International Economist,

T. Rowe Price

Choose your location

Austria

English

Austria

Belgium

Denmark

Estonia

Finland

France

Iceland

Ireland

Italy

Latvia

Lithuania

Luxembourg

Netherlands

Norway

Portugal

Spain

Sweden

Switzerland

United Kingdom

Japan Market Outlook

Economic momentum and growth supportive policies underpin Japan’s renaissance

Key Insights

- An encouraging growth outlook, nascent inflationary pressure, and ongoing market reform point to a positive outlook for Japan in 2024.

- Japan’s tightening labour market is leading to wage growth for the first time in decades. This is encouraging as a potential indicator that higher inflation can persist.

- Japan remains an outlier among developed market peers in terms of its accommodative policy stance. Any potential tightening of policy is a key risk to the 2024 outlook.

Just a year ago, few would have confidently predicted that Japan would see the kind of renaissance it is currently experiencing. An encouraging growth outlook and nascent inflationary pressure stand in stark contrast to the economic stagnation that has characterized much of the past 30 years. The resurgence has been encouraged by Japan’s outlier policy stance, maintaining an accommodative bias at a time when other major markets struggle with rising interest rates and fears of recession. At the same time, a weak currency is driving equity markets higher, while authorities continue to prioritize market reform, with the aim of making Japan a more competitive and attractive destination for foreign capital investment. This backdrop points to a broadly positive outlook for Japan in 2024, with a potential shift toward tighter policy being, perhaps, the main risk to this outlook.

"An encouraging growth outlook and nascent inflationary pressure stand in stark contrast to the economic stagnation that has characterized much of the past 30 years."

The signs point to a positive outlook in 2024

(Fig. 1)

Macro outlook—Japan’s direction of travel is positive

From an economic perspective, Japan has been a lot slower than other major economies in its recovery from the COVID shutdown. Real economic growth is robust, and the outlook is encouraging, with consensus expectations for growth to gain momentum in 2024, toward the high end of the last 10 years. Nominal GDP growth is expected to be on a rising trend, due to a rise in inflation, following decades of flat growth.

In contrast, growth in most other major economies in 2024 is expected to be around the low end of the range over the last decade. A key difference between Japan and other major markets is that Japan is not facing a backdrop of tightening in financial conditions, owing to its slower post‑pandemic recovery and weaker inflationary pressures. While other major economies continue to battle high inflation, forcing interest rates to multi‑decade highs, Japanese monetary policy has remained accommodative, with interest rates on hold.

In addition, fiscal policy is also supportive—the government recently announced stimulus in the form of tax cuts and rebates for households—providing a boost for Japanese consumers.

Inflation outlook—Data are encouraging, but durability is the key

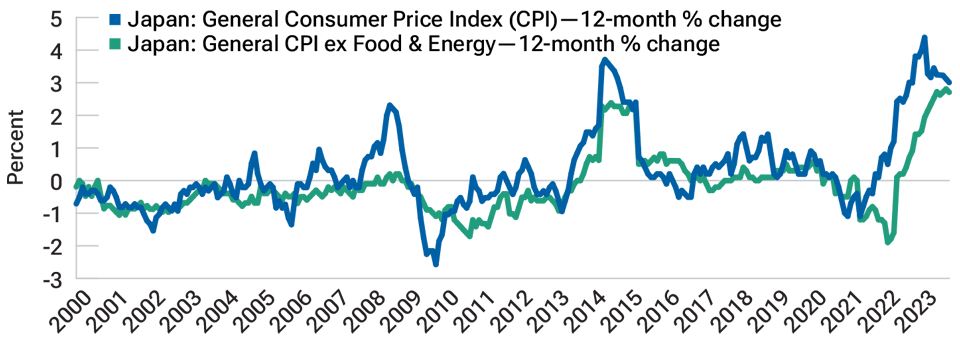

Having struggled for decades against a tide of weak inflation and long periods of deflation, the outlook here is also encouraging. Supply-side shocks, accommodative monetary policy, and tight labor market conditions have stimulated inflation. Unlike other major markets, Japanese policymakers are desperate to engineer sustainable 2% inflation supported by wage growth. The signs are positive, but after many false dawns, further evidence is needed to convince the Bank of Japan (BOJ) as to its durability. Core inflation (ex food and fuel) in Japan stands at 2.7%, year on year, as of September 2023, but there are strong base effects that impact the annual inflation data (Fig 2). Month-on-month data give a better picture of near-term inflation trends, and our measures of underlying, sequential core inflation indicate a run rate closer to 1.5%, which is below target.

Japan inflation is showing encouraging signs

(Fig. 2) It is too early to know if this is sustainable

As of September 2023.

Source: Japan Ministry of Internal Affairs and Communications. Analysis by T. Rowe Price.

Labor market outlook—A tightening labour market augurs well

One of the principal influences on Japan’s longer-term inflation outlook is the labor market. This has tightened in recent years, with unemployment levels currently around long-term lows. Certain sectors continue to report labor shortages, suggesting that the tight environment could continue well into 2024. In April 2023, annual wage negotiations saw workers receive a 3.6% overall wage increase, with a 2.1% increase in base pay—the highest since 1992. For the first time in decades, Japanese workers are looking forward to a higher wage outlook. The higher wage outlook, combined with a slowdown in inflation, will drive real income gains and underpin growth momentum.

The importance of wage inflation cannot be understated; it is the BOJ’s primary focus for policy decisions. Currently, questions are being asked about the potential for higher inflation to persist in Japan. The BOJ is less concerned about short-term supply shocks or distortions impacting core or headline inflation and more focused on wage growth as an indicator of longer-term inflation. The wage growth that we are now seeing in Japan suggests that company wage‑setting behavior is changing, which signals that higher inflation can persist, but it will remain below the 2% target.

"The importance of wage inflation cannot be understated; it is the BOJ’s primary focus for policy decisions."

Policy outlook—Can Japan maintain its accommodative stance?

There is no immediate urgency for the BOJ to change its accommodative stance, but our base‑case scenario is that it will terminate the current negative interest rate policy in April 2024 to coincide with the annual wage negotiations. This is also the time when the BOJ will include fiscal year 2026 in its forecasts, providing an additional year of forecasts, where the BOJ can signal rising confidence in higher inflation.

The other key decision facing the Bank of Japan is when—and how—to remove its yield curve control (YCC) policy. While this could happen as early as December this year, the YCC policy has already been gradually winding down, with the parameters of the 10-year yield cap being loosened toward the point of becoming irrelevant, as evident when the BOJ recently loosened the yield cap from a strict 1% limit to a more flexible “reference” rate.

Currency outlook—How low can the yen go?

The steep decline in the value of the yen, relative to the US dollar, has been a central narrative in Japan for more than a year and a primary influence on Japan’s strong equity market returns. Currently around multi-decade lows, the weak currency has been particularly supportive of Japan’s export‑heavy TOPIX index, with large, multinational auto companies and manufacturers benefiting greatly from their increased competitiveness. This has also meant that value-oriented companies have powered the market, significantly outperforming their growth-oriented counterparts. The swing toward value and away from growth in Japan in recent years has been significant. However, this differential looks increasingly stretched, compared with history, raising the potential for growth companies and more domestically focused businesses to rally in 2024 from depressed valuation levels. Should we see, at some point, a decline in global interest rates and a stronger yen, this would be a particularly supportive backdrop for growth companies.

Governance outlook—Prioritizing capital efficiency and higher shareholder returns

Japan investors should not overlook the ongoing corporate governance reform. These efforts are effecting meaningful change—change that will likely have a greater bearing on long-term equity returns than the country’s monetary policy.

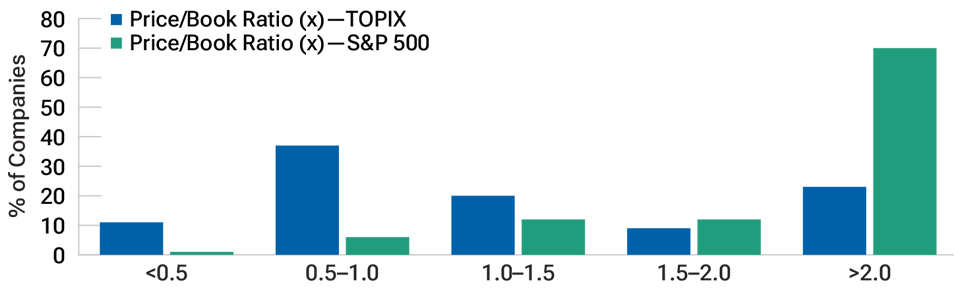

Recently, Japanese authorities have doubled down on reform measures, targeting the deep‑seated issue of capital inefficiency among Japanese companies. In early 2023, the Tokyo Stock Exchange (TSE) announced new rules requiring companies trading below a price/book ratio of 1x to improve or risk being excluded from the new Prime 150 Index. Perhaps more importantly, noncompliant companies will be required to explain why they remain so and to disclose action plans to increase their price/book ratio to 1x. While the TSE’s ambition is to weed out the worst‑run Japanese companies, the broader aim is to see sustainable improvement in returns on equity across corporate Japan. To date, just over half of the companies listed on the TOPIX have responded to this pressure, so the potential for further value creation, as more companies meet the threshold, is substantial (Fig 3).

Corporate governance reform is a priority

(Fig. 3) Authorities are focusing on increased value creation

As of September 30, 2023.

Source: Financial data and analytics provider FactSet. Copyright 2023 FactSet. All Rights Reserved.

"Japan investors should not overlook the ongoing corporate governance reform. These efforts are effecting meaningful change...."

Closing the gap with major market peers

In summary, the outlook for Japan is encouraging going into 2024, with expectations of robust economic growth and improving inflation that shows signs of being sustainable. The health of the global economy remains an important factor in this positive view, while accommodative policy and a weak currency are also key supports. Any potential moves to tighten policy via a hike in interest rates represent a key risk to the outlook. Given the BOJ will not want to risk undoing all the good work achieved to date, we believe it will remain dovish in its communication and keep policy accommodative.

On the market front, there is still a lot of hidden value to be revealed, particularly as reform measures gain traction, complicated cross-ownership structures are unwound, and companies are forced to allocate capital more efficiently. Improving returns on equity should see corporate Japan become more competitive with global peers and attract an increasing allocation of foreign capital investment.

Aadish Kumar

Thinking

Global Market Outlook insights

European Outlook

Europe must tread a fine line to avoid stagnation

China Outlook

Time to revisit an unloved asset class

Asia ex-Japan Outlook

Where we see opportunities in Asia ex-Japan equities

Sign up to receive our monthly Global Asset Allocation Viewpoints from our Investment Committee

Each month, our Investment Committee prepare a report revealing the two market themes they are watching, their bull and bear views per region and their latest asset class over and underweights.It has been designed to aid you in your decision making and client conversations.

Want to know more? Get in touch.

If you have questions or would like more information about T. Rowe Price please contact us.