December 2021 / INVESTMENT INSIGHTS

Germany’s Coalition Agreement Should Stimulate Growth and Inflation

The new government will likely show more flexibility on EU-wide issues.

Key Insights

- Germany’s new coalition agreement includes commitments to boost wages and, “ideally,” exit coal power generation by 2030.

- This will likely lead to strong growth and higher inflation, pushing up German bund yields.

- Reduced trade with China and a loosening of restrictions on EU spending are also in the cards.

Germany’s new “traffic light” coalition has agreed on a socially liberal agenda that includes higher wages, protection for public pensions, and a faster transition to renewable energy. Despite a commitment to reinstating Germany’s debt brake, the new program is likely to lead to stronger growth and higher inflation, pushing up bund yields. New appointments in key positions may also lead to reduced trade with China and greater spending flexibility for the European Union (EU).

The three coalition partners—the Social Democratic Party (SPD), Green Party, and Free Democratic Party (FDP)—fought their election campaigns on very different platforms. The SPD focused on issues of social justice, such as a large rise in the minimum wage, a stronger social safety net, and more redistributive taxation. The Green Party focused on an acceleration of the timetable to transition to net zero, favored greater spending to achieve this, and pushed for more carbon taxation. By contrast, the FDP focused on sound fiscal policy, adherence to the German debt brake, no additional taxes, and opposition to common debt at the EU level.

Despite these differences, the three parties managed to negotiate a coalition agreement that will enable each to claim victory on the issue it cares most about.

All Parties Secure Key Policy Objectives

The SPD’s headline policy, a 25% rise in the minimum wage to EUR 12 per hour from the current EUR 9.60, will be implemented in 2022. Other important SPD policies to be implemented include a commitment to easing access to the social safety net and maintaining pensions at 48% of average salaries without raising contributions or the retirement age. The new coalition government will inject EUR 10 billion into public pensions as an investment component to achieve these goals.

The Green Party secured a commitment to “ideally” exit from coal power generation by 2030 via a CO2 emissions tax of EUR 60 per ton, carbon neutrality by 2045, and a faster transition to renewable energy. The party also secured Germany’s commitment to implement a CO2 border adjustment mechanism at the EU level, as well as ongoing fiscal support to meet the unprecedented climate challenge.

The FDP secured adherence to the debt brake. While the coalition partners agreed that infrastructure investment by public German companies and a new Green investment fund will be excluded, the debt brake will restart in 2023. However, while the maximum possible structural deficit under the debt brake is 0.35%, the three parties agreed to a review of potential growth in Germany, which will likely allow the new government to run slightly higher deficits than under current rules.

At the EU level, all three parties agreed that the New Generation EU Fund should be temporary. Overall, all three parties can claim to have achieved important policy goals.

Agreement Commits to Higher Wages and Faster Carbon Reduction

The rise in the minimum wage to EUR 12 per hour will affect approximately 20% of workers in Germany, leading to an aggregate wage bill rise of around 0.8%. If most of this is spent (lower income workers have a high marginal propensity to consume), additional growth could reach from 0.5% to 1% in Germany in 2022.

Easier access to the social benefit system and promises to keep the retirement age the same could reduce labor supply, putting further upward pressure on wages, especially in light of demographic changes that suggest that the German labor force will shrink by 12% by 2035. Overall, these changes will likely result in the unions demanding a higher wage settlement than usual in the wage negotiations that will begin in late 2022.

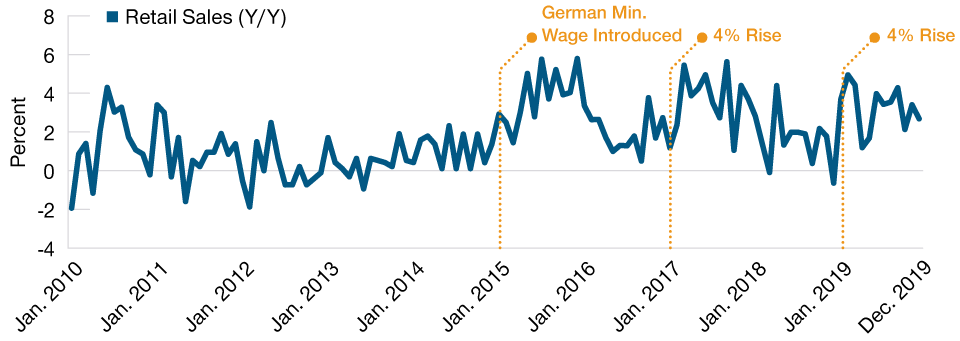

Rises in the German Minimum Wage Boost Retail Sales

(Fig. 1) Low‑income workers have a high propensity to consume

As of December 31, 2019.

Data shows retail sales following historical minimum wage rises in normal circumstances. The 2020 minimum wage rise is not shown as it occurred in unique circumstances during the pandemic.

Source: DESTATIS (German Federal Statistical Office), analysis by T. Rowe Price.

Germany will now aim to generate 80% of energy from renewables by 2030 (rather than the 65% previously planned). The planned phasing out of coal has been brought back to 2030 from 2038—a move that will require significant infrastructure investment in the coming years. Importantly, the German government has agreed to support the European Commission’s proposal on the EU‑level CO2 border adjustment mechanism. This policy will require importers to buy carbon certificates corresponding to the carbon price that would have been paid if the product was made under the EU’s carbon pricing rules. These costs would likely be passed on to consumers and, hence, make products from countries that rely on carbon‑intensive production, such as China, much less competitive in the EU.

The coalition treaty’s emphasis on reducing dependence on China, together with the appointment of Green co‑leader and China hawk, Annalena Baerbock, as foreign minister, suggests less trade with China in the future. The economic impact of this will be felt beyond trade, however. A key reason why inflation was low across developed markets over the past decade was the wide availability of cheap imports production via the proposed CO2 border adjustment mechanism. It is likely that the disinflationary influence of trade with China will be significantly reduced.

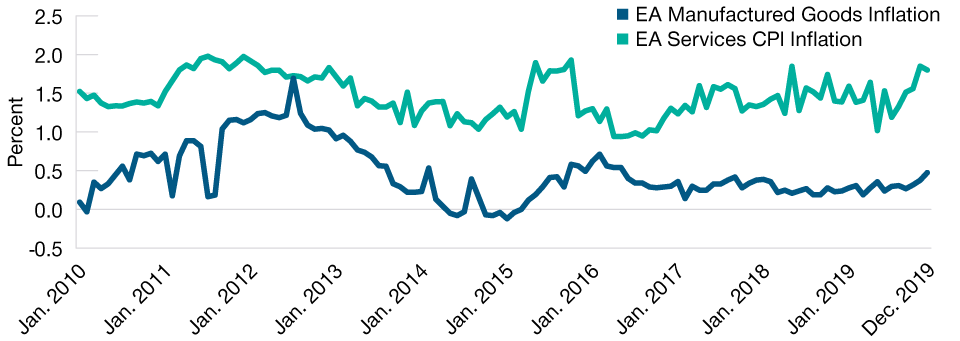

Chinese Imports Have Dampened Eurozone Inflation

(Fig. 2) Cheap products have kept manufactured goods inflation low

As of December 31, 2019.

The data shows inflation levels prior to the coronavirus pandemic. We have not included data from 2020 onwards as it was heavily distorted by supply chain problems.

Source: EuroStat.

Additional Green Funds to Be Balanced by Fiscal Discipline

The new goals to accelerate Germany’s transition to net zero will require significant additional investment. While the coalition treaty is light on numbers in this respect, reports suggest that the coalition will inject EUR 50 billion into a special climate fund with a supplementary budget for 2021. This money will be spent over four years until the next election.

Existing diesel subsidies will end and be converted to an additional EUR 8 billion to EUR 9 billion of Green investments. These two sources alone should lead to roughly EUR 21 billion worth of investments per year, or 0.7% of German gross domestic product. Furthermore, German public investment banks and companies will be allowed to invest greater resources in net zero and digital infrastructure projects. Although this is at the lower range of the 0.75%–1.25% we projected previously, it is still a sizable estimated rise in public spending by German standards.

The FDP scored a number of important wins on fiscal policy, thereby achieving its main objective. In addition to committing to restarting the debt brake in 2023, the coalition treaty explicitly refers to the EU Recovery Fund as a temporary facility, meaning that the government is unlikely to support a permanent fiscal redistribution facility.

However, the FDP had to make a number of compromises to secure these wins. The repayment schedule for borrowing beyond the debt brake during the pandemic stretched from 20 years to 35 years, which will provide additional fiscal space in the future. Furthermore, the coalition treaty agreed to revise the potential growth assumptions behind the debt brake, which will also provide an additional degree of fiscal space going forward—not only in Germany, but also within the Stability and Growth Pact at the European level. Furthermore, in a large step forward, the German government also agreed to complete the banking union and start negotiating a European Deposit Insurance Scheme. Although this is conditional on bank balance risk reduction, this nevertheless marks a significant departure from the previous German government’s stance on European financial integration.

New Bundesbank Boss Likely More Supportive of Flexibility in ECB Quantitative Easing (QE) Policies

Bundesbank president Jens Weidman resigned in October and will vacate the role in January, with media suggesting the SPD has negotiated the right to appoint his successor to this key position in German and European economic policy. Given the high probability that the next president of the Bundesbank will also become the next president of the European Central Bank (ECB), the SPD will likely appoint a Europhile candidate who is much closer to the center of the ECB’s governing council’s policy aims than previous Bundesbank presidents, who were historically very hawkish. This has important implications for current and future ECB policy, especially for the reinvestment of the ECB’s very large pandemic emergency purchase program (PEPP) facility.

Normally, the Banca d’Italia reinvests expiring Italian government bonds (BTPs) and the Bundesbank reinvests expiring bunds—and there was little chance of this arrangement changing under Weidmann. However, the next Bundesbank president is likely to be more Europe‑friendly and less opposed to creative monetary policy solutions to use PEPP reinvestment flexibly. The simplest solution would be for the Banca d’Italia to reinvest expiring bunds into BTPs when spreads start to widen; a more controversial (and politically difficult) strategy would be for the Bundesbank to buy BTPs directly. Regardless of the solution, there is good reason to believe that a new Bundesbank president will help make PEPP reinvestment a more powerful tool to address financial fragmentation.

Recent media reports suggest that, as a result of uncertainty about the consequences of the omicron variant of COVID‑19 spreading in Europe, the ECB’s governing council may delay a decision on what will happen to ECB QE after the PEPP finishes in March. These decisions were originally planned to be taken at the December ECB meeting, President Weidman’s last meeting. The new, probably less hawkish, Bundesbank president could be willing to support relatively more dovish changes to ECB QE policies when the Governing Council meets again in February.

Bund Yields Likely to Rise, but Spreads to BTPs to Remain Contained

In terms of market implications, the higher minimum wage is likely to propel consumption in Germany next year. However, this will also contribute to inflation through several channels. In the current supply chain environment, a wage rise of this size will also contribute to rising prices as demand exceeds the supply capacity of the economy. Business labor costs will rise and, in some cases, pass through to consumer prices. Finally, unions have thus far remained conservative with respect to their wage demands. However, the 25% rise in the minimum wage, together with higher inflation, will likely prompt unions to demand higher wage settlements to restore purchasing parity for their members. Firms are more likely to agree to this in a period of scarce labor supply.

While German inflation will likely fall from the 6% reached in November, these factors will likely lead to persistent above‑target inflation in 2023 and beyond. This is a key condition to satisfy the ECB’s forward guidance for a rate hike. Our expectation is that financial markets will therefore start pricing ECB rate hikes in 2023, which the ECB will likely deliver. This will likely support higher bund yields in 2022.

As a result of the coronavirus crisis, all European economies have become more indebted, making them more vulnerable to a rapid rise in their cost of finance. Past increases in the ECB’s policy rate have over‑proportionately affected BTP yields relative to bund yields. A large rise in this spread is undesirable as financial fragmentation tends to weaken the transmission of ECB monetary policy to the real economy. However, the new Bundesbank president will likely be less hawkish and more amenable to applying some flexibility to ECB asset purchases, which is likely to keep the spread between bunds and Italian government bonds contained.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

December 2021 / INVESTMENT INSIGHTS

December 2021 / INVESTMENT INSIGHTS