February 2024 / INVESTMENT INSIGHTS

Corporate bonds—A compelling long-term income profile

Fundamental research is imperative in credit markets as headwinds rise

Key Insights

- Yields available in credit markets are both attractive and competitive with other asset classes, such as equity, in our view.

- The weak macro backdrop and higher cost of financing are headwinds for companies, however, and should be carefully monitored.

- Against this backdrop, security selection powered by bottom‑up research is imperative and can help to instill confidence about investing in credit markets this year.

What is appealing about credit markets for investors in 2024? Put simply, it’s their attractive and consistent income stream profile. But, with headwinds from a slowing economy and a higher cost of financing, some investors may be feeling apprehensive about credit investing this year.

In this first piece of our series on credit markets, we’re delving into these issues and how an approach that prioritizes research may help to ease investor concerns and instill confidence about investing in credit markets this year.

A compelling income profile

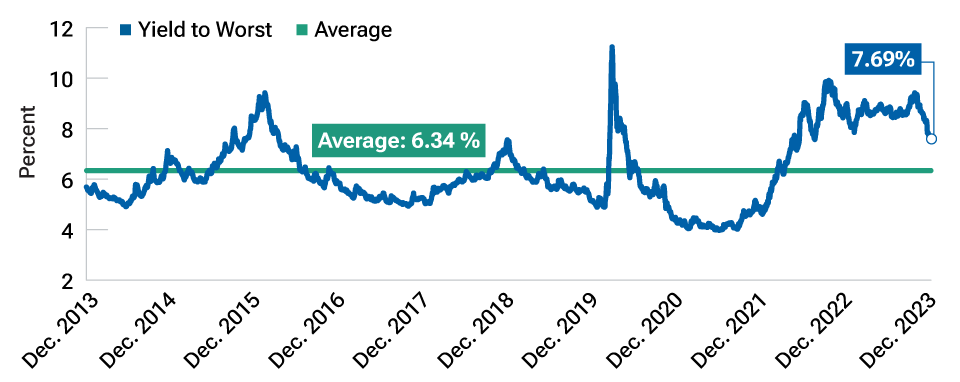

The corporate credit market continues to offer investors a compelling income‑generating opportunity, particularly for those investing with a long‑term horizon. Indeed, the average yield on offer in European investment grade is 3.56%—which is well above the average level of 1.41% observed in the last decade.1 Global high yield is also very appealing with average yields of 7.69% at present,2 again, much higher than the average yield of 6.34% observed in the last 10 years. These levels are not just attractive, but also competitive, in our view, especially given that fixed income is typically less volatile and a higher‑quality asset class than equity because it sits higher in the capital structure.

Burned in the past

Despite these encouraging characteristics, some investors remain cautious about credit investing. For some, the pain of losses suffered from credit in 2022 due to rising interest rates is still fresh. But there are indicators that suggest 2024 may be different. Inflation is clearly trending down, and most central banks appear finished with rate hiking and now look set to move into easing cycles at some point this year. This should help stabilize rate volatility, which is good news after the heightened periods of turbulence experienced in recent years.

Rising headwinds must be monitored

The picture isn’t entirely positive, and there are risks that need to be carefully navigated. Another concern for investors, for example, is that rising headwinds could lead to a pickup in rating downgrades and defaults this year. Even if a recession or a hard economic landing are avoided in 2024, the macro environment is likely to be weak, which could put pressure on company profit margins. In addition, companies face a higher cost of financing. The aggressive tightening of recent years means that it costs more for companies to borrow, which could eat into their profit margins. Although this could come down if central banks deliver cuts this year, it’s unlikely that the near zero interest rate environment that was the norm for so long after the global financial crisis will return, so companies will need to adjust to a higher cost of debt going forward.

Today’s yields have rarely been observed over the last 10 years

(Fig. 1) Yield to worst of the global high yield market

As of December 31, 2023.

Past performance is not a reliable indicator of future performance.

Source: ICE BofA. The yield of the Global High Yield Market is represented by the ICE BofA Global High Yield Index. (See Additional Disclosures.)

Importance of research

While income opportunities are clearly available, the tricky macroeconomic and funding backdrop demands quality research. We acknowledge that the conditions are a little tougher for companies and that there is potential for a deterioration in fundamentals in 2024. And while this could lead to rating downgrades and defaults picking up, there are ways to mitigate this—skilled security selection powered by bottom‑up research. By doing this, companies that are potentially more vulnerable to the headwinds of higher financing costs and a weak economy can be identified and avoided if needed. Similarly, research can help uncover those companies that are better equipped to navigate these conditions, and if the valuations and other factors, such as technicals, are right, these can become potential investments. We believe that an approach of rigorous research can help to restore investors’ confidence about credit investing this year and empower them to take potential advantage of the attractive yields that are available.

Additional Disclosures

CFA® and Chartered Financial Analyst® are registered trademarks owned by CFA Institute.

ICE Data Indices, LLC (“ICE DATA”), is used with permission. ICE DATA, ITS AFFILIATES AND THEIR RESPECTIVE THIRD‑PARTY SUPPLIERS DISCLAIM ANY AND ALL WARRANTIES AND REPRESENTATIONS, EXPRESS AND/OR IMPLIED, INCLUDING ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, INCLUDING THE INDICES, INDEX DATA AND ANY DATA INCLUDED IN, RELATED TO, OR DERIVED THEREFROM. NEITHER ICE DATA, ITS AFFILIATES NOR THEIR RESPECTIVE THIRD‑PARTY SUPPLIERS SHALL BE SUBJECT TO ANY DAMAGES OR LIABILITY WITH RESPECT TO THE ADEQUACY, ACCURACY, TIMELINESS OR COMPLETENESS OF THE INDICES OR THE INDEX DATA OR ANY COMPONENT THEREOF, AND THE INDICES AND INDEX DATA AND ALL COMPONENTS THEREOF ARE PROVIDED ON AN “AS IS” BASIS AND YOUR USE IS AT YOUR OWN RISK. ICE DATA, ITS AFFILIATES AND THEIR RESPECTIVE THIRD‑PARTY SUPPLIERS DO NOT SPONSOR, ENDORSE, OR RECOMMEND T. ROWE PRICE OR ANY OF ITS PRODUCTS OR SERVICES.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

February 2024 / GLOBAL EQUITIES

Saurabh Sud is a portfolio manager in the Global Fixed Income Division. He manages the Dynamic Credit Strategy, co-manages the US Core Bond Strategy, and is a member of the Global Fixed Income Investment team, with a specific expertise in credit markets. Saurabh is an executive vice president of the International Funds, Inc.; chairman of the Investment Advisory Committee for the Dynamic Credit Fund; and a vice president and Investment Advisory Committee member of the Global Multi-Sector Bond and Total Return Funds. He also is a member of the Sector Strategy Advisory Group. Saurabh is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price Associates, Inc.