September 2021 / INVESTMENT INSIGHTS

China: Why It Pays To Look For The Overlooked

China is an economy and market that is constantly changing.

When thinking of China, most investors will be familiar with the mega-cap stocks that dominate the MSCI China Index. They will likely already have allocations to these companies as part of their emerging markets or Asia exposure. However, as we have noted previously the investment universe for China is multiple times larger than the mega-caps and warrants a deeper look as a standalone strategy for your China exposure. A holistic approach to the full opportunity set of investable stocks available in China, regardless of where they are listed, could enable you to maximise alpha generation within your portfolio.

By focusing on the less well-known or under explored areas of the market, research-driven active managers can uncover idiosyncratic companies in nascent growth stages while simultaneously exploiting the inefficiencies that lie in these under-researched parts of the market.

Outliers: critical source of alpha generation

The narrowness of the recent performance of China’s stock market mirrors the experience of other markets where a relatively small number of companies have delivered spectacular returns driving up the wider market.

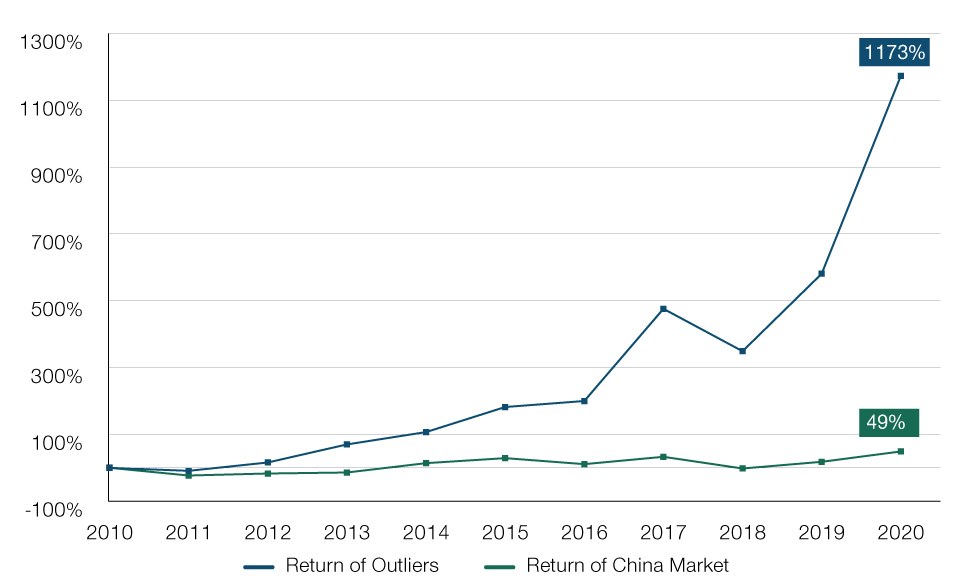

Analysing the past 10 years of performance for the Chinese market (to 31 December 2020), we noted that there are very few companies that we would consider to be such outliers (defined as those companies delivering at least 20% p.a. share price returns). In fact, of the 2,494 listed companies at the start of the period, we estimate that there were only 86 companies (3%) which achieved ‘outlier’ status. However, they accounted for an astonishing 87% of the broader market’s total gains over that period (see Fig. 1).

Fig 1: The majority of market return has been driven by outlier companies

10-year returns: outliers vs market

Past performance is not a reliable indicator of future performance.

Outliers: stocks compounded at 20%+ CAGR during 2011-2020

China Market: 2494 Chinese stocks listed before 2011

Sources: Goldman Sachs, FactSet. Financial data and analytics provider FactSet. Copyright 2021 FactSet. All Rights Reserved

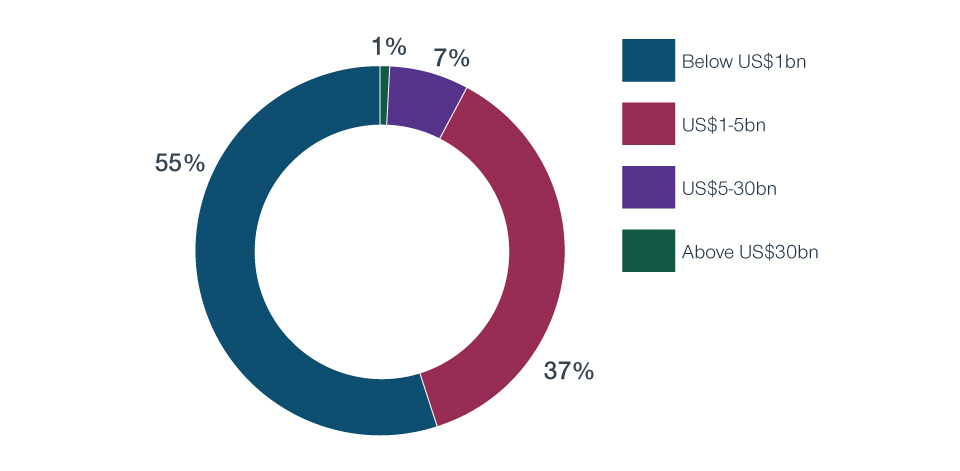

Examining their characteristics it is evident that they have some common traits, however – perhaps the most significant is that all bar one started out with a market cap below US$30 billion at the beginning of the review period. The average starting market cap was just US$2 billion.

Fig 2: Outliers by market cap

As at 31 December 2020

Sources: Goldman Sachs, FactSet. Financial data and analytics provider FactSet. Copyright 2021 FactSet. All Rights Reserved.

China is an economy and market that is constantly changing. The status quo does not last long. Whilst disruption is commonplace, the majority of assets under management invested in China appear concentrated in the overcrowded mega-cap space. Most investors seem to be ignoring the many diversified sources of alpha across this vast opportunity set that offers scope for a more balanced alpha generation and better up/down capture. As such, we believe it is important to look outside of today’s dominant mega-caps to unearth the companies that will become tomorrow’s winners.

By taking such an approach, investors can benefit from access to innovative companies that operate in niche or early-stage industries, or in more traditional industries that may be highly fragmented where through consolidation they can take market share and experience rapid growth. This can be powerful since China is home to many nascent industries where market leaders have less than 5% market share. It also means exploring opportunities across the full supply chain. Taking Electric Vehicles (EV) as an example, it’s not about buying the EV manufacturer, but about buying a company that makes the components that go into the EV – from glass, to headlamps, to semiconductors.

Smaller does not necessarily mean riskier

Crucially, delving deeper in China doesn’t necessarily mean investing in small, illiquid or riskier stocks. Instead, we would put it another way: it means having the forward-looking vision to invest in tomorrow’s mega-caps while they are still in the early stages of their development.

China is a highly liquid market, driven in part by the behaviour of local retail investors. There are approximately 500 companies with a market capitalisation between US$5-30 billion, and thousands more in the US$1-5 billion bracket. Our analysis of volatility among Chinese stocks above and below US$30 billion market cap, shows that both groups displayed different characteristics at different periods, but notably when the <US$30 billion bucket exhibited more volatility than the >US$30 billion bucket, it tended to be lower than when the larger caps stocks went through a period of heightened volatility. In the case of China, investors should not jump to the conclusion that smaller cap stocks exhibit higher volatility.

In our view, the deeper reaches of the China equities market offer access to tomorrow’s mega-caps that can complement many investors’ existing allocations. Fundamental investors with a longer-term investment horizon who can identify those companies where change and growth are under-appreciated or undiscovered, have the potential to construct a diverse portfolio of uncorrelated, and idiosyncratic, growth opportunities.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

September 2021 / POLICY INSIGHTS