March 2021 / INVESTMENT INSIGHTS

Preparing for Higher Inflation

With inflation expectations on the rise, we look at a few investment ideas that could benefit from a higher inflation environment

Key Insights

- Inflation has remained at low levels for several years, but it is expected to rise in 2021 because of an anticipated increase in consumer spending, dislocated supply chains and “money printing” by central banks.

- We believe investors should consider including investments in their portfolios that could potentially benefit from higher inflation. Inflation-sensitive assets include cyclical equities (value, small caps, emerging markets), inflation-linked government bonds and “real assets” (natural resources and real estate equities).

After remaining at low levels for several years, inflation expectations for the rest of 2021 have risen because of an anticipated release of pent‑up consumer demand; dislocated supply chains; and “money printing” by central banks in support of swelling government debt. In our view, investors should consider adjusting their portfolios to prepare for this potential shift.

The coronavirus pandemic created dramatic changes in consumer behaviour, and it meaningfully curtailed spending. According to Bloomberg, consumers in the world’s largest economies amassed USD 2.9 trillion in extra savings during Covid-related lockdowns. At the same time, governments provided massive stimulus to replace lost wages. Most notably, US President Biden has successfully passed a huge USD 1.9 trillion Pandemic Relief Bill in March 2021.

Following the 2008-09 global financial crisis (GFC), stimulus did not result in notably rising inflation for goods and services. After the GFC, monetary stimulus has supported the financial system, leading to inflation in prices of financial assets, not inflation in consumer prices, because most of the money has not reached consumers. However, this time is different because the stimulus from governments directly reaches consumers, sometimes in the form of cheques in the mail. Consequently, consumers are expected to exit the pandemic with a remarkable savings glut, likely leaving them plenty of resources to draw from once they are safely able to spend after the, hopefully successful, rollout of vaccines.

On the supply side, the pandemic has caused disruptions in services and bottlenecks in the production and transportation of goods. As the global economy begins to recover, so have the prices of commodities, agriculture and oil. The price of a barrel of Brent has again reached USD 70, up from lows of below USD 20 in April 2020. In addition, according to data published by the US Federal Reserve, about a fifth of all US dollars in circulation were printed in 2020. These are strong inflationary forces that, coupled with a sudden increase in spending, may lead to rising prices.

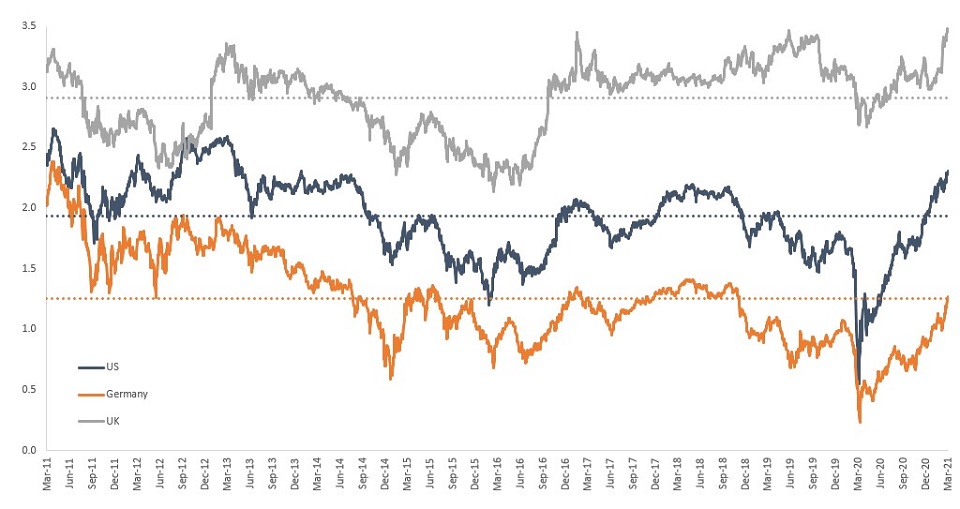

To gauge inflation expectations, investors can compare government bond yields with yields of inflation-linked government bonds with the same maturity – the breakeven inflation rate – shown in Figure 1. The breakeven rate indicates the fixed income market’s expectations for the annual rate of inflation over the next decade when using bonds with a 10-year maturity.

Figure 1: Inflation Expectations

The 10-year breakeven rate in the US, Germany and the UK – 10 years ended 16 March 2021

Past performance is not a reliable indicator of future performance.

Sources: T. Rowe Price analysis using data from Haver Analytics. Dashed line is the average rate over the time period.

While the anticipated inflation rates in all three countries remain relatively modest, it is noteworthy that expected inflation levels in Germany have not been this high since November 2018, in the US since June 2014 and in the UK in over a decade.

Many of the inflationary factors may be transitory, leading to a potential unsustainable spike in inflation. At the same time, some secular deflationary forces, such as ageing demographics, technological disruption and globalisation, are still in play, possibly anchoring inflation to lower levels than those seen in the past. However, in our view, investors should not continue to expect the abnormally low levels of inflation seen over the past decade.

Inflation rates are not expected to be the same across countries and regions. We expect higher inflation in the US than in Europe, for instance. The US economy is expected to rebound strongly, partially thanks to the massive stimulus programme of the Biden Administration and partially thanks to the unleashing of the mother of all pent-up consumer demands. The recovery in Europe is likely to be more modest. The European Central Bank has been struggling to reflate the Eurozone economy and reach its 2% inflation target in recent years. So, a moderate increase in inflation may be welcomed, as long as it does not exceed comfortable levels.

Investment Ideas

Given this expected shift, we believe investments that could directly or indirectly benefit from a higher inflation environment may add value to portfolios. These assets typically include value, small cap, and emerging markets equities. Within fixed income, inflation-linked government bonds and floating rate loans, where permitted for inclusion in portfolios, may be attractive options. “Real assets”— which include natural resources and real estate equities and REITs (real estate investment trusts) – also appear to be good alternatives as these assets have the potential to maintain or gain value during periods of higher inflation.

Key Risks

The following risks are materially relevant to the information highlighted in this material: Even if the asset allocation is exposed to different asset classes in order to diversify the risks, a part of these assets is exposed to specific key risks.

Capital risk - The value of your investment will vary and is not guaranteed. It will be affected by changes in the exchange rate between the base currency of the portfolio and the currency in which you subscribed, if different.

Equity risk—in general, equities involve higher risks than bonds or money market instruments.

Credit risk—a bond or money market security could lose value if the issuer’s financial health deteriorates.

Currency risk—changes in currency exchange rates could reduce investment gains or increase investment losses.

Emerging markets risk—emerging markets are less established than developed markets and therefore involve higher risks.

Foreign investing risk—investing in foreign countries other than the country of domicile can be riskier due to the adverse effects of currency exchange rates, differences in market structure and liquidity, as well as specific country, regional, and economic developments.

Interest rate risk—when interest rates rise, bond values generally fall. This risk is generally greater the longer the maturity of a bond investment and the higher its credit quality.

Investment portfolio risk - Investing in portfolios involves certain risks an investor would not face if investing in markets directly.

Real estate investments risk—real estate and related investments can be hurt by any factor that makes an area or individual property less valuable.

Small‑ and mid‑cap risk—stocks of small and mid‑size companies can be more volatile than stocks of larger companies.

Style risk—different investment styles typically go in and out of favor depending on market conditions and investor sentiment

Operational risk - Operational failures could lead to disruptions of portfolio operations or financial losses.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

March 2021 / INVESTMENT INSIGHTS