November 2020 / INVESTMENT INSIGHTS

Finding Alpha in an Increasingly Concentrated U.S. Market

The rules of the game in the large cap growth space have changed

Key Insights

- The U.S. equity market has become increasingly concentrated in recent years, due principally to the stellar growth of a handful of large‑cap growth companies.

- This has effectively changed the investment landscape, with success now largely dependent on making the right decisions on a small group of dominant companies.

- In terms of valuations, market movements in recent months have been driven by further multiple expansion to levels that, in our view, appear unsustainable longer term.

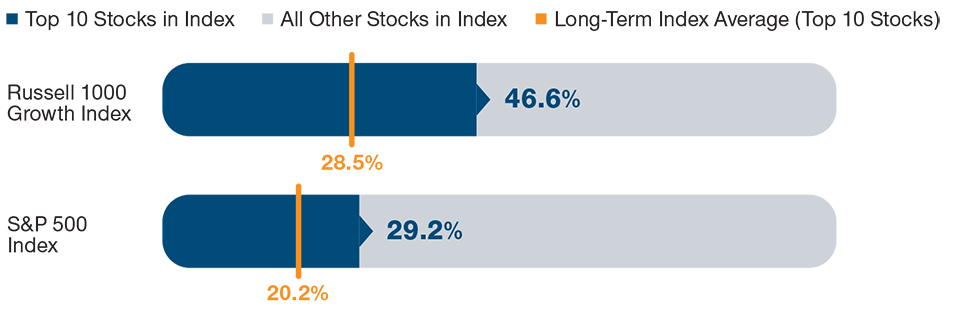

Amid the wider performance of the U.S. equity market, one particularly astonishing statistic is that the top 10 stocks in the S&P 500 Index now account for almost 30% of the entire index value. The picture is even more stark for the Russell 1000 Growth Index, with close to half of the entire index value concentrated in the 10 largest constituents.1

U.S. equity market concentration has been gradually increasing since the global financial crisis, but in recent years, it has become more acute. Much of the rise in concentration can be attributed to just five stocks—Facebook, Amazon, Apple, Microsoft, Google/Alphabet—the so‑called FAAMGs, which have experienced dramatic increases in their market capitalization. The increasingly concentrated market raises concerns about the broader market being vulnerable to the performance of the dominant few. It also creates distinct challenges for identifying alpha opportunities across the broader large‑cap universe.

Understanding the Risks by Isolating the Sources of Growth

In thinking about the potential risks posed by heightened market concentration, there are two important questions to consider.

The first is: How much of the rise in index concentration is due to the natural topline growth of companies versus that which is due to companies being reweighted higher in the index? Within the Russell 1000 Growth Index, for example, certain companies have been significantly reweighted higher in recent years, simply by virtue of their higher stock price. Apple is perhaps the prime example of this kind of concentration effect. In contrast, Amazon is a stock that has seen only relatively modest increases as a result of index reweighting and has instead been driven by underlying growth in revenue and earnings.

Just 10 Stocks Dominate the Composition of Key Indexes

(Fig. 1) Proportion of top 10 stocks* in Russell 1000 Growth Index and

S&P 500 Index

As of August 31, 2020.

*By market capitalization.

Source: T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved.

(See Additional Disclosures.)

The second question is whether the concentration is being driven by a divergence in the multiples of the companies involved. The point here is that market concentration itself is not necessarily an issue—it becomes problematic when it is driven by a small number of companies increasing their weight within the index solely due to multiple expansion, rather than as a result of an actual improvement in underlying cash flows or earnings. This is the scenario we are starting to see currently, and it is cause for concern, in our view.

Getting the Big Decisions Correct Has Become Paramount

As an active manager, our goal remains unchanged—singularly focused on generating alpha for our clients versus the index and, hopefully, with a lower level of volatility. That said, in terms of decision‑making, a highly concentrated market presents a very different investment landscape compared with a more normalized, diversified market.

In a normal environment, investing is all about maintaining a high average—that is, getting more investment ideas right than wrong, across the market. However, when certain stocks become very large weightings within the benchmark, the rules of the game change. Rather than a game of averages, success is much more about making the right decisions on a smaller group of large companies. In the current environment, this means getting the big decisions right on the FAAMGs over the next three to five years is paramount.

Valuation Multiples Continue to Expand—The Underlying Reasons Matter

In trying to assess the sustainability of current valuations, it is important to consider the various factors that drive market multiples.

Growth Valuations Have Risen Sharply in 2020

(Fig. 2) Russell 1000 Growth Index—P/E ratio spikes to 32x

As of December 31, 1997 to August 31, 2020.

Source: T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved.

(See Additional Disclosures.)

Interest rates have played a significant part in current equity market valuations. The U.S. Federal Reserve’s policy of low (and persistently low) rates has placed upward pressure on market multiples, which has been more acutely felt by higher-growth companies. There are other factors that can impact the multiples, namely volatility and the cyclicality of earnings, but these are less influential currently. Take earnings, for example: We are some 10 years into a recovery and far from the bottom in terms of the kind of depressed earnings levels that would serve to elevate multiples.

Looking at the current level of U.S. equity market multiples as recently as a couple of quarters ago, these seemed generally reasonable. However, more recent market movements have been driven by further multiple expansion to levels that now look more concerning. This is less perceptible for the S&P 500 Index but is particularly evident in the Russell 1000 Growth Index, given its greater exposure to high-growth companies. While this does not necessarily suggest a reversion in multiples anytime soon, we believe that the current levels are unsustainable over the long term.

Which of Today’s Large‑Cap Leaders Can Continue to Excel?

Can the large‑cap growth companies that have excelled over the past five to 10 years continue to lead the market over the next five to 10 years?

By virtue of the dominant positions of the two digital giants Google and Facebook, I believe they are likely to continue to gain market share and add more value via targeted advertising for the companies that use their services. Of course, this outlook does not account for any potential external factors, such as changes in regulation. Recently in Europe, for example, there has been discussion about potentially requiring certain companies to share their data on users with third parties in an attempt to level the playing field.

Elsewhere, Amazon has demonstrated an ability to reinvent itself and find novel areas of growth and momentum. We believe that Amazon’s vast logistics capabilities could be a meaningful driver of long‑term growth. In addition, Amazon’s advertising business, while still very small compared with Google and Facebook, could still grow.

In contrast, we believe there is a natural limit to the amount of market share that Apple can achieve as a hardware company in the mobile phone industry. If Apple is to continue to be as successful as it has been, over the next decade, in our view, it will need to develop a new product in a novel market area—similar to what it achieved with the iPad and the Apple watch. Apple either needs to develop some new product or service that we are not yet talking about or it needs to have great success with its recently launched Apple TV streaming platform.

Growth Multiples Are Looking Stretched

While concentration risk is not a new market phenomenon, it has become more acute in today’s U.S. equity market, due to the stellar performance of a handful of large‑cap growth companies within the consumer, media, and technology‑related industries. The success of these businesses is being driven by forces that are reshaping economies and markets. Through innovation and disruption of traditional business models, they are rapidly taking market share from long‑standing industry players, placing valuation and concentration considerations in a whole new context.

However, in recent months, we believe that growth benchmark valuation multiples have increased to levels that are unsustainable on a longer‑term basis. As such, we anticipate a reversion toward more normal valuation levels at some point. In the meantime, while there are still good growth opportunities to be found, investment success will largely depend upon getting the big decisions right on the index heavyweights.

T. Rowe Price beyond the numbers

Monitoring Growth Stock Multiple Expansion

Some companies are simply benefiting from the short‑term environment.

Since the onset of the pandemic, investors have effectively allocated companies into two distinct buckets: the winners and the losers. Those in the winners category have seen significant multiple appreciation as investors have assigned higher long‑term growth valuations. However, we are not convinced that this is always justified, with some companies simply benefiting in the short term. The opportunity presented by the pandemic has allowed them to pull forward free cash flows, which in turn, increases the company’s net present value. On this basis, investors are assigning higher long‑term valuations—valuations that, for some of these businesses, are unwarranted, in our view.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

November 2020 / MARKETS & ECONOMY