A Broader Approach to Investment-Grade Corporates

Executive Summary

- We are applying a broader lens to develop portfolio positioning in our corporate bond strategies for diversification away from the U.S. credit cycle.

- We have established a meaningful allocation to corporate bonds from high‑quality international issuers, particularly in Asia.

- The strategies also have allocations to asset‑backed securities that are much less exposed to a downturn in U.S. credit than investment‑grade corporates.

With the U.S. credit cycle in its later stages and escalating U.S. trade conflicts dampening corporate sentiment and expenditure, we are applying a broader lens to develop portfolio positioning in our corporate bond strategies. We have established a meaningful allocation to corporate bonds from high‑quality international issuers, particularly in Asia, for diversification away from the U.S. credit cycle. For similar reasons, the strategies also are allocating to asset‑backed securities (ABS) that are much less exposed to a downturn in U.S. credit than investment‑grade corporates.

We favor shorter‑maturity bonds for the reason that this positioning limits exposure to credit risk if there is a meaningful downturn in the U.S. economy. While we do not currently expect a recession in the next 12 months, we believe that this posture is a prudent hedge against credit downside.

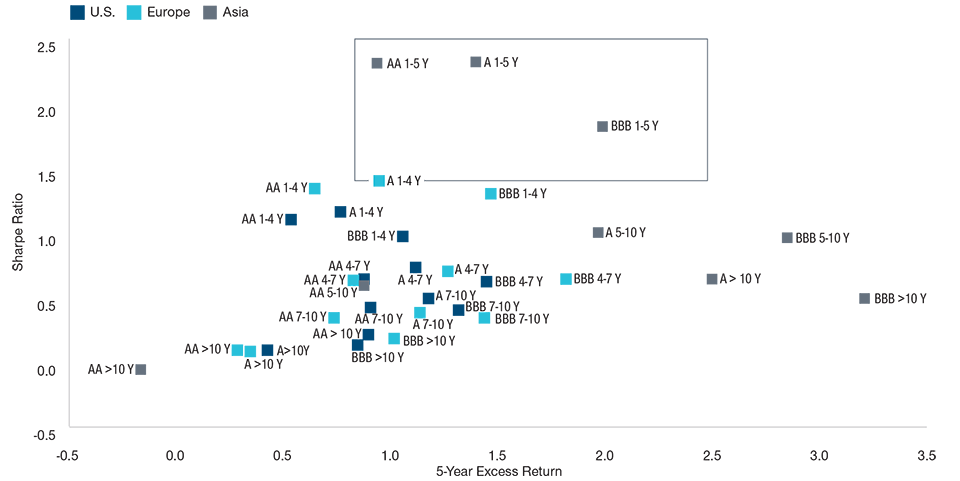

International Exposure Provides Diversification

Diversification away from U.S. issuers into global issuers is a key part of our positioning. We believe this international allocation can provide valuable exposure to credit cycles that are not as synchronized with the U.S. and may have further room to outperform. The number of non‑U.S. companies issuing investment‑grade debt in U.S. dollars has grown rapidly in the last few years, expanding the universe of corporates available for our analysts to source attractive relative value ideas.

We have a meaningful allocation to Asian investment‑grade corporates, which offer low correlation with the U.S. investment‑grade corporate market as well as a strong risk‑return profile. This exposure to Asian issuers is both defensive in terms of diversification as well as opportunistic as a potential source of higher risk/adjusted returns. Within the Asia region, we favor high‑quality issuers in the technology and telecommunications sectors. As with all other segments of the investment‑grade corporate bond market, we rely on the fundamental research of T. Rowe Price’s global network of credit analysts to select individual credits. We have analysts based in Asia who can conduct in‑depth, on‑site credit research.

(Fig. 1) Strong Risk/Return for Asian Corporates

Sharpe Ratio* Versus Excess Return** for Various Sectors

As of June 30, 2019

Past performance is not a reliable indicator of future performance.

Source: T. Rowe Price analysis of Bloomberg Barclays index data, Bloomberg Barclays U.S. Corporate Investment Grade Index and Global Corporate Investment Grade Index: Bloomberg Index Services Ltd. Copyright 2019, used with permission.

*Sharpe ratio measures a sector’s return above that of the risk‑free rate, divided by the standard deviation of excess return.

**Excess return is the return above that of a comparable‑maturity U.S. Treasury security.

ABS Add Stability and Incremental Yield

As another source of high‑quality diversification, we have an allocation to asset‑backed securities across our investment‑grade corporate portfolios. ABS are generally high‑quality and relatively stable—important defensive characteristics—while also providing some incremental yield over U.S. Treasuries. In addition, because consumer loans form the collateral for most ABS, they are less exposed to the U.S. credit cycle than investment‑grade corporate bonds.

One segment of the ABS market that we currently favor is whole‑business securitisations (WBS), which have characteristics of both ABS and corporate bonds. Like corporates, WBS do not amortise principal. The collateral backing WBS is generally a first‑priority interest in a company’s primary revenue‑generating assets—hence the “whole business” name. Quick‑service restaurant companies are typical WBS issuers, with the majority of the collateral backing the deals consisting of franchise fees and royalties. The cash flows from this collateral tends to be very stable, boosting the credit quality of the bonds. We have positions in the highest‑conviction WBS ideas from our securitised credit analysts. Exposure to BBB rated WBS can provide incremental yield over their similarly rated corporate counterparts.

Economic Acceleration Presents Upside Risk

We believe that the most meaningful risk to our broadly defensive positioning is an unexpected acceleration in the U.S. economy. While this scenario seems unlikely given the increasing trade war tensions and the fading effects of the 2018 tax cuts, an abrupt pickup in economic growth could extend the credit cycle and allow riskier, longer‑maturity corporates to outperform more conservative credits. We think that superior security selection from our global credit analysis team should help mitigate this risk.

WHAT WE’RE WATCHING NEXT

We are closely monitoring developments in the U.S.‑China trade conflict—and the Federal Reserve’s reaction to the economic pressure caused by the uncertainty surrounding the situation—to anticipate whether the U.S. economy will avoid a prolonged slowdown. The Fed cited the drag from the trade conflict as a factor in its decision to lower interest rates in July, its first cut since 2008.

Important Information

This material is being furnished for general informational purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, and prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

201908‑938489