

1. Market Perspective

- While global growth is trending lower, recent economic data, especially pertaining to the labour market, have shown resilience amid geopolitical challenges, supply disruption and reduction of liquidity.

- The US Federal Reserve remains committed to its tightening policy, hinting at a front-loaded path of rate hikes. The European Central Bank (ECB) has telegraphed its plan to end asset purchases and begin raising rates despite a fragile macro backdrop, while the Bank of Japan (BOJ) remains steadfast on its policy of yield curve control.

- Emerging market (EM) central banks continue to tighten policy in response to heightened inflation and weak currencies, while China’s policies continue moving in the opposite direction to counter weakening growth caused by zero-COVID policy.

- Key risks to global markets include central bank missteps, lingering inflation, the commodity impact of the Russia-Ukraine conflict, the sharp slowdown in economic data and China balancing growth amid COVID-related lockdowns.

2. Portfolio Positioning

As of 31 May 2022

- While equity valuations are more reasonable after recent declines, we remain cautious on the earnings growth outlook and inflationary impacts on margins supporting our modest underweight. Within fixed income, we remain modestly overweight cash.

- Within fixed income, we added to emerging market dollar sovereigns as it has been an unloved asset class, and flows and positioning have been so negative that it is a buy signal.

- Within fixed income, we moderated our credit risk exposure by neutralising the overweights to global high yield and emerging market corporates as spreads may widen with slowing economic growth and tightening financial conditions.

- Despite attractive carry from elevated inflation levels, we trimmed our position in Euro inflation linked securities as we expect inflation to moderate from current highs.

- Taking advantage of higher yields, we added to Euro government bonds, providing mitigation against heightened global market risks.

3. Market Themes

So Far, So Good...

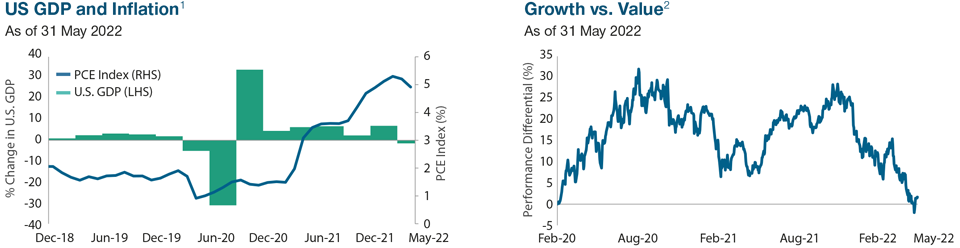

With inflation at multi-decade highs and growth already slowing, investors were rightfully sceptical about the Fed’s ability to aggressively tackle inflation without sending the economy into recession having waited too long. Now two hikes in and messaging front-loading future hikes with 50 basis point moves, recent data suggest that the broader economy is largely holding up. Although first‑quarter gross domestic product (GDP) showed that the economy surprisingly contracted by 1.5%, it appeared an anomaly due to temporary disruptions in trade and inventories, masking underlying support from consumer and capex spending. And while expected to slow, full year 2022 growth estimates still expect a 2.6% expansion, near pre-pandemic averages. Inflation too is showing some early signs of cooperating, with recent data suggesting easing in producer prices and wages, giving Fed officials a sigh of relief. While far from out of the woods, with topline CPI still expected to be near 6% levels at year-end, so far it seems like maybe, just maybe, a Fed-driven recession or stagflation are not inevitable.

Growth Spurt?

After more than a decade of outperformance versus value amid years of low economic growth, growth stocks went nearly parabolic during COVID lockdowns as many large-cap technology companies disproportionately benefitted from stay-at-home trends, sending valuations to record levels. That trend abruptly ended at the end of last year and has continued amid a spike higher in interest rates and threats of aggressive Fed tightening to battle multi-decade high inflation. The sharp drawdown in growth stocks has led to more reasonable valuations, and the move higher in rates appears to be largely priced in as expectations for economic growth are moderating—historically a time when growth stocks have tended to outperform. While time will tell if this is a pivotal inflection in style back toward growth stocks, they still face near-term challenges on upcoming earnings comparisons and uncertainty around the path of Fed policy. But for now, growth could be due for a spurt higher as many of the tailwinds for value—higher energy prices and rates—may be peaking.

Past performance is not a reliable indicator of future performance.

1 U.S. GDP is represented by the U.S. Gross Domestic Product Index quarter over quarter. The PCE Index is represented by the Personal Consumption Expenditure Core Price Index year over year.

2 Chart represents the difference between growth and value indices. Growth is represented by the Russell 1000 Growth Index and value is represented by the Russell 1000 Value Index. Sources: Bloomberg Finance L.P. and London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). See Additional Disclosures.

For a region-by-region overview, see the full report (PDF).

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.