Will ESG Factors Lead a Flight Back to Active Investing in Japan?

Executive Summary

- Prevalent passive and ETF investment strategies in Japan, particularly among foreign investors, are looking increasingly limiting within a market undergoing significant change.

- Japanese companies are rapidly adopting ESG best practices and, for investors wanting to be selective on this basis, a passive approach is potentially constraining.

- We believe that successful investing demands an investment process that actively seeks to identify sustainable companies positioned on the right side of change.

With the maturing of the equity market cycle, a growing conflict has become apparent in terms of investor positioning in Japan. At the heart of this conflict is an increasing focus on environmental, social, and governance (ESG) factors, with many investors wanting to understand more about the companies they own and their respective ESG credentials. This is especially the case for foreign investors in Japan, where passive and exchange‑traded fund (ETF) vehicles dominate. In a market defined by dynamic change and disruption, gaining and acting on ESG insights is potentially being constrained by the prevalence of passive investment.

Passive Strategies Can Be Ill‑Equipped to Address the ESG Challenge

The Japan equity market’s fall from grace in the two decades that followed the excesses of the 1980s bubble is well documented. One clear trend that has followed over the past decade has been a large‑scale shift to passive investment strategies—coinciding with a sharp decline in active investment and supporting sell‑side research. This diminishing availability of local research has recently dovetailed with a period defined by significant secular change, both locally in Japan, and globally—change that is cutting across economic, financial market, political, and societal dimensions

While not isolated to Japan, investors are also increasingly demanding insights into any heightened ESG risks (and opportunities) of companies. Investors in passive strategies who want to understand more, or who want to influence positive change in company behavior or activity, can be constrained in their capacity to actively engage with their portfolio holdings.

With many large, passive Japanese equity strategies run by global investment managers that have limited or no local research presence, engagement with companies is imperfect at best, reactive or absent at worst. Meanwhile, the ability to be selective and single out progressive companies with strong or improving ESG standards is an opportunity being lost, given that a traditional passive approach does not discern between good and bad companies on traditional fundamental, or ESG, grounds.

We believe that successful investing demands an investment process that actively seeks to identify sustainable companies positioned on the right side of change.

We believe that successful investing demands an investment process that actively seeks to identify sustainable companies positioned on the right side of change.

Policy and Regulation Changes Heighten the ESG Imperative

We believe that successful investing demands an investment process that actively seeks to identify sustainable companies positioned on the right side of change. This is particularly relevant in Japan—a market that is experiencing considerable change, with an evolving corporate landscape and where companies are rapidly embracing ESG best practices, particularly under the influence of government initiatives and the demands of local pension funds.

One of the most significant achievements of Prime Minister Shinzo Abe’s “Abenomics” economic revitalization strategy has been an improvement in Japanese corporate governance standards. These have, in turn, increased the emphasis on delivering higher returns for shareholders. New stewardship codes, for example, have been implemented with speed and determination, with tangible changes in corporate atmosphere.

Change implies active management and investment selectivity, both to optimize returns and to manage the risks that emerge as companies find themselves on the wrong side of change and evolution. This is true today more than ever with respect to ESG considerations, which we believe can only be fully understood by active engagement backed by real, face‑to‑face interactions with company management teams.

In contrast, the fundamental business model of passive management inherently involves a low‑cost solution executed via investment in every company in a particular index. The outcome is the inclusion of companies that some will find objectionable and that invest in activities and practices that are at odds with certain core values. This lack of selectivity, in a world increasingly focused on ESG factors and judgments about long‑term sustainability (of business models and business practices), seems imperfect. This is especially the case in a market such as Japan, where corporate governance standards are evolving more rapidly than in any major developed market.

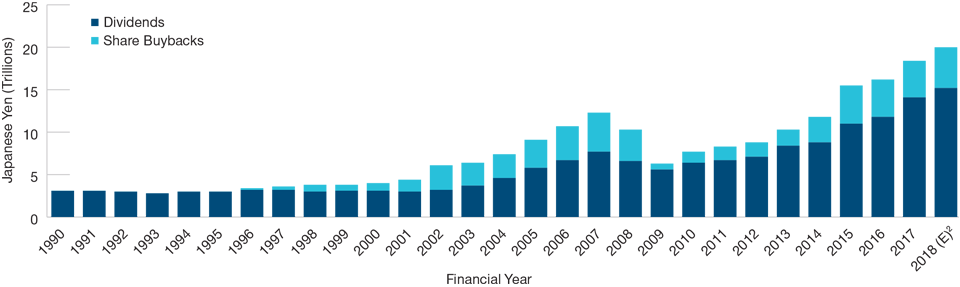

(Fig. 1) Improving Governance Means More Focus on Shareholder Returns

Total shareholder returns of all listed companies1

As of June 30, 2018

Past performance is not a reliable indicator of future performance.

Sources: Corporate Reports, Japan Exchange Group/ Haver Analytics, and Empirical Research Partners Analysis.

1 Listed on the Tokyo Stock Exchange (TSE); data exclude financials and utilities. Share buybacks net of share issuance. Based on governance reports submitted by mid-July each year.

2 E = estimated data, latest available at time of publishing.

Investors Increasingly Demand an ESG Lens

Over the past year, we have discussed increasingly specific and complex ESG integration and exclusion requirements with clients, particularly larger institutions. Dialogue often emphasizes concerns around corporate engagement or the application of negative ESG screens to portfolios (omitting companies based on particular attributes, such as weapons or tobacco exposure). Most frequently, it focuses on the requirement for ESG factors to be embedded within the investment decision‑making process, alongside the analysis of traditional financial data points.

This is important from an investment process perspective but also in terms of how it is shifting the investment opportunity in Japanese equities. To regard these concerns as transient would be an error, in our view, given the rapid adoption of ESG policies and the commitment of asset owners to influence corporates to the betterment of society.

ESG Best Practice Is a Journey, Especially in Japan

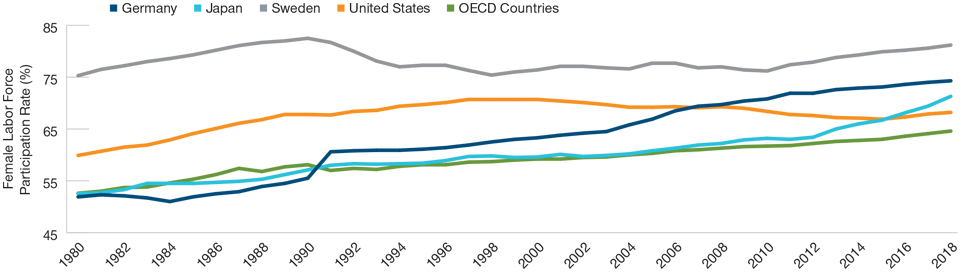

While improvements in corporate governance have served to lift shareholder returns in recent years, the next stage of Prime Minister Shinzo Abe’s reform agenda focuses on addressing workplace diversity. Here again, the commitment to change is real and progressive.

Workplace diversity, and the representation of women in senior management, in particular, are being given explicit focus and attention by a government that sees female workforce participation as a solution to Japan’s demographic shrinkage. These are topics that we will continue to engage with Japanese companies going forward in order to fully understand these dimensions of change—and their impact on performance—on a stock‑by‑stock basis.

(Fig. 2) Efforts to Boost the Number of Women in the Workforce Are Working

Japan’s female labor participation rate (%)

As of December 31, 2018

Source: OECD (2019). OECD Labour Market Statistics: Female Labour force participation rate data set:

https://data.oecd.org/emp/labour-force-participation-rate.htm, accessed on December 10, 2019. Analysis of data by T. Rowe Price.

Greater Insights From Dedicated ESG Resources and Investment Processes

Tremendous progress has been made in Japanese corporate governance in recent years. We believe this focus on improvement will only gather pace, creating both risks and opportunities for companies as they respond to, or fall behind, the pace of change. Active management approaches can be agile to identifying these potential winners and losers and managing them within the investment portfolio.

...our company engagement programs have always been driven by our fundamental research and supported by local market expertise.

At T. Rowe Price, our company engagement programs have always been driven by our fundamental research and supported by local market expertise. In recent years our research platform has been bolstered by substantial investment in our dedicated ESG research team, which provides proprietary analysis to integrate into our investment decision‑making. This provides us with a deeper understanding of potential ESG risks or opportunities in our investment universe and identifies opportunities for engagement with our portfolio holdings. Combined with the deep expertise of our nine‑strong Japanese equity research team, this positions us well to actively respond to the evolving investment needs of our clients.

What we’re watching next

An environment of modest global growth should continue to help corporate Japan perform well; however, we are mindful of the trade conflict between China and the U.S. Any escalation here is a key risk, for Japan and globally, and we continue to monitor developments closely. While the ideal scenario is that trade war concerns ease and sanctions are lifted, we believe that our quality bias can potentially hold us in good stead if the trade situation deteriorates and jeopardizes the supportive growth environment.

IMPORTANT INFORMATION

This material is being furnished for general informational purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, and prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

201912-1037408