September 2023 / INVESTMENT INSIGHTS

Why You Should Consider a Better Future for EM Equities

Turnaround factors are forming to support emerging markets

Key Insights

- A strong dollar, disappointing earnings growth, and slowing global growth make the outlook for emerging market equities challenging in the short term.

- Those same headwinds, however, are likely to become tailwinds as we move through the next stages of the economic and equity cycle.

- Emerging market equities have historically been an early beneficiary of global economic recoveries. Any improvement in economic conditions may represent a signal to increase allocations to the asset class.

The global economic environment is highly complex as economic indicators are flashing red, liquidity is being drained from the financial system, and equity market returns have become concentrated in specific areas. Emerging markets (EMs) have also had to deal with distinct headwinds that have hindered performance. To add to this, the yield curve has been inverted for over a year now, raising the prospects of a US recession. (An inverted yield curve has preceded every US recession for the last 50 years.)

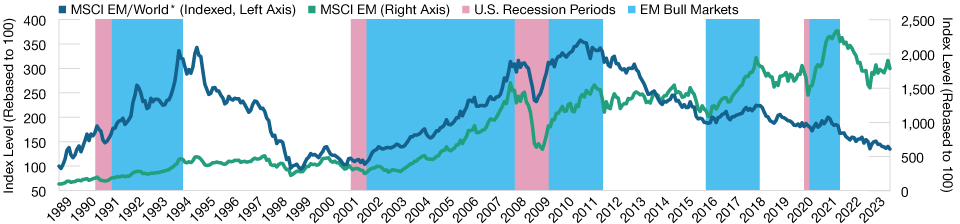

Emerging Markets Equities Have Typically Been Early Beneficiaries of Economic Recoveries

(Fig. 1) EM equities have historically outperformed coming out of U.S. recessions

As of August 31, 2023.

Past performance is not a reliable indicator of future performance.

*Blue line represents MSCI Emerging Markets Index performance versus the MSCI All Country World Index.

Sources: National Bureau of Economic Research, FactSet. Financial data and analytics provider FactSet. Copyright 2023 FactSet. All Rights Reserved.

At first glance then, it may not seem like the ideal time to be considering allocations to EMs, particularly given their reliance on global trade and exports. However, we believe specific turnaround factors are beginning to form. In addition, if we witness a short or mild recession that many economists are predicting, then EMs may be well placed to deliver as they have historically been early beneficiaries of economic recoveries (Figure 1).

Headwinds Likely to Turn to Tailwinds

There is no argument that EMs have performed poorly versus developed markets in recent years. A strong US dollar, geopolitical tensions, disappointing earnings growth, and a narrowing of the economic growth premium versus developed markets weighed heavily on sentiment. More recently, deglobalization trends—with greater protectionism and onshoring of production—have also worked to limit growth. However, looking further out, those same headwinds could become potential tailwinds as we move through the next stages of the economic and equity cycle. With compressed valuations, a weakening US dollar, peaking inflation in many emerging market countries, and the potential for interest rate cuts, the ingredients for early stages of recovery are forming.

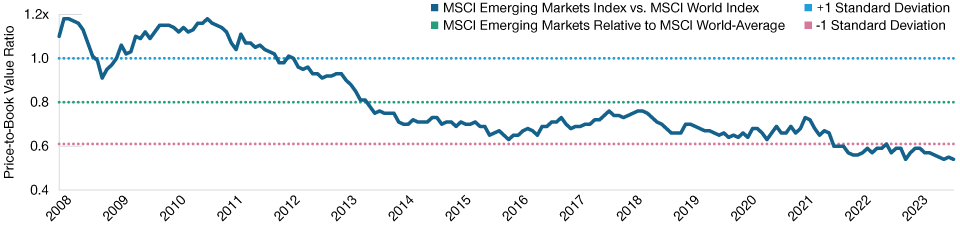

Valuations are particularly attractive relative to other markets. In terms of price‑to‑book, EM valuations have fallen to 1 standard deviation below historic levels (Figure 2), offering both opportunity (in terms of recovery) and further downside mitigation (as we head into a possible recession). Meanwhile, EM earnings estimates have already been marked down sharply, but we expect these to rebound as the global economy bottoms and then recovers.

Valuations Are Looking Attractive Versus Other Markets

(Fig. 2) Price‑to‑book valuations are close to historic lows

January 1, 2008 through August 31, 2023.

Source: FactSet. Financial data and analytics provider FactSet. Copyright 2023 FactSet. All Rights Reserved.

The Outlook Shows Promise, but Expect Bumps Along the Way

The path toward recovery is unlikely to be smooth, however, and the experience across EM countries will vary. Economies such as China, India, and Brazil, with strong domestic demand potential, are better placed to weather the challenging environment. China remains a conundrum, and even though the reopening of China following the extended COVID restrictions initially spurred investment, more recent data have been disappointing. Similarly, the underperformance of Chinese equities relative to their global counterparts year‑to‑date also reflects disappointing momentum.

There are positive signs for China, however. We believe the recovery hasn’t stalled but has started to move in a new direction where consumption, rather than investment, will drive growth. A key factor will be whether any further signs of slowdown prompt Chinese policymakers to stimulate the economy more aggressively to boost sentiment and consumption—a move likely to be welcomed by investors.

Outside China, Latin America is once again looking interesting. In Brazil, where interest rates are close to 14%, the market appears spring‑loaded to respond to any turn in the rate cycle after a long period of interest rate hikes. Mexico has been benefiting from increased investment as companies increasingly relocate their production. As of the most recent quarter‑end, we had our largest overweight here compared with the index as we can find strong idiosyncratic stock stories where we believe these companies can compound earnings growth over the next few years.

More fundamentally, the last 10 years for commodity‑producing EM nations like Brazil, South Africa, Chile, and Indonesia have been difficult. But, if we believe that commodity inflation is back, as many do, then their fiscal and current accounts are likely to improve markedly. Whether we are in the initial stages of another supercycle in commodity prices is up for debate, but there are similarities between the early 2020s and the early 2000s, the last time commodities began a long and powerful run. Now, as then, there has been significant underinvestment in commodity supply with capital expenditure in oil and gas and global mining sectors. In the early 2000s, China was the major source of accelerating commodity demand. Today, the switch to clean energy sources and electric vehicles is likely to prompt a more general acceleration in demand for key raw materials. We are overweight both materials and energy versus the index as of most recent quarter‑end.

We also believe the inflationary environment can be the catalyst to drive increased spending and awaken entrepreneurial spirits (at both a company and a government level). Since the global financial crisis in 2008, we have seen large‑scale underinvestment from both corporations and governments. Both policymakers and companies have focused on repairing balance sheets. Many industries have invested only at “maintenance capex levels,” rather than investing to improve productivity or expansion. We believe many industries are now long overdue investment, after many years of neglect.

Be Prepared As Conditions Improve

Although EM equities have been disappointing for investors over the last few years, we believe the risk/reward is starting to turn positive. Along with well‑known secular drivers, EMs are once again demonstrating a range of growth characteristics not easily available in developed markets (outside some of the best technology companies). We are increasingly finding what we believe are high‑quality companies that can generate sustainable earnings growth at a much higher rate than the global average. Banks are a notable example, with the return on equity for EM banks having been far higher than their developed market counterparts. Meanwhile, China’s leadership in electronic vehicles and solar panels, and the rise of the Chinese consumer will also offer multiyear possibilities.

In the near term, the imminent prospects for weaker growth, or recession, will likely trigger a flight to safety and set a challenging backdrop for EMs. However, if we see a shorter and milder slowdown and those headwinds start to dissipate and then reverse, we believe EMs are well placed to benefit, as they have typically done so in early phases of recovery. While investors should be wary of volatility in the short term, signs of recovery in the global economy will represent a signal to take a fresh look at allocations.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

September 2023 / MARKETS & ECONOMY

September 2023 / MARKETS & ECONOMY

Ernest Yeung is a portfolio manager for the Emerging Markets Discovery Equity Strategy at T. Rowe Price.