INVESTMENT INSIGHTS

How EM Investors Can Succeed in a Dovish Monetary Backdrop

August 2019

Andrew Keirle

, Senior Portfolio Manager

Key insights

- Despite growth concerns, we believe emerging markets (EM) can perform well as they form an important source of real income in a backdrop of low developed market government yields.

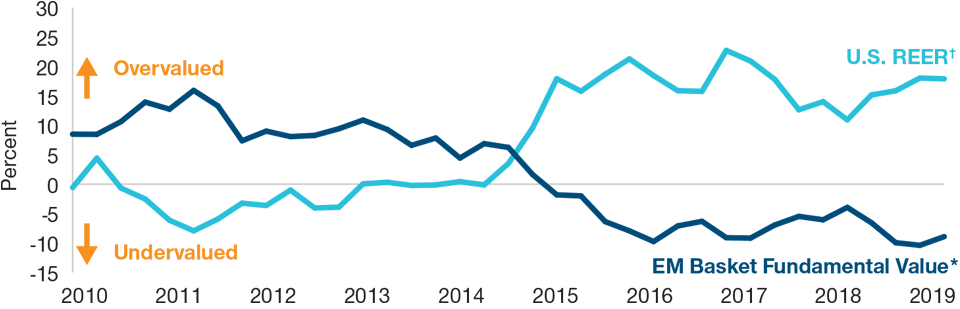

- Local currency assets could stand out if the U.S. dollar weakens. EM currencies lagged the rallies in early 2019 and are currently undervalued.

- However, EM are at risk should the macro backdrop shift. Investors should look beyond this near‑term binary choice of a risk‑on or risk‑off backdrop and seek out strong fundamentals.

The current emerging markets (EM) backdrop can appear puzzling at first glance. On one hand, dovish central bank policies could boost EM assets. However, global growth uncertainty and trade wars dominate headlines. Should investors be looking to reduce EM risk exposure? Or should they follow the axiom of “don’t fight the Fed” and expect central banks to support a risk‑on backdrop?

While conditions could spur further EM rallies this year, we maintain that EM investors should look beyond this binary choice of a risk‑on or risk‑off macro backdrop. There is a lot to like within EM themselves. Investors who seek out areas with strong long‑term fundamentals can help shield themselves from swings in macro sentiment.

Monetary Policy Creates Room to Run

Global central banks are giving investors reason to remain upbeat. Currently, the market anticipates that the Federal Reserve (Fed) could follow its July rate cut with additional cuts this year. The European Central Bank (ECB) is also talking about rate cuts or even restarting monthly bond purchases. Several other global central banks have either begun or are poised to ease policy in the coming months. While these easing measures are not certainties, major central banks are likely to take broadly accommodative stances as long as the economic picture remains mixed. Therefore, we are optimistic about EM for several reasons:

- EM asset classes could see further inflows. In the first half of the year, EM enjoyed strong fund flows, particularly hard currency assets, when the Fed and ECB began their respective dovish shifts. Going forward, global central bank policies will likely keep core government yields suppressed.

In a world of low, or even negative, developed market yields, EM can continue to attract investors because they form an increasingly rare source of positive real (inflation‑adjusted) income. Currently, the estimated value of global debt with a negative real yield is over USD 25 trillion.1 Should inflation rise when central bank easing takes hold, an even greater share of developed market debt would saddle investors with negative real yields. In this environment, securing much‑needed real income could become a larger focus for investors globally.

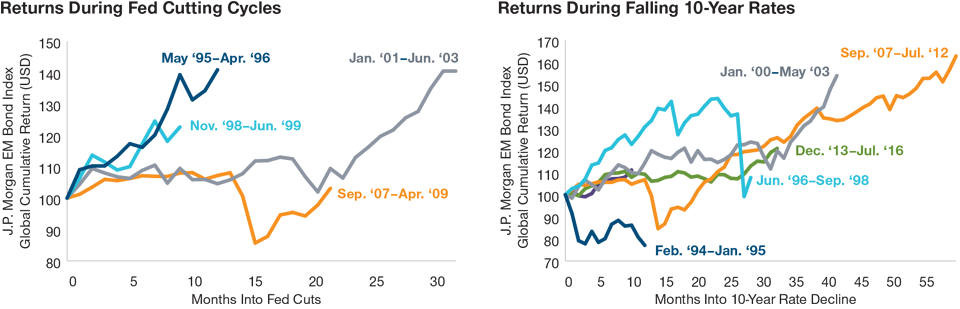

Furthermore, EM are still under‑owned. Although early 2019 saw steady inflows, retail investors have not returned to the levels seen before the 2018 volatility. Signs of committed loose policy stances by major central banks could provide the incentive to many hesitant investors. After all, historical data show that EM debt typically performs during Fed cutting cycles.

- Valuations in EM still look enticing. Even though valuations are not as cheap as they were at the start of the year, they have improved relative to developed markets in many cases. Also, EM asset prices do not yet reflect potential improvements in the growth outlook should stimulus take hold. The recent rallies have largely stemmed from developed market monetary easing expectations. Should growth data stabilize, asset prices could continue to rise.

Additional stimulus measures in China are also not yet priced into the market. So far, Chinese authorities have been cautious about adding monetary or fiscal stimulus. However, as economic concerns persist, authorities may adopt a more concerted approach to revive growth. This would give a boost to EM sentiment as Chinese growth remains an engine of EM economies.

- EM local currency assets could stand out. If the Fed remains dovish and EM growth is sustained, the U.S. dollar would likely depreciate against EM currencies. The greenback’s sustained strength in recent years has meant EM currencies lagged the rally in EM hard currency assets in early 2019. Consequently, local currency bonds and foreign exchange markets contain some of the more compelling opportunities should the dollar’s roughly seven years of strength fade in the next cycle.

(Fig. 1) Rate Cut Boosts for EM

EM debt* during Fed rate cuts and falling yields

As of June 30, 2019

Past performance is not a reliable indicator of future performance.

*EM debt refers to J.P. Morgan Emerging Market Bond Index (USD).

Source: J.P. Morgan (see Additional Disclosures).

(Fig. 2) EM FX Looks Attractive

EM currencies have been undervalued versus U.S. dollar

As of March 31, 2019

*EM Basket Fundamental Value = Average Misevaluation of currencies of Brazil, Chile, China, Colombia, Czech Republic, Hong Kong, Hungary, India, Indonesia, Israel, Malaysia, Mexico, Peru, Philippines, Poland, Romania, Russia, Singapore, South Africa, South Korea, Taiwan, Thailand, and Turkey.

†U.S. REER = U.S. dollar real effective exchange rate.

Sources: Thomson Reuters (see Additional Disclosures) and data analysis by T. Rowe Price.

Stay Alert to the Potential Risks

Investors should remain on guard for potential shifts in monetary policy or the economic outlook, which could disrupt EM. Those who focus solely on short‑term macro tailwinds are likely to get burned in the longer run.

- For one thing, EM assets would suffer if markets lose confidence in central banks’ ability to resurrect growth. Developed market central banks have less firepower than they have had in the past. The Fed’s recent tightening cycle was moderate, leaving interest rates at a historically low starting point. The ECB, meanwhile, did not even begin hiking rates and only ended its quantitative easing bond purchases at the end of 2018. Any restart of the quantitative easing program would likely be smaller in size. A further escalation in U.S.‑China tariffs would also hurt sentiment. EM could face volatility if economic data meaningfully deteriorate, sparking renewed recession fears.

- Alternatively, growth could improve more quickly than expected, prompting central banks to under‑deliver on their expected easing policies. This is concerning for EM given that much of the first‑half 2019 rally was based on expected EM rate cuts. While we would regard an improved growth outlook as a favorable long‑term trend, any sudden shift back to more hawkish central bank policy could trigger bouts of shorter‑term volatility.

- The U.S. dollar could also enter another period of strength should economic data in the country surprise materially on the upside or downside. Investors aware of the “dollar smile” concept are likely familiar with this already. The dollar smile posits that the greenback will appreciate during periods of either very weak or very strong U.S. growth. Currently, the economic data are mixed, and the dollar may weaken as investors look elsewhere for higher returns. However, a pronounced deterioration of the economy would trigger a flight to safe assets, such as the dollar. Conversely, a rejuvenated U.S. economy would also pull in investor money, causing the currency to appreciate as the Fed would likely become more hawkish. Therefore, investors need to be mindful of any sharp shifts, positive or negative, in the data.

Focus on Fundamentals

In the short term, EM could thrive in a mixed “not too hot, not too cold” global backdrop. However, we maintain that investors should look beyond the external macro drivers. By taking an active approach, investors should search for positives within EM and avoid the areas that may suffer most if macro sentiment shifts.

Fortunately, we identify several areas with strong or improving fundamentals even with the current economic concerns and policy uncertainty. Many countries, such as Indonesia and South Africa, are implementing constructive reform programs following recent elections, which could help improve stability through different market cycles. Several EM countries are displaying fiscal discipline, managing healthy external balances, and employing rational economic policies. These positive trends give countries like Brazil increased policy flexibility to cope with shifts in the external environment.

That is not to say these areas of EM won’t experience volatility. In our view, though, they can better withstand shifts in the macro backdrop and perform over the full market cycle while also benefiting from the near‑term central bank‑driven tailwinds.

WHAT WE’RE WATCHING NEXT

We are closely watching economic data in China. Growth indicators, particularly in the manufacturing sector, have trended lower for much of 2019. Despite more resilient data in the services and real estate sectors, a further deterioration in China purchasing managers index figures would likely trigger deepening concerns about the wider EM outlook. Furthermore, although talks remain ongoing, the recent escalations in tariffs on Chinese goods by the U.S. followed by a deterioration of the renminbi suggest a resolution is unlikely in the near term. However, if the data proceed on a downward trend, we will watch for the People’s Bank of China to possibly respond with more aggressive stimulus measures. This could form a silver lining as it could release some pent‑up demand following the extended period of soft data.

Additional Disclosures

Information has been obtained from sources believed to be reliable, but J.P. Morgan does not warrant its completeness or accuracy. The index is used with permission. The Index may not be copied, used, or distributed without J.P. Morgan’s prior written approval. Copyright © 2019, J.P. Morgan Chase & Co. All rights reserved.

Bloomberg Index Services Limited. BLOOMBERG® is a trademark and service mark of Bloomberg Finance L.P. and its affiliates (collectively “Bloomberg”). BARCLAYS® is a trademark and service mark of Barclays Bank Plc (collectively with its affiliates, “Barclays”), used under license. Bloomberg or Bloomberg’s licensors, including Barclays, own all proprietary rights in the Bloomberg Barclays Indices. Neither Bloomberg nor Barclays approves or endorses this material, or guarantees the accuracy or completeness of any information herein, or makes any warranty, express or implied, as to the results to be obtained therefrom and, to the maximum extent allowed by law, neither shall have any liability or responsibility for injury or damages arising in connection therewith.

Copyright 2019 © Thomson Reuters. All rights reserved.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

201908‑927752

RELATED FUND

SICAV

Class I

ISIN LU0310189781

An actively managed, diversified portfolio of the local-currency denominated bonds of emerging market sovereign issuers. The strategy seeks to provide generally lower levels of credit risk compared to external bonds, with meaningful opportunities in terms of local interest rate cycle and emerging markets currency exposure. Put simply, we aim to buy high quality businesses run by high quality people. The fund is categorised as Article 8 under Sustainable Finance Disclosure Regulation (SFDR).

View More...

View more information on risks

FACTSHEET