January 2021 / INVESTMENT INSIGHTS

Finding “Deeper Value” in Emerging Markets

Value-growth divergence may be peaking

Key Insights

- We search for “forgotten” stocks in emerging markets (EM) that we believe are under owned and underresearched and are about to experience fundamental change, with significant upside potential.

- After the pandemic‑related global sell-off and the resulting market dislocations, we identified better investment opportunities in “COVID‑off cyclicals.”

- 2020 has been a very tough year for our strategy, though the huge policy stimulus should help to reflate economies and allow value stocks to recover.

Value funds—whether global, developed, or emerging—encountered a major style headwind in 2020. Globally, economy‑sensitive value stocks underperformed during the coronavirus pandemic, which was to be expected. Value companies tend to be in traditional sectors that need growth in real economic activity to keep their earnings coming. With economies all but closing during their lockdowns, these companies could not generate earnings growth. Later, value stocks failed to rebound in the early phases of economic recovery, counter to historical experience. From a relative earnings perspective, the pandemic boosted e‑commerce, cloud computing and online services, and entertainment, favoring many of the large‑cap internet growth stocks that were market leaders prior to the pandemic. The result has been a market recovery characterized by concentrated sector leadership and narrow breadth that has been driven by COVID‑19 trades in addition to the value versus growth factor. In EM, growth had outperformed value by a record margin in 2020, the largest style divergence ever (Figure 1).

The shock of global recession this year was caused by the medical response to contain the coronavirus and not by the buildup of macroeconomic imbalances, the more traditional route. As such, it is likely to be relatively short, albeit deep, with the successful reopening of economies seen as depending on the distribution of an effective coronavirus vaccine. Here, the recent news has been very encouraging, with several effective vaccines available for widespread distribution this year. Add up the production plans of the major pharma companies involved, and global pharmaceutical production could be around 8.5 billion doses in 2021—enough to potentially inoculate over half of the world’s population.

EM Value-Growth Style Divergence Is Extreme

(Fig. 1) Calendar year value-growth divergence (%)

As of December, 31 2020.

Past performance is not a reliable indicator of future performance.

Source: Financial data and analytics provider, FactSet. Copyright 2020 FactSet. All Rights Reserved.

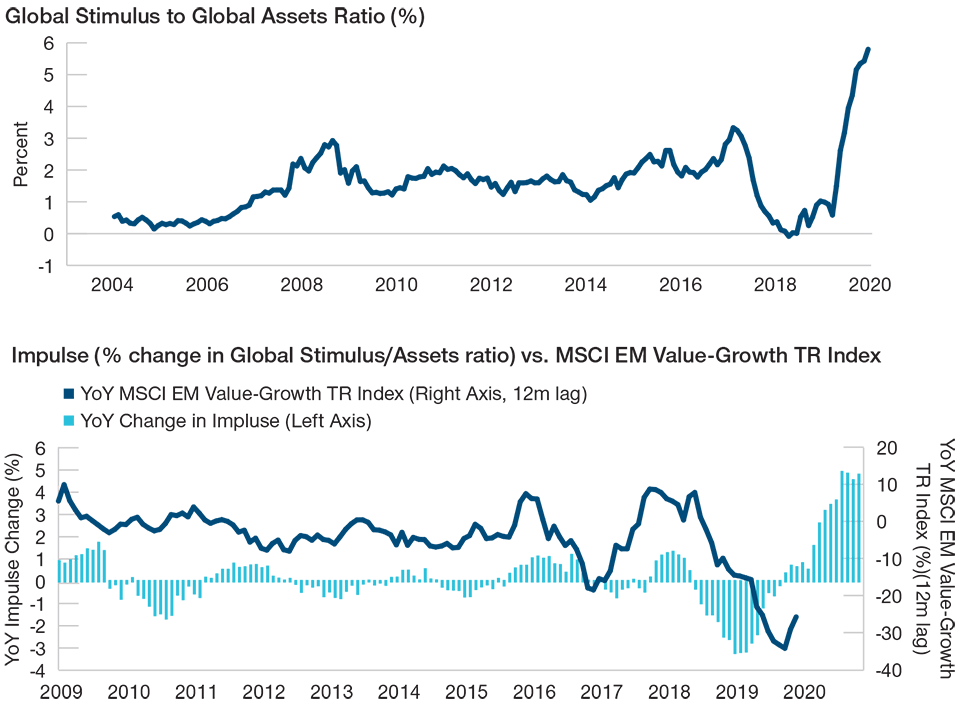

While the initial impact of the coronavirus crisis has been to push the divergence of value and growth stocks to all‑time highs, the latter part of the year was dominated by the “COVID‑on/COVID‑off” trade. This has been a one-factor trade, and in our view, it presents the single biggest market disconnection we are currently experiencing. Stocks that were perceived to be “COVID‑off” were indiscriminately sold off as investors chased “COVID‑on” beneficiaries. However, traditional growth stocks, such as cosmetics, gaming, and airport operators, have been sold off regardless of fundamentals. We expect the unprecedented global policy stimulus introduced this year will continue to have a beneficial impact on economies in 2021, as much of the income transfers have not been spent but remain sitting in people’s bank accounts. As effective vaccines become more widely available, business and consumers should become more confident, allowing social and economic behavior to normalize globally (Figure 2). At that point, a broader economic recovery should lead to an unwinding of many of last year’s “COVID” trades also supporting a market rotation away from growth in favor of value. Cyclical/old economy stocks in 2020 have become more forgotten and unloved than ever before. Looking at this opportunity set, we see no fundamental justification for value stocks to be quite so unloved, since many of them exhibit strong balance sheets and high cash flow generation while the economic impact of the coronavirus shock should fade as vaccines become available.

Our “Discovery” Thesis for Investing in EM Stocks

We believe that an active manager who seeks to identify such companies via a disciplined, bottom-up approach is more likely to succeed than a passive, indexed approach to EM value stocks. Instead of focusing on a particular index and quantitative screens, we prefer to invest bottom up, looking closely at what we believe drives the share price of every stock in the portfolio. Because we believe that buying cheap and waiting for mean reversion does not work well for EM, our starting point is not valuation. Our core investment thesis is that there are many good value opportunities at the stock level in emerging markets that tend to get “forgotten” or overlooked by mainstream EM equity funds.

Massive Global Stimulus May Trigger a Value Rotation

(Fig. 2) EM value-growth responds to stimulus with a lag

As of November 30, 2020.

Past performance is not a reliable indicator of future performance.

Sources: Bloomberg Finance L.P., Bank of International Settlements/Haver Analytics.

Please see Additional Disclosure page for information about this MSCI information.

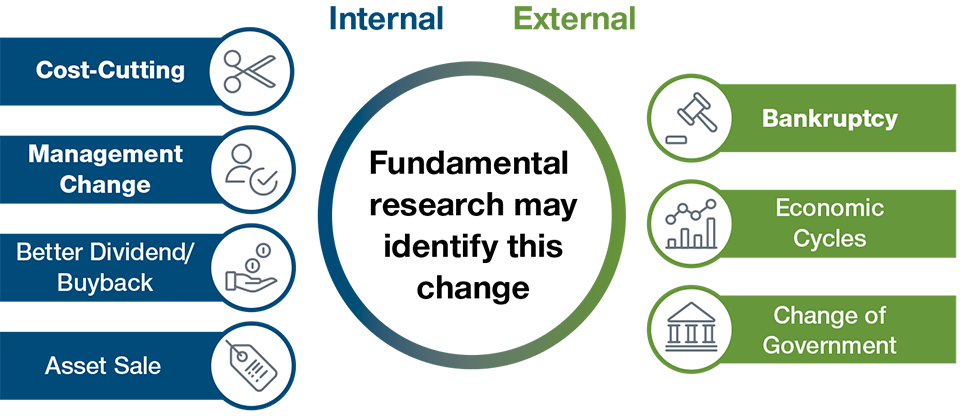

We tend to agree that the bottom 25% of EM stocks by quality are often “value traps” that are justifiably ignored by foreign investors. But among the next two quartiles—stocks that can be thought of as being of average EM quality—there will always be some that are about to move into the top 25% in terms of quality, rerating over time in the process (as well as others that are headed lower). We like to search for EM businesses in the mid quartiles that are successfully addressing the reasons for past underperformance and where management are confident that future performance can improve (Figure 3). Often, such stocks can be characterized as having been “forgotten” or neglected by the majority of EM portfolio managers. We look for signs of fundamental improvement that can help an EM stock to move up from being average quality to being good quality.

EM Value Stocks May Not Need Strong Topline Growth

(Fig. 3) Potential drivers for a value stock rerating

As of December 31, 2020.

Source: T. Rowe Price.

We do not invest on the basis of a one‑off, short‑term time catalyst. Rather, we look to invest in change that we expect will lead over time to fundamental improvement. The change can be company specific (e.g., cost-cutting, change in management, divestment), or it can be external (industry consolidation, government change that leads to a better run economy). We believe that such forgotten stocks can experience strong share price appreciation. We also look for a buffer, such as a strong balance sheet, that can provide a measure of downside support, potentially acting as an “anchor” to stocks that are already “cheap,” which in turn implies a potentially favorable asymmetric risk profile.

In Adversity Lies Opportunity

As investors have been chasing COVID beneficiaries, they have not been taking into account the solid fundamentals of old economy stocks, providing us with a fertile hunting ground. A deep dive into EM corporate balance sheets reveals that these remain intact in most cyclical industries—where banks, energy, and materials industries typically have low recapitalization risk and are fundamentally strong. Solid bottom‑up fundamentals coupled with the structural change in the way governments have been stimulating during the coronavirus crisis, in our view, provide the ingredients for a style regime change in the near term, and possibly the longer term. For the first time since the strategy’s inception, we see fundamental change to support a style‑based rotation.

In the past, we witnessed developed market governments and central banks pumping a lot of money into banks and corporates to recapitalize weak corporates’ balance sheets. Such was the case of Japan in the ‘90s and western economies after Lehman Brothers collapsed. This type of stimulus failed to have a multiplier effect in these economies. Now, post‑COVID, we believe something has changed—governments have realized that low interest rates alone are not enough to kick‑start economies. This time around, very little money is going into struggling corporates. Globally, other than a few airlines, governments have hardly stepped in for industrywide bailouts, instead targeting the consumer (helicopter money), and we believe this should likely result in a visible multiplier effect that could in turn benefit beaten‑down sectors and stocks. This offers the external fundamental change that we seek to invest in.

Outlook

We are of the view that the current extreme growth/value divergence will prove unsustainable. At some point, the unprecedented monetary and fiscal stimulus deployed by governments to deal with the coronavirus crisis is likely to result in a global reflation trade that can be expected to trigger a potentially sustained rebound in value stocks. Since strategy inception up to the onset of the coronavirus crisis, our portfolio has been tilted toward the “core” region of value. The extreme shifts in markets in 2020 have prompted us to favor a deeper value exposure. We are of the view that the conditions are currently being created to power a strong tailwind in 2021 for EM value investors.

Emerging markets have had a difficult time as an unpopular asset class, especially in the first quarter of last year when the pandemic started to accelerate across the world. The global emerging markets asset class experienced 35 consecutive weeks of outflows. But we are of the view that emerging markets are also likely to recover earlier than developed markets, as many of these countries did not implement extended lockdowns and as a result are already experiencing V‑shaped production recovery. In most of the emerging markets, governments do not actually have the capacity to lock down, because there is a large informal economy and people are without savings. Weaker fiscal balances make it equally hard for governments to lock down entire economies, as western-style consumer relief efforts are unaffordable. As a result, the deterioration of fiscal positions ended up being a cyclical phenomena. We see improved gross domestic product and fiscal accounts and are hopeful of a road to recovery from here on out.

What we’re watching next

We remain constructive toward EM equities and are looking for confirmation that a peak in performance divergence between value-oriented and growth stocks has been reached. We expect a cyclical recovery in EM, supported by measured stimulus, strong household savings, pent up consumer demand, and the return of corporate capital expenditure. The balance sheets of many cyclical industries like banks, energy, and materials appear to be fundamentally strong with low recapitalization risk.

Key Risks—The following risks are materially relevant to the strategy highlighted in this material:

Transactions in securities denominated in foreign currencies are subject to fluctuations in exchange rates which may affect the value of an investment. Returns can be more volatile than other, more developed, markets due to changes in market, political and economic conditions. The portfolio has increased risk due to it’s ability to employ both growth and value approaches in pursuit of long-term capital appreciation.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

January 2021 / INVESTMENT INSIGHTS