May 2023 / MARKETS & ECONOMY

US Labor Market Strength May Be Tenuous

Emerging signs of weakness could be headwinds for jobs

Key insights

- The U.S. labor market faces headwinds amid tighter credit conditions for small businesses and declining corporate profit margins.

- We are closely monitoring forward-looking employment indicators, as historical data show that a persistent uptick in unemployment can be difficult to reverse.

The current strength in the U.S. labor market could deteriorate over the next 12 months. Tighter bank lending standards typically hurt small businesses—which account for a very large share of the U.S. employment market—and falling profit margins usually mean bad news for jobs.

In the first half of 2022, strong employment data helped to fend off a U.S. recession despite negative gross domestic product growth in the first and second quarters. While the economy has further softened over the past year, the labor market remains at a historically strong level, with unemployment at a remarkably low rate of 3.5% as of March 2023. However, emerging signs of weakness could mean that job losses are on the horizon.

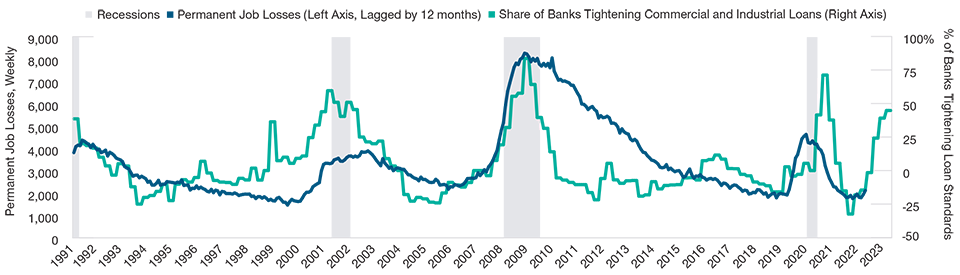

Following the recent banking woes, risk-conscious banks have been tightening lending standards to help preserve liquidity. Since small businesses often rely heavily on banks for their ongoing credit needs, tighter credit conditions could limit their operations, which would not augur well for the labor market (Figure 1). In fact, current survey data show that small businesses have moderated their hiring intentions.

Tight Credit Conditions Often Weaken Labor Market

(Fig. 1) Job losses versus tighter bank lending standards

January 1, 1991, through March 31, 2023.

Past results are not a reliable indicator of future results.

Source: Bloomberg Finance L.P.

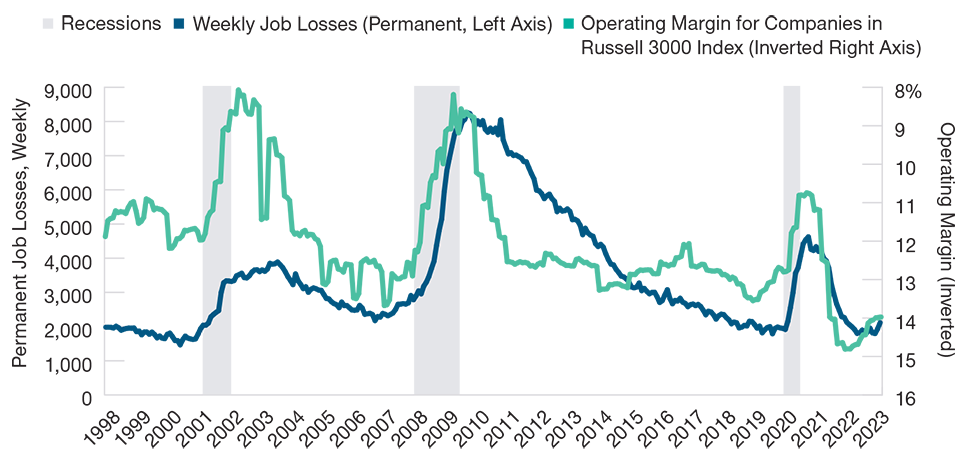

Falling corporate profit margins are another concern for the labor market. With dwindling savings, consumers have become less willing to pay the higher prices that corporations charged post-pandemic to help offset surging input costs. As corporate profits decline, employers may inevitably be forced to cut costs by laying off employees (Figure 2).

Falling Profit Margins Typically Lead to Job Losses

(Fig. 2) Profit margins versus weekly job losses

January 1, 1998, through March 31, 2023.

Past performance is not a reliable indicator of future performance.

Sources: U.S. Bureau of Labor Statistics and the Federal Reserve Bank of Atlanta/Haver Analytics.

Modest weakness in the labor market could help to push wage inflation back to sustainable levels, which would be positive for the economy. However, historical data show that once employment momentum turns negative, the trend is very difficult to reverse. Therefore, we are closely monitoring forward-looking employment indicators, and we remain cautious about the medium-term path for the U.S. economy.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

May 2023 / ASSET ALLOCATION VIEWPOINT