March 2021 / MARKETS & ECONOMY

Investing in a Pandemic: Lessons Learned and What’s Next

Disruption, speculation in markets, and themes to watch

Key Insights

- Our portfolios were largely well positioned for the acceleration in technological disruption caused by the coronavirus pandemic.

- I did not anticipate how quickly the economy and consumer spending would rebound thanks to massive stimulus.

- With investors having embraced risk with a vengeance, we are carefully watching clear signs of speculation in markets.

Just about a year ago, only days after we shifted to a remote working environment, I wrote a note to our investment teams across the globe. I urged them to focus on two things as they grappled with extreme market conditions.

“Keep a long‑term orientation, and remain grounded in the fundamentals,” I wrote.

So how did we do? And where do markets go from here?

Those are key questions we’re discussing right now. Reflecting on the investment decisions our portfolio managers made in the past year, there were many calls we got right. Admittedly, there were also outcomes we didn’t anticipate. As for what’s next, we are watching several developments, including clear signs of speculation in markets now.

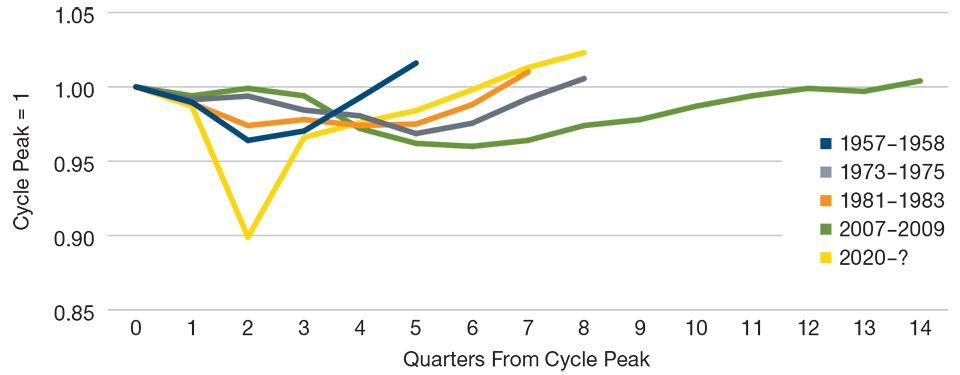

The Recovery’s Trajectory Has Been Unprecedented

(Fig. 1) Change in gross domestic product over deep postwar U.S. recessions

As of February 25, 2021.

Sources: Haver Analytics/U.S. Bureau of Economic Analysis, Bloomberg. Data analysis by T. Rowe Price.

The collapse in markets that unfolded in February and March 2020 quickly reflected the near‑term damage that the pandemic would ultimately inflict. However, the crash also created tremendous opportunities as price levels became disconnected from longer‑term prospects. Many of our portfolios were able to take advantage of these opportunities by repositioning and adding risk. Importantly, we maintained a keen focus on liquidity and balance sheet strength.

Throughout the volatility of last February and March, we identified market dislocations. We repositioned early and then added risk. One response I think our portfolio managers made correctly was staying rooted in company fundamentals and focused on the long term. Identifying companies with balance sheets they believed were strong enough to get to the other side was a particular focus.

Another series of prescient calls had its roots in a trend we’ve been focused on for some time: disruption.

In our 2020 Global Market Outlook, published in December 2019, we wrote, “Disruption has created a strong fundamental backdrop for its beneficiaries—such as the major technology platform companies—while curbing earnings growth for many incumbent firms trading at lower multiples.”

The pandemic, combined with low interest rates, accelerated this transformation. Nearly everything about how we work, socialize, learn, shop, and entertain ourselves has been rethought. We’ve been watching this trend for some time. We were largely positioned accordingly.

More recently, we identified opportunities across sectors, including health care and energy, and in fixed income markets, among municipals and high yield bonds. Our Asset Allocation Committee, which was overweight to growth for much of 2020, moved overweight to value in September last year when we thought cyclicals could benefit from pent‑up demand, an improving economy, higher rates, and further stimulus.

Yet, there have been developments that have been more challenging to anticipate, including the magnitude and the length of the pandemic. I wouldn’t have expected to be writing this follow‑up note one year later from my home office.

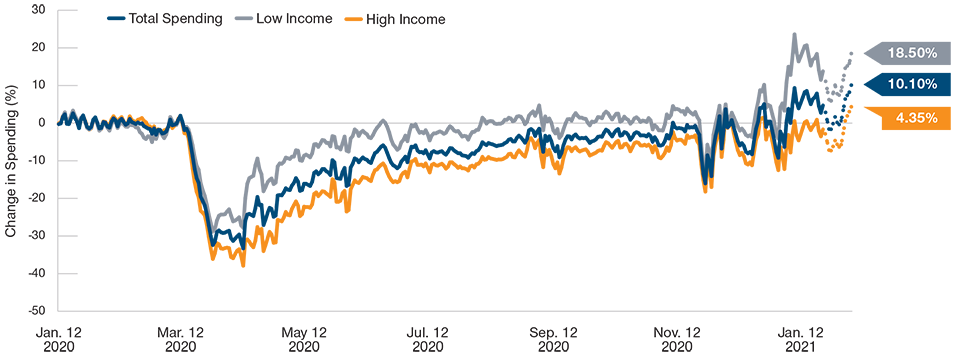

Stimulus Helped U.S. Consumers Rebound Quickly

(Fig. 2) Spending by income level

As of February 14, 2021.

Source: Percent change in consumer spending data compiled by Raj Chetty, John N. Friedman, Nathaniel Hendren, Michael Stepner, and the Opportunity Insights Team. February 14, 2020. Data available at tracktherecovery.org. Dotted lines represent provisional estimates from January 5, 2021 to February 7, 2021.

On the other hand, I also underestimated how rapidly the forceful policy response would fuel the market’s rebound. Central banks learned from the global financial crisis. They reacted quickly and powerfully.

Consumer spending also remained surprisingly resilient. I would have expected people to be more conservative. Second home markets, as one example, are buoyant.

The market’s recovery has been, in turn, swift and dramatic. While the turnaround in investor expectations has been logical in direction, its magnitude has surprised me.

We’ve transitioned from a period in March 2020 that was full of fear into a period now where speculation seems to be rampant and valuations by many measures are historically high. We’re not quite in a bubble in my view, but the breadth of the high valuations we see now is expansive.

Notably, the strong wave of COVID‑19 cases that peaked just after the holidays did not sidetrack the market. It was worse in terms of total cases than many of us expected and arguably led to a “COVID 2.0” recession.

Yet, because of the strength of the vaccines, anticipation of the release of pent‑up demand for goods and services, and the expectation that central banks will keep rates low for the foreseeable future, investors seem to have looked beyond the otherwise negative headlines.

However, we may be in a period where we’ve swung too far. Valuations are expensive under all but the most optimistic scenarios. Current conditions can persist for a while, but sustained gains will be harder to identify.

So where do we go from here as investors?

Broadly, there are four key themes we’re watching. First, we think it will be an uneven road to recovery, meaning there will be periods of volatility as we get back to a new normal and especially as much of the recovery has been priced into markets. Second, politics and the Biden administration’s emerging priorities will remain in the spotlight. Third, investors will need to be creative as they search for yield in this low rate environment. Fourth, disruption will continue, which in turn should create style dispersions, such as we’ve seen recently with recent stronger returns in small‑cap and value.

It’s a time to be careful, however. There are clear signs of speculation in markets. The rapid rise of cryptocurrencies and capital formation through less conventional vehicles are two that have my attention.

One key risk that we’re watching: signs of inflation. It’s hard to know when the current regime will end, but if inflation rises meaningfully, it will be a whole new environment for financial markets.

The one thing we can say is that we won’t have continued disinflation in the near term. Longer term, markets will no longer have the tailwind of falling rates, although they could remain at historically low levels if the inflation impulse fades.

What we’re watching next

Four risks—both downside and upside—that we’re watching in addition to the eventual end of the accommodative era.

- Geopolitical hot spots that grabbed headlines in early 2020 have been bumped from the front page, but they have not disappeared.

- What happens to tax rates will be front and center, including the potential for higher corporate rates and tax rates on dividends for individuals.

- The U.S.-China trade war might intensify or establish new fronts.

- The Biden administration may prove less market friendly, but some cabinet appointments, such as Janet Yellen as Treasury secretary, point to moderation.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.