Still Comfortable Being Uncomfortable

Equity markets continue to fascinate and surprise, with the one constant being a backdrop of uncertainty, driven by a cycle that keeps defying “the rules.”

Expectations of reflation and recovery, spurred on by U.S. tax cuts in 2018, quickly faded into a gloom of anticipated recession by mid‑2019, creating extreme investor positioning and especially in the valuations of defensives and cyclical stocks. Just as consensus fixed on trade and economic “crisis,” optimism was once again rekindled by a soothing policy response. The net outcome of this “cycle in a calendar year” is that global equity markets (measured by the MSCI All Country World Index in U.S. dollars) delivered +27.3%.1 Quite some rebound from the panic in December 2018.

Alongside healthy equity returns, the year will be remembered for the market rotation in the later months of 2019 and the impact it has had on portfolio outcomes. Starting in September, factors rolled over, cyclicals jumped, defensive havens proved no longer defensive, and standard deviation events were freely quoted. Despite the positive outcome and the comfort this might imply, it was an uncomfortable year, but also one filled with opportunity.

Improvement

In September, equity markets showed improvement, alongside very strong rotation. The catalyst centered on easing fears around trade and hopes of economic stability (bottoming purchasing managers’ indices (PMIs)), both of which applied pressure to defensive valuations.

Meanwhile, with the U.S.‑China trade war dance becoming more friendly and economic indicators beginning to show improvement for the first quarter of 2020, a different tone has come to the market of late, lifting market returns and economically sensitive stocks especially.

While market levels have clearly reflected a change in sentiment, we do see economic improvement in the coming year…

While market levels have clearly reflected a change in sentiment, we do see economic improvement in the coming year…

While market levels have clearly reflected a change in sentiment, we do see economic improvement in the coming year, as policy response exerts an influence and as we compare growth with the low base levels a year ago. These low base levels were established as Chinese and U.S. economic stimulus wore off, in tandem with an auto sales and information technology (IT) capex recession, all within a backdrop of rising tariffs and a “trade war.”

One key insight represented in our strategy in mid‑2019 was the need to reduce our positioning in sources of defensive “stability” and the search for ideas in the growth cyclical segment of the market. While our carefully contrarian approach was at odds with investor sentiment gravitating toward low controversy stocks, the search for high‑quality cyclical growth companies in a deeply unloved segment of the market proved to be a rich source of opportunity and return from September onward. While we remained underweight “value” and deep cyclicals, including banks and commodities, we have seen our key positions levered to capital markets, semiconductors, automation, and U.S. housing contribute to a positive outcome for our clients in 2019.

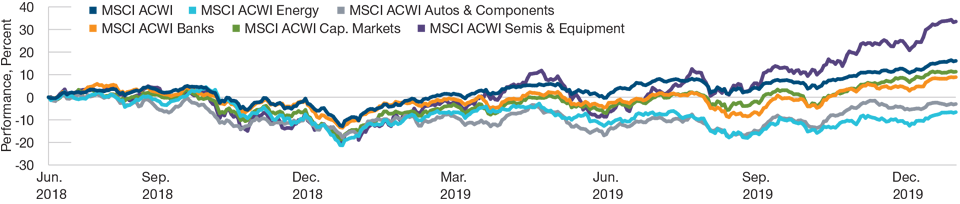

(Fig. 1) Cyclicals Reborn

The second half of the year saw economically sensitive stocks outperform.

As of December 31, 2019

Past performance is not a reliable indicator of future performance.

Sources: MSCI and FactSet (see Additional Disclosures).

+46%

MSCI Semiconductors & Semiconductor Equipment Index2

Importantly, while recent strength has backed stocks away from extremes, we remain excited by the prospects of select cyclical technology, automation, and industrial intelligence stocks. While isolating the secular winners on the right side of change is always our core thesis, integrated within our stock picks is the fundamental benefit from PMIs bottoming at a time when we also see an acceleration of semiconductor capex and inventory recovery, in what will be an important year for 5G mobile device innovation.

A Political Era

Demographics, automation, and excess energy have led us from a world of scarcity and supply constraints to a world of abundance. Technology is unlocking capacity in every industry, disrupting and deflating along the way. I thought that I would enjoy a world of abundance, but it turns out that it causes all sorts of problems.

One key issue relating to this flavor of abundance is that it is driven by intellectual property in the form of technology, making the winners concentrated and the losers broad. Median incomes are not rising fast enough, and democracies are rightfully upset at the median worker being left behind. This has led to a period of political protest, unease, and dissatisfaction that, today, feels global, rather than local. When future generations look back on this period, unpredictable political outcomes will define this era as much as technological progress and change, in part because they are so inherently linked.

We are especially conscious of the unpredictability of a U.S. election race that remains wide open, with dispersed candidate and presidential outcomes. Given the shifting rhetoric in an election cycle, we are sharpening our watchlist as we see secular and defensive growth names underperform.

As a brief observation on the ongoing trade negotiations, the Trump administration remains focused on obtaining significant concessions from China heading into the election, given the inability to pass policy through a divided Congress. The case for trade reform between the U.S. and China is strong, and the incentives for a surface‑level agreement, especially for Donald Trump, clearly outweigh the cost of a U.S. slowdown or recession.

…intellectual property in the form of technology [is] making the winners concentrated and the losers broad.

Secular Growth and Disruption Are Constant

In times of macroeconomic uncertainty, insights about stock‑specific and positive change are even more valuable. Here, we believe our research platform continues to provide exceptional support, spanning ideas to capture the pockets of improvement and bottoming of cyclical data points we expect in the coming year, as well the long‑term disruption that will define the next phase of the current technological revolution.

The case for industrial automation remains a compelling one, in our view. In the future, there will be many more robots, lasers, and computers (artificial intelligence and machine learning) running factory and machine‑driven processes. Companies with key intellectual property in these areas should become more valuable, and their addressable market is very large.

The case for analog and digital semiconductors is similar but nuanced. Analog involves taking real‑world measurements of temperature, light, and pressure and connecting those measurements to a computing platform. We will only see more of this over time, while what was once an industry defined by fierce competition has consolidated, helping the dominant survivors.

Digital semiconductors are the memory and logic of all devices and of the cloud. Dynamic random‑access memory (DRAM) was once isolated to PCs but has since spread to mobile computers (smartphones) we carry with us and rely on today. Now DRAM is spreading to become the “brain memory” for artificial intelligence and machine learning. We believe this will only grow.

We are also focused on the fundamental changes happening in semiconductor manufacturing. The semiconductor equipment sector has consolidated just at a point when physics has created an epic challenge for digital semiconductor makers trying to deliver innovation in chips. This is a powerful structural change benefiting those companies capable of advancing the industry further and should not be interpreted as merely a cyclical bounce on improved economic sentiment.

The Bull Isn’t Dying of Old Age

We know that we have enjoyed a very long equity bull market, but we remain cautiously optimistic. Despite the length of the cycle, interest rates and inflation remain low, in part because disruption is so prevalent–creating capacity and abundance. This era of disruption is deeply linked to the length of the equity cycle and how it has evolved, including the sources of return and the dispersion of opportunity and outcomes within the market.

It is also linked to today’s valuation backdrop, which remains reasonable. We believe this has been a distinctly begrudging bull market, which has real merits in terms of cycle longevity.

…this is a good environment for equity investors and especially for stock pickers willing to be uncomfortable.

While creating significant challenges ahead spanning society, economics, and politics, one outcome of an era of disruption is the world of moderation we find ourselves in as equity investors. Not moderation in the day‑to‑day news flow or the dispersion of returns stock by stock, but moderation of the growth and inflation environment that has persisted. This is an environment defined by the middle ground that exists between crisis and excess. Importantly, this is a good environment for equity investors and especially for stock pickers willing to be uncomfortable.

Fading exuberance and factor moves, while focusing on secular changes that define long‑term winners, have been the key to delivering alpha in this market. We will, therefore, remain focused on active insights and keep applying a carefully contrarian spirit in a market environment that we believe will continue to confound global investors.

1 Source: FactSet (see Additional Disclosures). As of December 31, 2019.

2 As measured by the performance of the index from May 31, 2019, to December 31, 2019.

Additional Disclosures

Financial data and analytics provider FactSet. Copyright 2020 FactSet. All Rights Reserved.

MSCI and its affiliates and third party sources and providers (collectively, “MSCI”) makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI. Historical MSCI data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

IMPORTANT INFORMATION

This material is being furnished for general informational purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, and prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

201912‑1038067