December 2021 / GLOBAL MARKET OUTLOOK

Playbook for a Shifting Economic Landscape

After back‑to‑back years of strong performance across most equity and credit sectors, global markets face more uncertain prospects in 2022, according to T. Rowe Price investment leaders. Investors will need to use greater selectivity to identify potential opportunities, they say.

Higher inflation, a shift toward monetary tightening, and new coronavirus variants all pose potential challenges for economic growth and earnings—at a time when valuations appear elevated across many asset categories.

On the positive side, household wealth gains, pent‑up consumer demand, and a potential boom in capital expenditures could sustain growth even as monetary policy turns less supportive.

“Over the next year, I think the bottom line is that we will face slowing growth, but still very high growth,” predicts Sébastien Page, head of Global Multi‑Asset.

But strong growth and rising wages also could put further upward pressure on U.S. commodity and consumer prices, which accelerated sharply in the second half of 2021.

Mark Vaselkiv, CIO, Fixed Income, worries that the U.S. Federal Reserve may have fallen behind in the fight against inflation. As of mid‑November 2021, interest rate futures markets indicated the Fed wasn’t expected to begin raising rates until mid‑2022.

“The Fed may already be behind the curve,” Vaselkiv warns. “That could be the biggest risk for 2022.”

Economic growth should continue to support corporate earnings and credit quality in 2022. But the earnings momentum seen in 2021 is unlikely to be repeated, suggests Justin Thomson, head of International Equity and CIO. “It seems highly unlikely that positive [earnings] revisions will be of the same level of magnitude as we’ve been seeing.”

This could make the interest rate outlook an even more critical factor for equity performance. “If U.S. rate expectations get brought forward, I think equity markets will take their cue from that,” Thomson says.

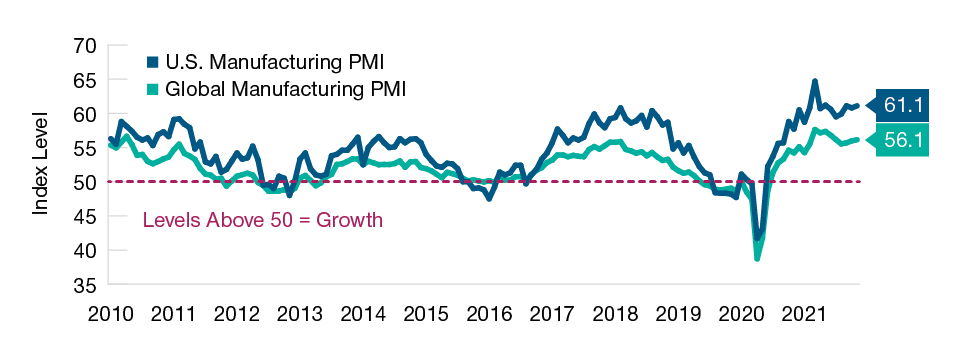

The Global Recovery Has Slowed but Still Appears on Track

(Fig. 1) U.S. and global Purchasing Managers’ Indexes (PMI) for manufacturing

As of November 30, 2021.

Sources: Institute for Supply Management and J.P. Morgan/IHS Markit/Haver Analytics (see Additional Disclosures).

Growth Delayed, Not Derailed

Despite headwinds from the pandemic, the global economic recovery still appeared on track as 2021 neared its end. But inflation risks have risen. In 2022, investors will need to watch what fiscal and monetary policymakers do to try to stem price pressures while sustaining growth.

Although a COVID‑19 resurgence in Europe and the emergence of the highly mutated omicron variant are reminders that the pandemic is still with us, the net economic effect of past waves—such as the spread of the delta variant—has been to postpone activity, not prevent it. This pattern could give a modest boost to growth in the first half of 2022, Page says.

The bearish economic case now centers on monetary and fiscal policy, Page contends. As governments and central banks withdraw the massive stimulus applied during the pandemic, economic growth inevitably will slow sharply—or so the argument goes.

But slower growth doesn’t necessarily mean low growth, Page responds. He points to a number of tailwinds that he thinks could sustain the recovery in 2022:

- Consumers are in a strong cash position, especially in the United States, where over USD 2 trillion is sitting in checking accounts and other short‑term deposits.

- Asset appreciation has boosted household wealth both in the U.S. and globally.

- Pent‑up demand for housing should continue to fuel new home construction.

- Corporate balance sheets generally are in strong shape, with high liquidity and low debt ratios.

- Transportation bottlenecks appeared to ease in late 2021, as seen by a sharp drop in global seaborne shipping costs.

The question, Vaselkiv says, is whether global consumers will convert their improved financial positions into higher spending. Assuming pandemic disruptions remain relatively manageable, he sees the potential for a surge in pent‑up demand in 2022 for travel, entertainment, and other “quality of life” services, as well as for new cars as auto production normalizes.

With interest rates still low and banks eager to put deposits to work, loan growth also could drive consumer demand, Vaselkiv adds.

But the same factors—free cash, wealth, pent‑up demand—potentially supporting growth also could prolong the sharp upswing in inflation seen in the second half of 2021.

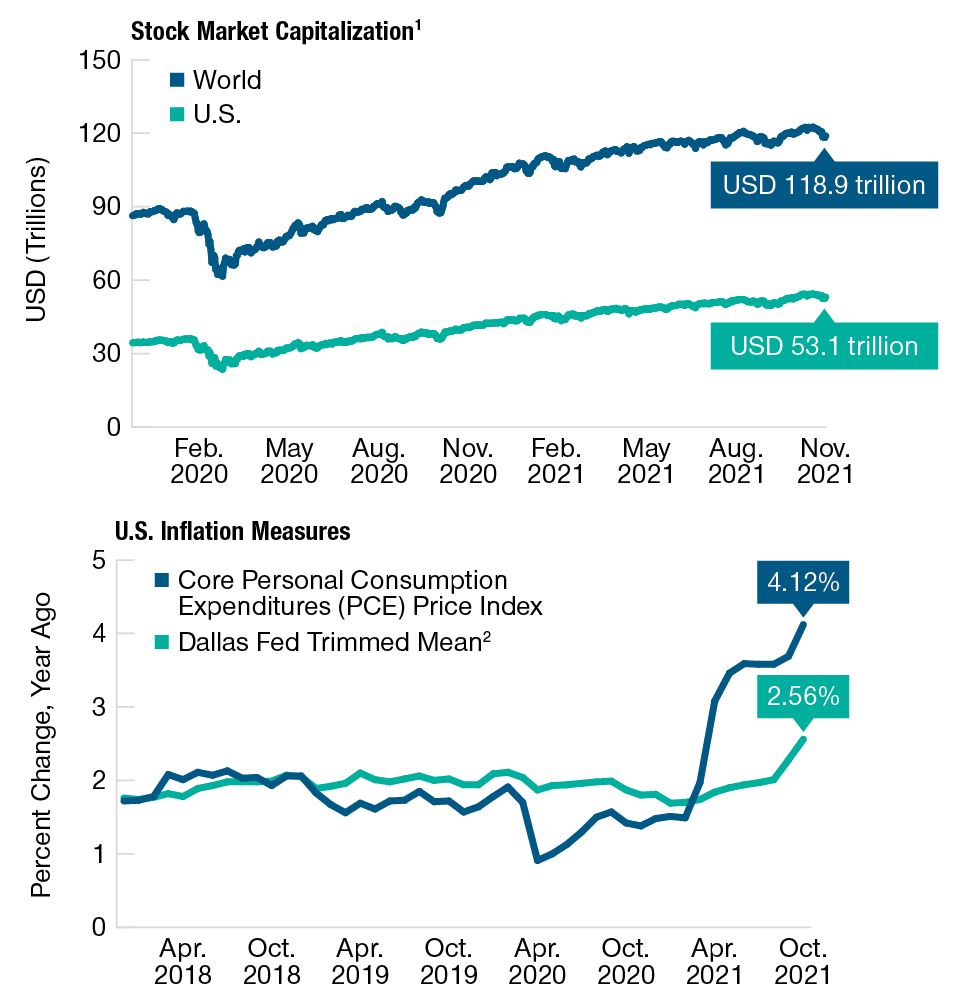

Wealth Effect Could Be a Tailwind for Growth—but Also for Inflation

(Fig. 2) Global and U.S. stock market capitalization and core measures of U.S. consumer inflation

Past performance is not a reliable indicator of future performance.

Market capitalization data as of November 30, 2021. Inflation data as of October 31, 2021.

1Bloomberg World Exchange Market Capitalization. Tickers on Bloomberg: Market Cap: WCAU (World) and WCAUUS (United States).

2The Dallas Federal Reserve Bank’s PCE trimmed inflation rate is designed to exclude extremely low or extremely high changes among 178 goods and services series tracked by the U.S. Bureau of Economic Analysis’ PCE Chain‑Type Price Index in order to smooth volatility and show the underlying inflation trend. These 178 categories add up to roughly 100% of nominal personal consumption. On average since 2009, the calculation has trimmed 24% of expenditures from the lower tail of the distribution of price increases and 31% from the upper tail.

Sources: Bloomberg Finance L.P., Bloomberg Index Services Limited (see Additional Disclosures), U.S. Bureau of Economic Analysis, and Federal Reserve Bank of Dallas.

Unless pandemic conditions deteriorate significantly, improving global supply chains and factory reopenings could ease the upward pressure on prices in 2022, Page suggests.

Much of the 2021 inflation surge, he notes, was concentrated in specific products—such as used cars and gasoline—that were particularly hard hit by supply/demand imbalances. The hefty price hikes in these goods seen in 2021 are unlikely to be repeated in 2022, he argues.

The bad news: Prices for many other key items—such as some foodstuffs, rent, apparel, and airfares—have lagged broader inflation. As higher energy costs and the appreciation in home prices ripple through the economy, price increases for these goods are likely to play catch‑up, Vaselkiv warns. Rents, in particular, appear poised to accelerate in 2022, Page adds.

Rising wages could present a longer‑term structural inflation risk, Vaselkiv says. While faster income growth should help support consumer spending, it could contribute to a wage‑price spiral as businesses pass along higher costs—in turn putting more upward pressure on wages.

“If inflation starts to permeate into wages, and that starts to drive inflation expectations, then maybe inflation will not be as transitory as we thought,” Thomson adds.

Demographic and labor market trends could heighten that risk. Vaselkiv notes that occupations in a number of key sectors—including transportation, health care, and education—are seeing a wave of retirements, or soon will, as the baby boomer generation passes out of the workforce.

Meanwhile, large companies with deep pockets, such as Amazon, can afford to raise wages aggressively to attract the workers they need, Vaselkiv says. Other service industries and smaller companies could be hard pressed to compete.

“Profit margins have been very high for very long,” Vaselkiv notes. “But now the pendulum is swinging from capital to labor.”

For illustrative purposes only. This is not intended to be investment advice or a recommendation to take any particular investment action.

Focus on Fundamentals

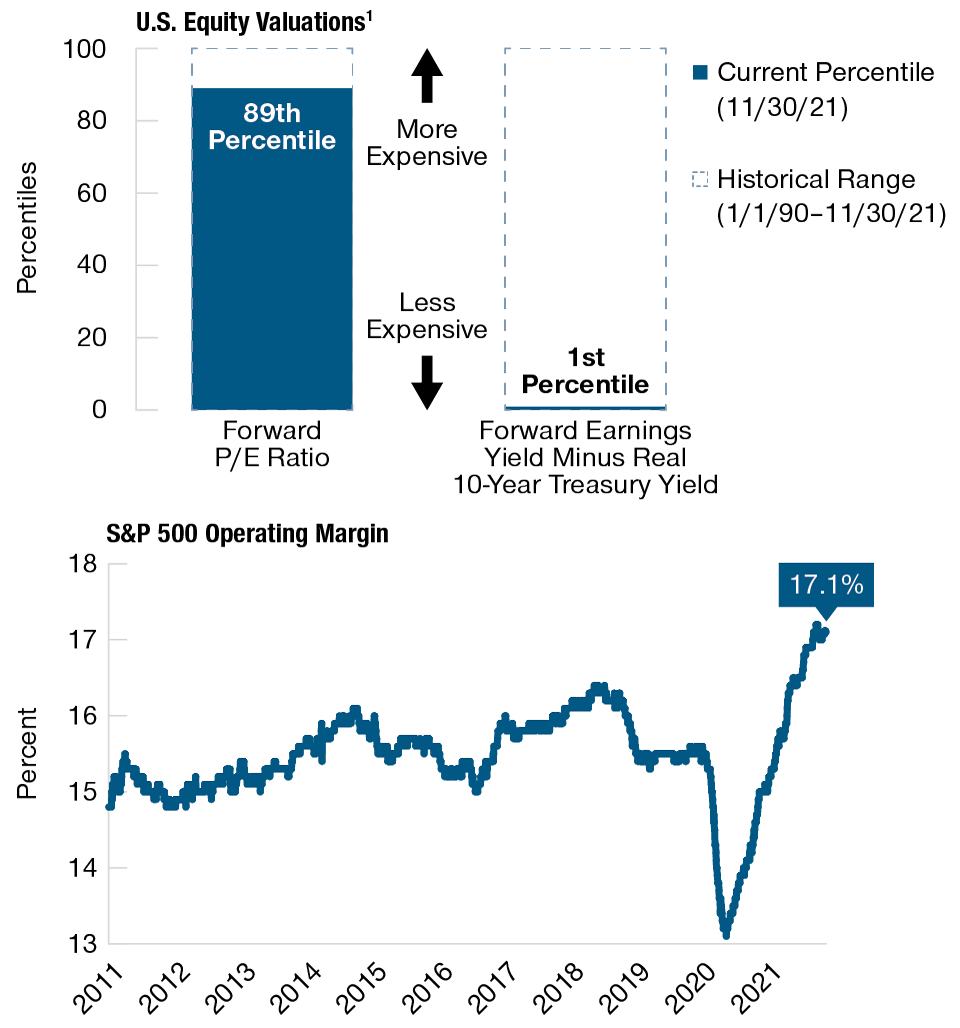

Global equity markets demonstrated resilience in 2021, although the rise of the omicron variant put a damper on optimism as the year drew to a close. Looking ahead to 2022, the question is whether earnings growth will continue to support U.S. equity valuations that appear stretched in absolute terms.

Although signs of speculative excess abounded in 2021 in areas like cryptocurrencies and nonfungible tokens, the U.S. stock market did not appear to be in bubble territory, Page asserts. But equity valuations were a bit of a puzzle, he says.

- As of mid‑November 2021, the price/earnings (P/E) ratio on the Russell 3000 Index was almost at the top of its historical range since 1989.

- Relative to real (after‑inflation) bond yields, however, the index’s earnings yield was in the least expensive percentile for that same period.

“So I can say that U.S. stocks looked almost as expensive as they’ve ever been, but also almost as cheap as they’ve ever been, and both statements are technically correct if you look through the right lens,” Page observes.

Much will depend on the strength of earnings growth in an environment where the spread of coronavirus variants and the potential for rising interest rates both pose significant—if contrary—risks to the global economic recovery.

Throughout most of 2021, U.S. equity gains were supported by a steady stream of upward earnings revisions, Thomson notes. Despite a nearly 23% rise in the S&P 500 Index in the first 10 months of the year, the index P/E actually fell over that same period as earnings rose faster than stock prices.

If the recovery remains on track, earnings growth should continue in 2022, Thomson predicts. But with S&P 500 operating margins at a record level, U.S. earnings momentum is likely to slow. “The starting point for profitability is very high,” Thomson says. “It’s going to be a hard hurdle to beat.”

Although Stocks Do Not Appear Expensive Relative to Bonds, Earnings Momentum Could Slow

(Fig. 3) Distribution of U.S. equity valuations and operating margin for companies in the S&P 500 Index

As of November 30, 2021.

1Valuation measures are based on the Russell 3000 Index. Stock versus bond yield percentile has been reversed.

Sources: Bloomberg Finance L.P., Strategas Research Partners, and Standard & Poor’s (see Additional Disclosures); data analysis by T. Rowe Price.

Beyond 2022, the hurdles look even tougher to clear, Thomson warns. “The next two to three years could be very difficult from an earnings growth perspective. At a minimum, we could well see below‑normal growth. But the stock market simply has not factored that in.”

Slowing earnings momentum also is likely to produce more uneven results across companies, Thomson says, requiring investors to be more selective but potentially creating opportunities for active portfolio managers to add value for their clients.

Likewise, rising costs could put a premium on stock selection skill. “Companies that can pass through inflation should continue to see earnings growth,” Thomson says. “But for companies that don’t have pricing power, it could be an issue.”

The earnings picture for ex‑U.S. equities is more mixed, Thomson says. While earnings growth has been surprisingly strong in Europe, momentum in Japan has been slowed by a sluggish domestic economy.

Looking to 2022, however, Thomson suggests that Japan could offer potential relative valuation opportunities if the global recovery remains on track, as could equities, credit, and currencies in select emerging markets (EM). A contrarian case can be made for Chinese equities, he adds, as Beijing moves to restimulate an economy that appears close to stall speed.

Valuation fundamentals and cyclical factors could favor the “recovery trade” in 2022, Page says. Financial stocks, which carry a heavy weight in the value universe, historically have tended to outperform in a rising interest rate environment, he observes. And small‑cap stocks typically have done well during economic recoveries.

In a period of rising rates and higher inflation, the growth style could underperform, Thomson concedes. This could have implications for key growth sectors—technology in particular—that have led equity markets for much of the past decade.

“Companies that can grow earnings persistently over a long period of time are extremely rare,” Thomson says. “So I think the odds that technology will continue to be a dominant sector are rather low.”

For illustrative purposes only. This is not intended to be investment advice or a recommendation to take any particular investment action.

Navigating Policy Shifts

With inflation emerging as both a leading investment risk and a hot political issue, a turn toward higher interest rates appeared to be underway as 2021 ended. Yet, with COVID‑19 still clouding the outlook, global central banks were moving at different speeds.

As usual, the Fed holds center stage. As of late 2021, market expectations were rising that the Fed would begin tapering its quantitative easing bond purchases at a faster pace early in 2022.

But there may be a disconnect between investor perceptions of Fed policy and the inflation expectations priced into fixed income yields.

According to Vaselkiv, many investors came to the conclusion in the second half of 2021 that Fed Chairman Jerome Powell was being “irrationally dovish” in continuing to focus on U.S. unemployment even as inflation accelerated.

But Thomson argues that market indicators as of mid‑November 2021 were reflecting a less bearish view. “Whether it’s long‑dated rates or Treasury Inflation Protected Securities, the markets are saying that inflation is a transitory effect.”

A key question could be whether market expectations are compatible with the Fed’s 2% long‑term inflation target, Page argues. While that target is flexible, five‑year break‑even rates (the spreads between yields on TIPS and on regular Treasuries with equivalent maturities) as of mid‑November 2021 suggested that the market was anticipating 3% U.S. consumer inflation. The Fed’s credibility could be on the line.

“There’s being flexible around 2%, and then there’s letting inflation average 3% over the next five years,” Page observes. “Something will have to give.”

Vaselkiv says he sees two potential interest rate scenarios for 2022:

- The Fed remains too dovish for too long, causing the yield curve (the spread between short‑ and long‑term Treasury yields) to steepen. That could push the benchmark 10‑year U.S. Treasury yield above 2%.

- The Fed is forced to raise rates faster—and possibly higher—than markets expect. In that scenario, the yield curve could flatten and the 10‑year Treasury yield could fall as investors begin to anticipate a negative shock to growth.

While continued strong economic growth and inflation potentially could pose significant risks for U.S. Treasuries and other low‑yielding sovereign sectors in 2022, they’ve produced something close to “nirvana” for global credit investors, Vaselkiv says.

Recent indicators of corporate credit quality reflect that blissful state, Vaselkiv notes, with the default rate on floating rate bank loans below 1% as of mid‑November 2021 and the upgrade/downgrade ratio among U.S. high yield issuers approaching 1.8‑to‑1.

Some Central Banks Have Raised Rates, but Credit Conditions Appear Favorable

(Fig. 4) Interest rate actions by global central banks and upgrade/downgrade ratio for U.S. high yield issuers

Interest rate actions as of September 30, 2021. Interest rate actions show the number of rate cuts and rate hikes made by all central banks globally.

Upgrade/downgrade ratio as of October 31, 2021. The ratio shows credit rating upgrades to downgrades.

Sources: International Monetary Fund, CentralBankRates, J.P. Morgan North America Credit Research (see Additional Disclosures), and T. Rowe Price.

In Vaselkiv’s view, floating rate bank loans could offer particularly attractive potential opportunities in a rising interest rate environment because their rates typically reset every 90 days, giving them the shortest duration of any credit sector.

But history suggests that ideal credit conditions don’t last forever, Vaselkiv cautions. The dynamics supporting credit quality—ample liquidity, solid earnings growth, low balance sheet leverage—also could facilitate a shift to riskier financial practices.

“I see a flashing yellow light that over the next year or so credit quality could begin to deteriorate,” Vaselkiv says, as companies use low‑cost debt to pursue merger and acquisition deals and banks offer easier financing for private‑equity transactions.

With credit spreads (the yield differences between bonds that carry default risk and comparable U.S. Treasury securities) historically tight across nearly every U.S. credit sector, investors may need to cast a wider net in 2022.

EM corporate debt is the one global credit sector that still appears extremely cheap, especially in Asian markets, Vaselkiv contends. However, a positive outcome for Asian credit in 2022 will require a successful stabilization of China’s economy, he adds.

For illustrative purposes only. This is not intended to be investment advice or a recommendation to take any particular investment action.

Path to Global Sustainability

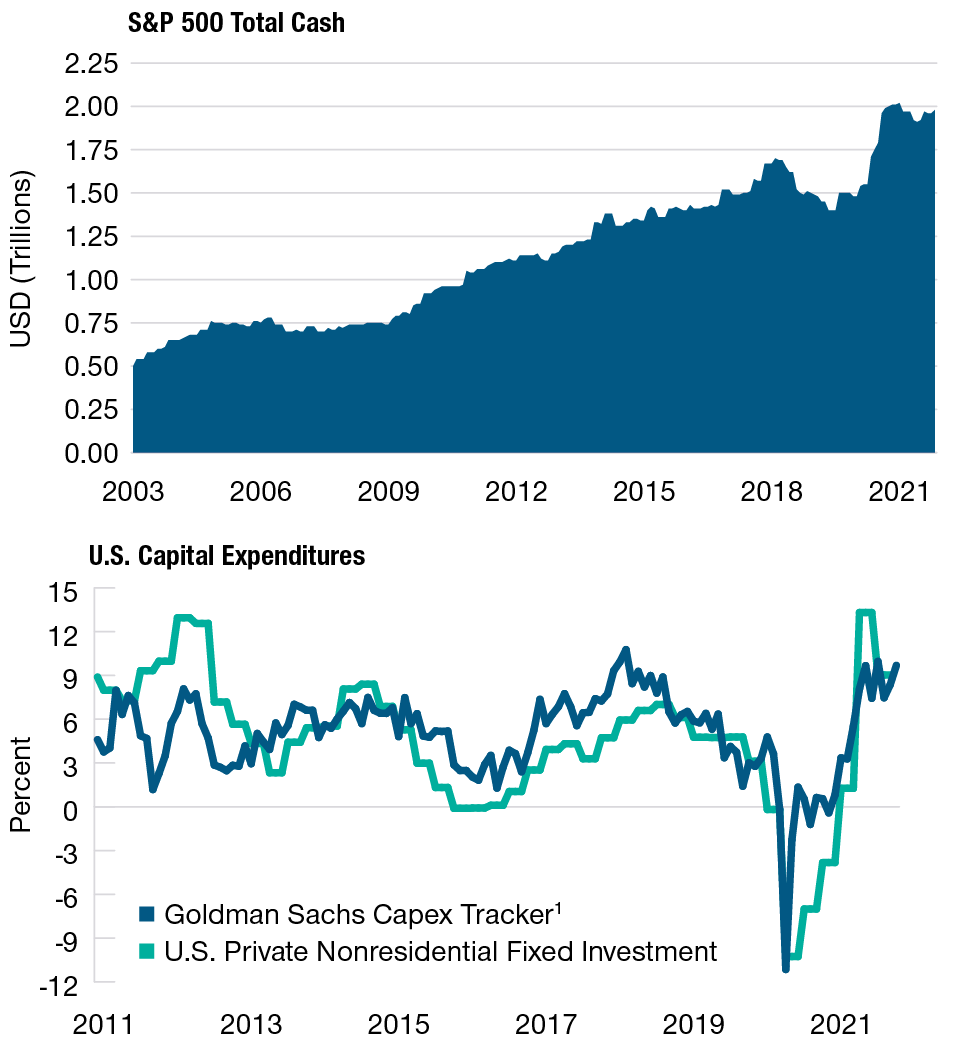

Vulnerable supply chains, crumbling infrastructure, higher energy prices, and a longer‑term need to reduce carbon emissions all have helped push economic sustainability to the forefront of the global policy agenda, T. Rowe Price investment leaders say. This could boost public and private fixed investment in 2022, supporting economic growth.

“It may be that we’re in for a paradigm shift here,” Thomson says. “You can certainly make the case for a sustained period of high capex [capital expenditures].”

Global corporations appear to have ample resources to finance fixed investment, thanks to strong earnings, spending restraint amid the pandemic, and a surge in low‑cost borrowing. The cash holdings of the companies in the S&P 500, for example, totaled nearly USD 2 trillion at the end of September 2021.

U.S. Corporations Are Flush With Cash, Leaving Them Well Postioned to Finance Capital Spending

(Fig. 5) Cash holdings of S&P 500 Index companies and 12‑month percentage change in U.S. capital expenditures

Cash holdings as of November 30, 2021. U.S. fixed investment as of September 2021. Goldman Sachs Capex Tracker as of October 2021.

1The Goldman Sachs Capex Tracker is a monthly index based on 15 U.S. investment‑related indicators such as loan demand and capital goods orders.

Sources: Strategas Research Partners, Goldman Sachs Global Investment Research (see Additional Disclosures), and U.S. Bureau of Economic Analysis.

Corporate spending on fixed investment has been relatively restrained for the past several decades, Thomson notes, in part because new technologies enabled companies to boost productivity and profitability without heavy capital outlays.

But that may be changing. Economic recovery spurred a sharp cyclical acceleration in capex in 2021. The push for sustainability, Thomson suggests, could generate a more extended wave of investment in physical infrastructure—ports, highways, power grids, etc.—and in capital goods manufacturing.

Thomson identifies several trends he thinks have the potential to drive capex, including:

- Meeting the international target of “net zero” carbon emissions by 2050 will require heavy investments in utilities, the automotive sector, and green technologies.

- Ports and maritime fleets need to be expanded to bolster global supply chains; onshoring those supply chains could boost demand for warehouses, rail and truck delivery, and domestic factories.

- Upward pressure on wages could produce a substitution effect as companies try to replace labor with capital, spurring investment in factory robots and other automation equipment.

- Companies may decide to rebuild depleted inventories, which in turn could spur investment in new productive capacity.

- Fiscal policymakers appear more relaxed about spending, debt, and inflation. This could clear the way for public infrastructure spending—like the USD 1 trillion package passed by the U.S. Congress in late 2021.

For investors, these trends could generate potential opportunities in both equity and credit markets in 2022.

A capex boom could be expected to boost sales and earnings for capital goods manufacturers, Thomson notes, to the potential advantage of stock markets in Germany and Japan, which host some of the world’s leading industrial companies.

European banks, which have carved out a major role in financing investments in solar, wind, and other renewable energy sources, also could be indirect beneficiaries, Thomson adds.

Financing “transformational” industries has long been a core competency for high yield debt markets, Vaselkiv argues—as evidenced by the role that high yield financing played in getting the electric vehicle industry off the ground.

“This could be an exciting decade as we move from traditional carbon fuels to cleaner sources of energy,” Vaselkiv says. However, demand during that period also could be high for “transitional” fuels, particularly natural gas, he suggests. This likely would require substantial investment in gas production and distribution. “I think global high yield markets are well positioned to provide that capital.”

The runup in energy prices seen in 2021 also could help reduce carbon emissions, by restraining demand for oil and making renewable sources more competitive, Page notes.

To a considerable extent, Vaselkiv adds, higher energy prices are the product of a steady decline in oil and gas investment—partly driven by pressure from activist shareholders but also reflecting the industry’s poor profitability.

“Some of these companies haven’t generated free cash flow for years,” Vaselkiv says. “You look at some of the major oil players, and their stocks are significantly below where they were five years ago—in the middle of one of the great bull markets in history.”

For illustrative purposes only. This is not intended to be investment advice or a recommendation to take any particular investment action.

Summary

For the better part of the past two years, the global market outlook has been dominated by COVID‑19. While the omicron variant—and the possibility of renewed lockdowns—are still threats, the primary economic focus for 2022 has shifted to the risks that higher inflation and interest rates could pose for growth and asset returns.

Those concerns have put the spotlight squarely on the world’s central banks, particularly the U.S. Federal Reserve.

So far, the Fed’s go‑slow approach to tightening has avoided a repetition of the 2013 “taper tantrum.” But it looks increasingly out of step with the inflation fundamentals, Vaselkiv argues. “I think the probabilities of major policy mistakes are very high.”

Policy uncertainty is highlighted by a stark contrast between an accelerating U.S. consumer price index and nominal bond yields that as of mid‑November 2021 appeared to reflect much more benign expectations. How—and when—that contradiction is resolved could determine the performance of sovereign and investment‑grade credit sectors in 2022.

“It’s hard to disagree that bond valuations look stretched when real rates are near all‑time lows,” Page contends. “The bond market appears to have priced in an extremely dovish Fed and a sharp deceleration in growth.”

Barring a return to widespread pandemic lockdowns, the coming year could offer relatively favorable prospects for global equity and credit investors, T. Rowe Price investment leaders say, if pent‑up consumer demand, stabilization in China, and a potential upswing in fixed investment can—as they expect—sustain economic growth.

But, even if growth remains strong, it would be a mistake to assume the impressive U.S. earnings momentum seen in 2021 will extend into 2022, Thomson warns:

- There appears to be little room for margin expansion—especially if wage costs continue to rise quickly.

- While some industries, such as aerospace, airlines, hotels, and cruise lines, have lagged in the earnings recovery so far—potentially leaving room for positive momentum—they account for relatively small shares of S&P 500 capitalization.

Continued cyclical expansion, but with slower U.S. earnings growth, could bring to an end an exceptionally long period of U.S. equity outperformance over ex‑U.S. equities, Thomson suggests.

As noted by Page, negative real U.S. interest rates have lent critical support to historically stretched equity valuations. But in periods of rising rates, Thomson warns, “high valuations can become an albatross.”

Accordingly, Thomson argues, relative valuation considerations could favor less expensive, more cyclically exposed markets in 2022—such as Japan and the emerging markets, including China—that appear positioned to benefit from stronger global capital spending.

In an uncertain policy environment, asset allocation could be especially crucial for managing investment risk going forward, Page says. But that may require a more dynamic diversification approach than the traditional 60/40 stock/bond portfolio—and a broader mix of fixed income sectors than the typical “core” investment‑grade bond allocation.

“With real rates this low, we have to acknowledge that bonds may not diversify stocks as well as they have in the past,” Page says. “My view is that the 60/40 portfolio needs to be reoptimized for the current environment.”

2022 Tactical Views

1For pairwise decisions in style and market capitalization, boxes represent positioning in the first asset class relative to the second asset class.

The asset classes across the equity and fixed income markets shown are represented in our multi-asset portfolios. Certain style and market capitalization asset classes are represented as pairwise decisions as part of our tactical asset allocation framework.

This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action.

Important Information

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

USA—Issued in the USA by T. Rowe Price Associates, Inc., 100 East Pratt Street, Baltimore, MD, 21202, which is regulated by the U.S. Securities and Exchange Commission. For Institutional Investors only.

© 2025 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.

December 2021 / INVESTMENT INSIGHTS