June 2022 / MARKET OUTLOOK

2022 Midyear Market Outlook: Transitioning to a New Paradigm

Adjusting to an uncertain future.

Heading into the second half of 2022, higher inflation and rising interest rates remain the most serious threats to global financial markets, T. Rowe Price senior investment leaders say.

Russia’s invasion of Ukraine has added fire to those risks by pushing food and energy prices sharply higher and further disrupting global supply chains.

This inflationary “shock on shock” has put more pressure on the U.S. Federal Reserve and other major central banks to tighten monetary policy, while making it more difficult for them to tame inflation without choking off economic growth, according to Sébastien Page, Head of Global Multi‑Asset and Chief Investment Officer (CIO).

“The three biggest challenges for investors over the next few months will be inflation, inflation, and inflation,” Page says. “It’s the transmission mechanism for all the other risks we are facing.”

The key question now is whether those risks will cause a sharp deceleration in growth or push major economies into full‑blown recessions, dragging corporate earnings down as well, Page warns.

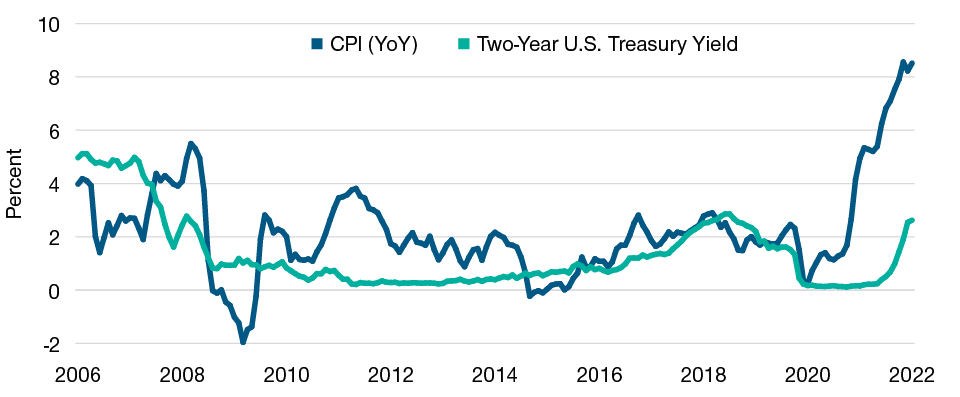

Beyond the cyclical risks, investors need to consider that global markets may have reached a structural inflection point—an end to the era of ample liquidity, low inflation, and low interest rates that followed the 2008–2009 global financial crisis (Figure 1).

The Era of Tame Inflation and Ample Liquidity Appears To Be Over

(Fig. 1) U.S. inflation* and the yield on the U.S. two‑year Treasury note

May 31, 2006, through May 31, 2022.

*Inflation = year‑over‑year change in U.S. Consumer Price Index for All Urban Consumers.

Sources: U.S. Bureau of Labor Statistics and the Federal Reserve Bank of St. Louis.

“I think that regime is over,” says Arif Husain, Head of International Fixed Income and CIO. “You can throw away that playbook.”

Central bank liquidity was critical for stabilizing economies and markets during both the financial crisis and the coronavirus pandemic, notes Justin Thomson, Head of International Equity and CIO. But it helped push valuations for many risk assets toward historical extremes. “I think we’ve learned from history that those extremes are never permanent,” he says.

However, the new paradigm also could offer potential opportunities for investors with the skills and research capabilities needed to seek them out, Thomson adds. “In volatile markets, active management can be your friend.”

Navigating Challenging Currents

Inflation expectations are likely to dominate financial market performance in the second half of the year, just as they did in the first, the T. Rowe Price CIOs predict.

Although investors must contend with other economic headwinds—the war in Ukraine, COVID‑19 lockdowns in China, and central bank tightening—inflation is the risk that channels those pressures into financial asset prices, Page argues.

- Higher energy and food prices in effect are a tax on the consumer, the main engine of global economic growth.

- With interest rates rising, continued earnings gains will be needed to support positive equity returns. But higher wage and input costs could cut into profit margins.

- Inflation raises the risk that the Fed will hike rates too aggressively, increasing the cost of capital and causing a recession.

“Those are three ways in which inflation can trigger a growth shock,” Page says.

The key questions investors face now are whether inflation has already peaked, and, if so, whether it will decelerate quickly enough to limit the need for a prolonged monetary tightening campaign by the Fed.

While there have been some anecdotal signs in some markets that price pressures are easing—such as a slowdown in home price appreciation and cooling demand for labor—clearer evidence is needed, Husain argues. “Until we see a meaningful decline in inflation toward the targets that central banks have set, the burden of proof hasn’t been met,” he says.

How Will Central Banks Respond?

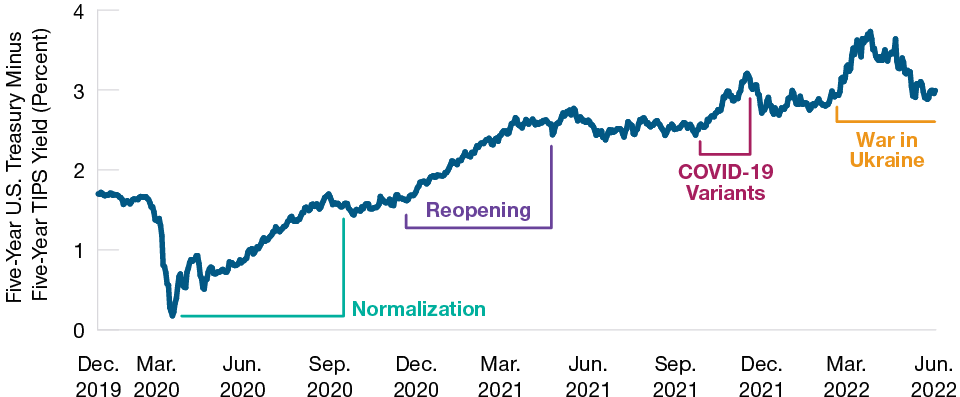

Even if inflation has peaked, fixed income investors appear unconvinced it will quickly return to the Fed’s long‑run target.

Figure 2 shows the spread, or breakeven, between yields on the nominal five‑year U.S. Treasury note and on the five‑year Treasury inflation protected security (TIPS). The breakeven is widely viewed as an estimate of investors’ inflation expectations.

Inflation Is Still the Key Issue for Global Investors

(Fig. 2) Five‑year U.S. inflation expectations based on TIPS breakeven yields

December 31, 2019, through June 1, 2022.

Source: Bloomberg Finance L.P. Data analysis by T. Rowe Price.

Although inflation expectations eased somewhat after surging in the wake of Russia’s invasion of Ukraine, the breakeven remained close to 3% as of the end of May—almost a percentage point higher than the Fed’s long‑term target for the U.S. consumer price index (CPI).

“The market has already priced in a number of future Fed rate hikes, yet it still expects inflation to overshoot the Fed’s target by a full percentage point per year over the next five years,” Page comments.

With the CPI up more than 8.5% year over year through May, the market consensus also could prove too optimistic, Page says. “What if the CPI gets stuck on the way down at 4% or 5%?” he asks. “How committed is the Fed to its 2% target?”

The answers could be critical, and not just for the bond markets, Thomson says. “For global equity markets, the inflation outcome is absolutely key.”

“If inflation settles around 3%, that could be a reasonable backdrop for equities,” Thomson argues. “If it’s between 3% and 4%, things could get a bit more difficult. But, if it’s over 4% it could be [Paul] Volcker time”—a reference to the Fed chairman of the early 1980s who hiked rates to double‑digit levels to break an inflationary spiral, pushing U.S. equities into a deep bear market.

The Supply Chain Factor

Inflation pressures are coming from both supply and demand and are being driven by both cyclical and structural factors, which makes the forecast exceptionally cloudy, Husain notes.

“I think what that means is that the Fed is going to keep raising rates,” Husain says. “There will come a point where they’ll want to pause and see what effect they are having. But my view is that we should be prepared for much higher rates going forward over the next few months.”

Page suggests a possible silver lining to those clouds. There is plenty of potential “pent up” supply in the global economy, he argues, which could help bring inflation down if supply chain bottlenecks can be unclogged.

“The question is whether fixing supply chains could do part of the Fed’s job for it,” Page says. “If it happens soon enough, maybe they won’t have to push demand off the cliff.”

For illustrative purposes only. This is not intended to be investment advice or a recommendation to take any particular investment action.

Fundamentals Matter

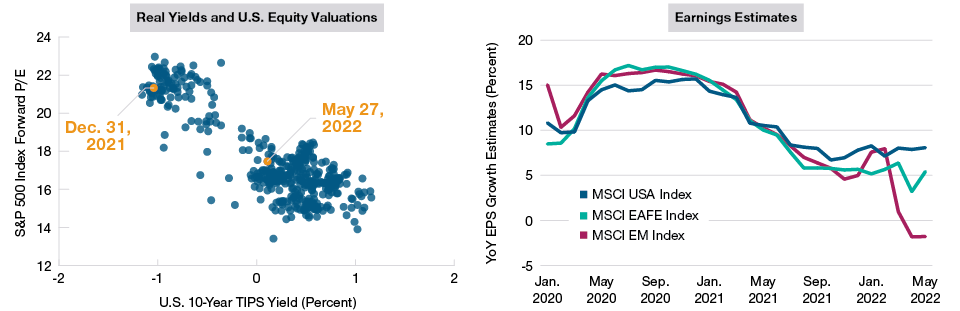

A brutal spike in bond yields largely drove global equity losses in the first half of the year. In the second half, stock market performance is likely to depend on the outlook for corporate earnings growth.

After spending most of 2021 in deep negative territory, Page notes, the real, or after‑inflation, 10‑year Treasury yield (as measured by the 10‑year TIPS yield) turned positive at the end of April. Figure 3 (left panel) shows the effect this had on U.S. equity valuations, which fell closer toward the middle of their recent historical range.

The Balance of Equity Risks Is Shifting From Interest Rates to Earnings Growth

(Fig. 3) S&P 500 Index forward P/E vs. 10‑year Treasury real yield and 2022 EPS growth estimates in USD

P/E versus real yields from January 3, 2014, through May 27, 2022. EPS estimates from January 31, 2020, through May 31, 2022.

Sources: Haver Analytics/U.S. Bureau of Economic Analysis, Federal Reserve Bank of Dallas, MSCI, and T. Rowe Price calculations using data from FactSetResearch Systems Inc. All rights reserved (see Additional Disclosures).

Now, Page says, with growth concerns rising, the focus is shifting to the “E” side of the price/earnings (P/E) ratio. “Everybody’s wondering if this will be the next shoe to drop.”

Although earnings momentum sagged in many non‑U.S. markets in the first half, earnings per share (EPS) growth in the U.S. remained surprisingly steady (Figure 3, right panel). But Page says he doesn’t believe this strength will last. “I think U.S. earnings are likely to decelerate in the second half, challenged by slowing economic growth,” he predicts.

Supply chain improvements also could impact earnings—but maybe not in a good way, Page says. While moving more products might boost sales and revenues, it also could limit pricing power and eat into profit margins.

Sector and Style Leadership

Poor earnings environments historically have tended to favor the growth style, which typically is less threatened by cyclical downturns. But, Thomson says, this time could be different, given the heavy weight the technology sector now carries in the growth universe.

“The pandemic really did pull forward digitization, so we’re going to be lapping some very strong 2021 earnings comparisons in the second half,” Thomson explains. “We’re also seeing some late‑cycle effects that are detrimental to tech, such as skill shortages and salary inflation.”

Consumer‑oriented technology platforms, such as streaming media, also could be exposed to a cyclical slowdown in spending, he adds.

These factors suggest that the back‑and‑forth style rotations seen since the pandemic recovery have tipped in favor of value. “A shift in market leadership appears to be underway,” Thomson says. “As we’ve seen from history, these cycles have tended to last a long time.”

China Could Offer Opportunities

With the Morgan Stanley Capital International (MSCI) China Index down almost 50% from its early 2021 peak as of the end of May, Chinese equity valuations appeared potentially attractive, Thomson suggests. However, Beijing’s “zero COVID” strategy has been a key obstacle to a growth revival.

“China has the capacity to stimulate,” Thomson observes. “But there’s no point in stimulating while locking down. It’s like stepping on the accelerator and the brake at the same time.”

How effectively Chinese policymakers will be able to boost growth in the second half is not yet clear, Thomson says. In addition to the coronavirus, sagging property values and credit defaults also could challenge any stimulus efforts.

That said, Thomson adds, in a world where many central banks are withdrawing liquidity to fight inflation, and governments in many developed countries are running deep fiscal deficits, China at least has scope to focus policy on supporting growth.

Another key factor for Chinese equities in the second half could be the regulatory climate, Thomson says, including Beijing’s treatment of the country’s domestic technology platform companies and its crackdown on foreign depositary receipt listings.

Thomson says he believes regulatory policies are likely to turn more market friendly in the runup to the Chinese Communist Party’s 20th Party Congress later in the year. “This regulatory cycle has been particularly drawn out and deep,” he says. “But we believe these issues will get better from here.”

Thomson says he’s reluctant to predict a leadership shift to non‑U.S. equities in the second half, given the U.S. market’s extended outperformance over the past decade. However, if the U.S. dollar appreciation seen in the first half subsides, and the technology sector continues to struggle, the relative performance of non‑U.S. equity markets should at least improve, he says.

For illustrative purposes only. This is not intended to be investment advice or a recommendation to take any particular investment action.

Flexible Fixed Income

U.S. Treasuries and other developed sovereign bonds did an exceptionally poor job of offsetting equity volatility in the first half. This suggests that investors may need to expand their search for diversification across fixed income sectors and geographic regions.

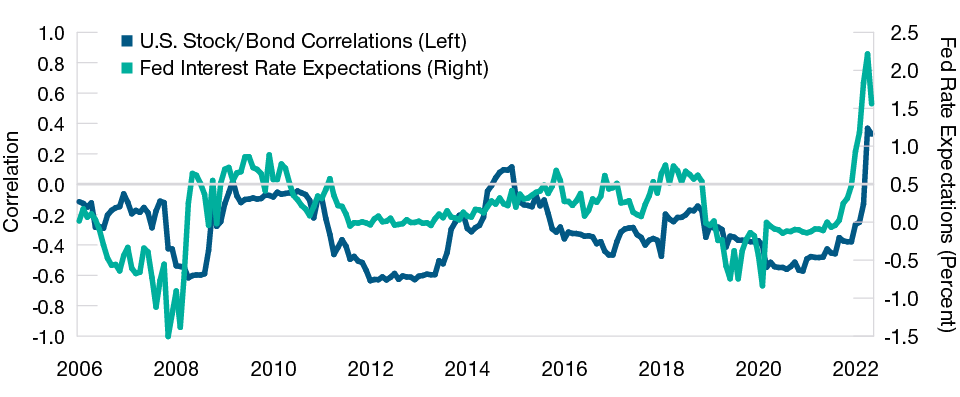

A key question, Page says, is whether the spike in stock/bond correlations seen in early 2022 was just temporary or reflected a structural “regime change” that could keep correlations high for an extended period. If the latter explanation is correct, alternatives to the traditional 60/40 stock/bond allocation that include dynamic hedging and other defensive strategies could offer advantages to some investors.

Stock/bond correlations have switched from positive to negative several times in recent years, Page notes (Figure 4). T. Rowe Price research suggests that these shifts typically were caused by economic shocks—sudden spikes in unemployment, inflation, or interest rates.

In a Rising Rate Environment, Bond Investors May Need More Diversification

(Fig. 4) Fed rate expectations vs. U.S. stock/bond correlations*

Past performance is not a reliable indicator of future performance.

January 2006 through May 2022.

*Fed interest rate expectations = yield on two‑year Treasury note minus federal funds target rate. U.S.stock/bond correlations = rolling two‑year correlation of monthly price changes for the S&P 500 Indexand the 10‑year U.S. Treasury futures contract.

Sources: Standard & Poor’s, J.P. Morgan North America Credit Research (see Additional Disclosures), and Bloomberg Finance L.P. Data analysis by T. Rowe Price.

“I think Treasuries still have a role to play in portfolio allocations—especially if the next leg of the crisis is a recession,” Page says. “But I also think investors are going to want to consider other approaches to downside risk mitigation.”

Is It Time to Extend Duration?

A more immediate issue for fixed income investors is whether bond yields have reached a near‑term peak, creating a potential opportunity to lock in portfolio income.

“In our view, this is the most attractive point to buy bonds that we’ve seen for several years,” Husain says. “We think that over the next several quarters investors may want to consider adding duration.”

However, Husain also predicts that the Fed will continue tightening until it has pushed its key market rate, the federal funds rate, into positive territory in after‑inflation terms. With the nominal fed funds rate still under 1% at the end of May, that would seem to leave considerable room for further rate hikes. As of early June, he adds, “I don’t think we’re quite at the peak for yields.”

For U.S.‑based investors worried about rising rates, global markets could offer diversification potential, Husain suggests. While the Fed is tightening, other countries are further along in their interest rate cycles. Some have stopped raising rates. Others have even started cutting them.

“By taking advantage of monetary policy divergence, investors can seek to diversify their interest rate exposures on a currency‑hedged basis,” Husain explains. Recent valuation levels potentially make emerging markets (EM) U.S. dollar bonds particularly attractive, he adds, although both country selection and underlying security selection will be critical.

The Upside Potential of Higher Yields

If yields do continue to rise, Husain says, at some point they should reach levels that offer attractive income opportunities for investors who understand how to manage duration—or who can rely on skilled investment professionals to do it for them. “Over the medium term, I think yields will reach levels that will make clients happy with the income they’re getting from their bond portfolios,” he says.

Some credit sectors, such as high yield corporate bonds, may have reached that point, Husain suggests. “Looking at the high yield universe, I’ve seen yields in the 7% to 8% range, in some cases,” he says. “I’ve seen some BB rated bonds priced at 80 cents on the dollar. Those are levels that historically have proven to be good buying points.”

The caveat to the bullish case for high yield is the uncertain economic outlook, Husain notes. As of May, high yield default rates remained near historical lows, and rating upgrades were more than twice as high as downgrades. But a growth shock could quickly change that picture.

“The threat of recession is real,” Husain cautions. “So investors need to do their homework.” For T. Rowe Price fixed income portfolio managers, he adds, this will mean relying on the firm’s extensive research capabilities and independent credit ratings to help navigate risks.

In volatile markets, duration management and yield curve positioning also could be important tools for managing risk, Husain suggests. “Fixed income is a relatively liquid asset class, so I would argue that investors could potentially benefit by using that liquidity to stay active,” he says.

For illustrative purposes only. This is not intended to be investment advice or a recommendation to take any particular investment action.

Managing Through Geopolitical Risks

Russia’s invasion of Ukraine has shaken the global political landscape. Beyond the destruction and human suffering inflicted by the war itself, the conflict threatens to worsen hunger in the world’s poorest countries, spur a new arms race, and block cooperation on problems like climate change and nuclear proliferation.

While those shocks could be felt for years, the consequences for global markets were more immediate:

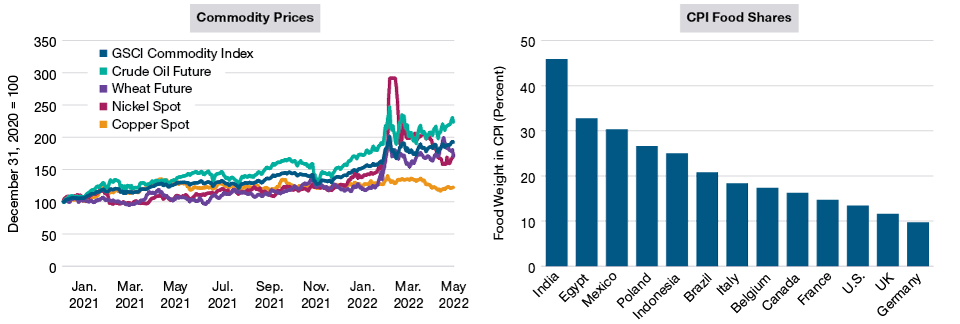

- Economic sanctions on Russia and the closure of Ukraine’s ports on the Black Sea sent prices of key commodities soaring (Figure 5, left panel).

- Fears about the impact on Europe’s economies pushed the euro and the British pound sharply lower against the U.S. dollar.

- Financial sanctions made Russian equities essentially uninvestable for foreign investors and pushed Russia’s foreign currency debt to the brink of default.

The War in Ukraine Is Feeding Commodity Inflation Worldwide

(Fig. 5) Price changes for select commodities and weight of food in national consumer price indexes

Past performance is not a reliable indicator of future performance.

Commodity prices from December 31, 2020, through May 31, 2022. Food price shares as of March 31, 2022.

Sources: Haver Analytics/J.P. Morgan (see Additional Disclosures) and T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved.

The war’s inflationary impact will be magnified in the developing world, where food products typically have a much heavier weight in consumer price indexes than in the developed world (Figure 5, right panel).

“Not only are Russia and Ukraine the breadbaskets of Europe,” Husain says, “but they export many of the chemicals that go into fertilizers and other agricultural inputs around the world.”

The war also has exposed Europe’s overdependence on Russia for oil and natural gas supplies, Thomson says. This will have implications not just for energy security, but for issues related to energy equity—such as consumer subsidies.

Disappointing financial performance in the oil and gas sector had led many equity investors to underweight energy stocks heading into this year, Thomson notes. But the Russian invasion was a wake‑up call.

“I think the market suddenly realized that energy is a strategically important sector and that we’ve probably been undervaluing it,” Thomson says. “A lot of portfolios are feeling the consequences.”

A Boost for Renewable Energy

Like most economic disruptions, the energy shock has the potential to create investment opportunities as well as risks. The transition to renewable energy sources, such as wind and solar, could be one of them, Thomson suggests.

“As the saying goes, the cure for high prices is high prices—in this case, high prices for hydrocarbons,” Thomson argues. “It reduces the relative costs of switching to other sources, so the transition to renewable energy should accelerate.”

Higher oil and gas prices also could spur investments throughout the energy supply chain, not just in renewable projects such as wind and solar farms, Thomson adds. This could include upgrading electrical grids and developing more efficient energy storage technologies—which in turn could boost demand for the raw materials used in those projects.

The Impact of Sanctions

The financial penalties imposed on Russia in response to the invasion could accelerate another longer‑term transition—toward a less centralized global financial system, Husain contends.

The initial round of sanctions included several unprecedented steps, such as freezing Russia’s foreign currency reserves at the Fed and other cooperating central banks and banning some Russian banks from the SWIFT (Society for Worldwide International Financial Telecommunications) financial messaging system.

While these measures have imposed heavy costs on Russia, they also could motivate other countries to seek alternatives to an international payments system dominated by the U.S. and the other major financial powers.

“Some countries may be looking at this and thinking, ‘We need to find another way of moving our money and transacting on a global basis,’” Husain says.

As long as sanctions remain limited to Russia and its closest allies, they appear to pose limited risks to the global economy. But that might not be the case if secondary sanctions were imposed on other countries, particularly China, in response to actions perceived as aiding the Kremlin’s war effort.

“The biggest unknown here for Chinese markets is geopolitical risk,” Thomson says. “If there is a further spillover from Russia’s invasion, and the Western democracies extend sanctions to China, then we would be in a very difficult situation.”

Although secondary sanctions on China appear to be a “tail” risk—i.e., a relatively low‑probability outcome—that risk is likely to weigh on Chinese equity valuations in the second half, Thomson adds.

For illustrative purposes only. This is not intended to be investment advice or a recommendation to take any particular investment action.

Summary

The shocks inflicted on markets in the first half of 2022 required global investors to adjust their expectations for inflation, interest rates, earnings growth, and volatility. But a longer‑term adjustment also may be necessary, the T. Rowe Price CIOs say.

“We are in the midst of a paradigm shift here,” Thomson says. “We’re moving from a low‑yield, low‑inflation, low‑volatility environment to one of higher inflation, higher rates, and probably higher volatility.”

New conditions may force many investors to unlearn some old ideas, like the notion that the Fed and/or the other major central banks can be counted on to pump liquidity into the markets if asset prices fall too far or too fast—a concept popularly known as the “Fed put.”

Now, “the Fed put is either gone or deeply out of the money,” Page says. If anything, he argues, investors face the potential for a “Fed call.” If risky assets rally too exuberantly in the second half, an inflation‑wary Fed might respond by hiking interest rates more aggressively, choking off any rebound.

Lessons From the Past

Previous paradigm shifts offer some unsettling examples of markets caught off guard either by valuation excesses or external shocks—or both, Thomson says.These past episodes include:

- The 2000–2002 dot‑com crash, which illustrated the enduring importance of basic valuation fundamentals like cash flow and earnings.

- The highly concentrated U.S. large‑cap market of the early 1970s, which was slammed by oil supply shocks and rampaging inflation.

But history doesn’t have to repeat, Thomson observes. “The way central banks are dealing with inflation is more sophisticated this time. I think that will lead to better outcomes than we saw for the duration of the 1970s.”

But the new paradigm also will require investors to pay close attention to their time horizons and tolerance for risk.

“Risk tolerance doesn’t usually get tested in normal times,” Page cautions. “You only truly understand your risk tolerance during regime shifts.”

Above all, we believe investors should understand the risks of remaining passive in a fast‑changing market environment. Capitalization‑weighted indexes may be poorly positioned for structural change, making skilled active management a critical tool for identifying risks and opportunities.

“In the middle of a paradigm shift, doing nothing can be a very dangerous thing,” Husain says.

2022 Midyear Tactical Views

*For pairwise decisions in style and market capitalization, boxes represent positioning in the first asset class relative to the second asset class.

The asset classes across the equity and fixed income markets shown are represented in our multi‑asset portfolios. Certain style and market capitalization asset classes are represented as pairwise decisions as part of our tactical asset allocation framework.

This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action.

Additional Disclosures

MSCI and its affiliates and third party sources and providers (collectively, “MSCI”) makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI. Historical MSCI data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Copyright © 2022, S&P Global Market Intelligence (and its affiliates, as applicable). Reproduction of any information, data or material, including ratings (“Content”) in any form is prohibited except with the prior written permission of the relevant party. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice. Credit ratings are statements of opinions and are not statements of fact.

Information has been obtained from sources believed to be reliable but J.P. Morgan does not warrant its completeness or accuracy. The index is used with permission. The Index may not be copied, used, or distributed without J.P. Morgan’s prior written approval. Copyright © 2022, J.P. Morgan Chase & Co. All rights reserved.

Important Information

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is no guarantee or a reliable indicator of future results.. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

USA—Issued in the USA by T. Rowe Price Associates, Inc., 100 East Pratt Street, Baltimore, MD, 21202, which is regulated by the U.S. Securities and Exchange Commission. For Institutional Investors only.

© 2024 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.

June 2022 / MULTI-ASSET SOLUTIONS