October 2021 / U.S. FIXED INCOME

The Fed Surreptitiously Turns Dovish

SEP reveals a renewed commitment to average inflation targeting.

Key Insights

- An examination of the September FOMC meeting’s summary of economic projections reveals that the Fed has surreptitiously made a dovish turn in monetary policy.

- The FOMC is showing renewed commitment to the average inflation targeting framework, which can result in higher yields and a steeper yield curve.

- Stubbornly high inflation must recede to allow this new framework to proceed, which will be the focus of markets over the coming months.

The September Federal Open Market Committee (FOMC) meeting left the lasting impression on most that the conditions for tapering quantitative easing (QE) have been “all but met”1 and a reduction in purchases “may soon be warranted.”2 One could assume that, by themselves, these phrases represent a further hawkish shift by the FOMC. Moving past the taper discussion, however, closes a hawkish chapter for the Federal Reserve (Fed). The next chapter was revealed in the summary of economic projections (SEP),3 and it is overwhelmingly dovish.

SEP Indicates Dovish Policy Stance for Years

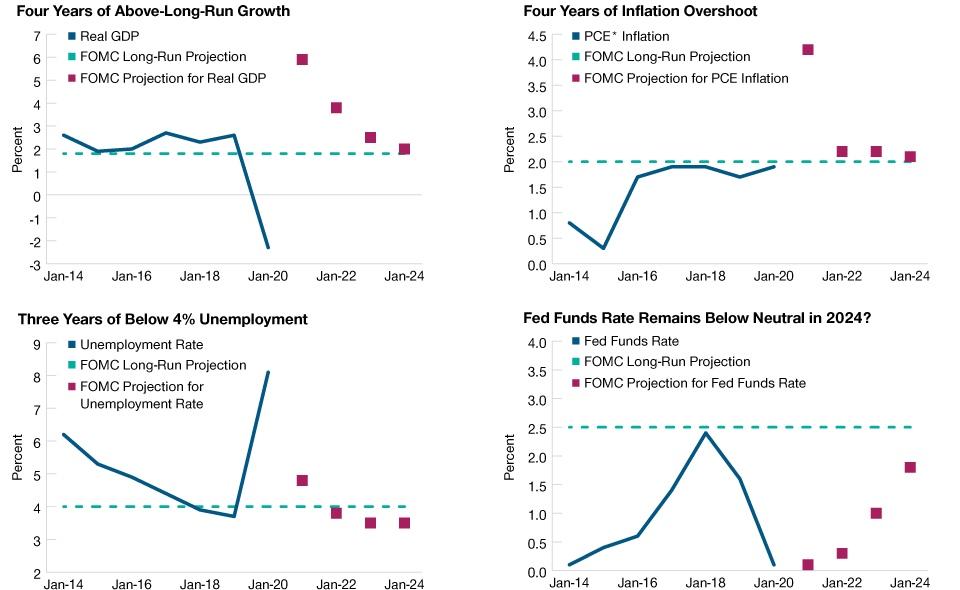

The SEP is much maligned, but it is a highly informative and valuable indicator of the FOMC reaction function. The September SEP indicated an extremely dovish reaction function. The median projections (see charts below) indicate four years of inflation overshoot and three years of below 4% unemployment, but the 2024 federal funds rate median (the 2024 “dot”) is only at 1.75%, 0.75% below the long‑run, or neutral, rate. That is incredibly dovish!

SEP Reveals Dovish Long‑Run Stance

As of September 22, 2021.

Source: Summary of Economic Projections. Data provided is for illustrative and informational purposes only. There can be no assurance that the estimates will be achieved or sustained. Actual results may vary.

*Personal consumption expenditure.

The medians or “dots” for 2023 and 2024 did move slightly higher, but in revealing the 2024 dot, the FOMC indicated it would be in a highly accommodative stance years after having achieved its objectives. Within any historical context, these projections make no sense—but perhaps this is the new, average inflation targeting framework4 in action. The SEP suggests the post‑taper period will likely be punctuated by a comeback of average inflation targeting and a re‑affirmation of the new framework. The FOMC has taken a first successful step in separating the tapering decision from the tightening decision.

Probabilities of Higher Yields, Steeper Curve Have Increased

What does this mean for U.S. Treasury yields? The taper negotiation, which began in May, was a major component of the summer decline in yields. The market had difficulty processing a net hawkish shift from the FOMC at a time when supply constraints were pushing inflation higher and growth lower. Getting on with the taper resolves the negotiation and has allowed yields to release from their summer range. Post‑taper, an FOMC showing renewed commitment to the average inflation targeting framework can result in a continuation of the current trend of higher yields and a steeper curve. Somewhat controversially, though, it will not likely be higher inflation but an easing of inflation that leads to higher yields.

Paradox of Lower Inflation Leading to Higher Yields

At this point in this particular cycle, lower inflation means higher yields, which is the opposite of the typical dynamic. This paradox is present purely because the source of inflation now is shortage‑induced, cost‑push price pressure. Stubbornly high inflation has taxed growth and led the FOMC into a protracted taper discussion, which raised questions about whether we were in a stagflationary5 environment.

There are many reasons to believe that inflation will remain above 2%, but for this potentially stagflationary environment to recede and allow the FOMC to pursue average inflation targeting, supply side inflation pressure must dissipate. From an expectations standpoint, this is already happening. Expectations for inflation were laughably low earlier this year and have now adjusted much higher. Inflation is not sneaking up on anyone anymore; it has space to ease lower.

The Next Phase of Monetary Policy

The September FOMC meeting presented a surreptitiously dovish outcome, indicating that the next phase of monetary policy is a renewed commitment to the still relatively new average inflation targeting framework. This framework supports strong future economic outcomes, which can lead a renewed push higher in yields. Stubbornly high inflation must recede to allow this new framework to breathe; while early indications suggest this process has begun, that will be the focus of markets over the coming months.

What We're Watching Next

We monitor surprises in economic statistics, measured in terms of how much an actual data point exceeds or falls short of consensus expectations. Economic data surprises were consistently negative over the summer, which helped define the top of the trading range for Treasury yields. Positive data surprises could help clear the way for another leg higher in yields.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

October 2021 / U.S. FIXED INCOME

October 2021 / ENVIRONMENTAL, SOCIAL, AND GOVERNANCE