June 2021 / INVESTMENT INSIGHTS

Opportunistic Investing in a Dynamic High Yield Market

Investment flexibility may enhance risk-adjusted returns

Key insights

- Policy responses to the coronavirus pandemic should continue to create a conducive backdrop for leveraged credit in the near to medium term.

- Bank loans offer some degree of insulation from interest rate risk while providing attractive income in a low-yield fixed income opportunity set.

- Selectively participating in special credit situations, when value and a competitive advantage exist, is an important part of our approach.

With the economy continuing to recover from the global pandemic, we believe investors could benefit from an allocation to below investment-grade credit. Equity valuations appear somewhat stretched after a rally that began more than a year ago, meaning that returns could be more subdued going forward. In our view, the high yield market, including bank loans and distressed credit situations, remains an attractive option for investors seeking meaningful income in a relatively low-yield environment.

Policy responses to the pandemic should continue to create a conducive backdrop for below investment-grade, or leveraged, credit in the near to medium term. Unprecedented fiscal stimulus has provided meaningful support for the economic recovery, while the Federal Reserve and other major central banks have committed to accommodative monetary policy with a focus on real economic growth and improvements in the labor market.

We believe significant progress in vaccine distribution—roughly 50% of the U.S. population had received at least an initial dose of a vaccine by the end of May—could have powerful effects on consumer sentiment and behavior. At the corporate level, declining distress and improving fundamentals should result in a lower default rate in 2021 and 2022.

Ability to Invest Across the Capital Structure

We believe our investment approach is somewhat unique in that we can dynamically shift exposures based not only on our views of value across capital structures and industries but within companies’ capital structures as well. Our holdings reflect high-conviction names gleaned from our combined global high yield and bank loan credit research team, which allows us to identify inefficiencies and pursue relative value across both asset classes.

Specifically, we evaluate the full capital structure of a company, allowing for investment in positions outside of traditional high yield bonds, including bank loans and, to a lesser extent, equity or equity-related securities often tied to an existing credit position. However, we are willing to maintain a larger allocation to “core” high yield when risks appear skewed in favor of a more balanced approach.

Flexibility to Pursue Relative Value

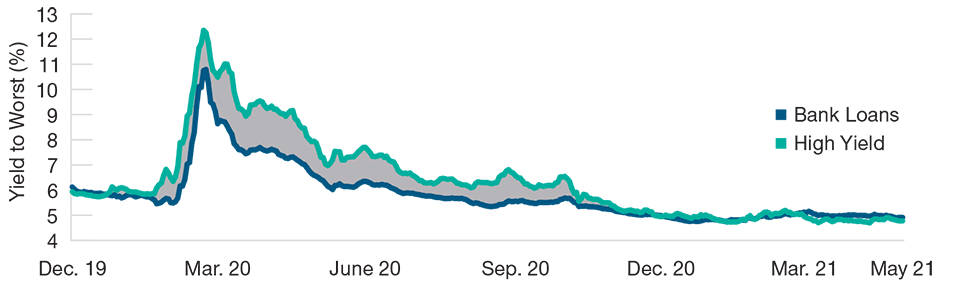

(Fig. 1) High yield bond and bank loan yields

As of 31 May 2021.

Past performance is not a reliable indicator of future performance.

Source: J.P. Morgan Chase & Co.

High yield represented by the J.P. Morgan Global High Yield Index; bank loans represented by the J.P. Morgan Leveraged Loan Index

Bank Loans Offer Low-Duration Profile and Attractive Yields

The post-pandemic macro environment has led to higher intermediate- and long-term Treasury yields as investors contemplate whether a broad economic recovery could trigger inflation, bringing greater attention to interest rate risk, often measured by duration.1 Our ability to flexibly allocate to bank loans should offer some degree of insulation from interest rate risk while providing attractive income in a low-yield fixed income opportunity set.

The floating rate feature of loans—where coupons adjust based on a short-term benchmark rate—gives them a very low duration profile, which means that they should perform well relative to other fixed income asset classes as rates increase. Given their shorter duration profile and seniority in the capital structure, we believe the loan asset class is a more defensive way to add exposure to below investment-grade names while also providing attractive income.

If the Federal Reserve remains on hold for the next year or two, we believe loan investors will be fairly compensated with solid income relative to other fixed income alternatives. On the other hand, if inflation picks up and the Fed is compelled to normalize rates earlier than anticipated, bank loan coupons will reset higher. The potential resiliency of loan income in differing rate scenarios contributes to the attractive value of the asset class.

Special Situations Could Provide Competitive Advantage

The breadth and depth of our global credit research platform allows us to selectively participate in special situations and distressed names when we identify the potential for value and a competitive advantage in negotiating favorable outcomes. When participating in a restructuring process, for example, we seek to maintain our position in liquid, freely tradeable securities and take an active role on creditor committees to create value for the positions.

Compelling Yield/Duration Profile

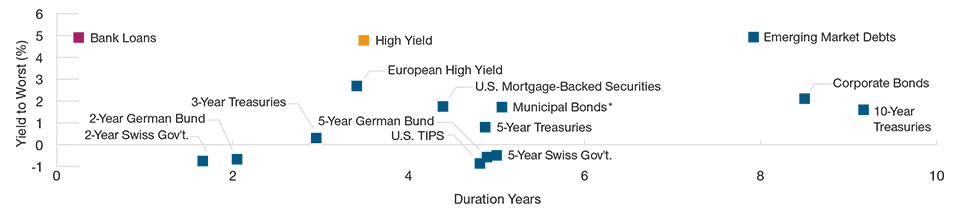

(Fig. 2) Duration and yield across asset classes

As of 31 May 2021.

Past performance cannot guarantee future results.

*Taxable-equivalent yield assuming a 40.8% tax rate.

Sources: J.P. Morgan Chase & Co., Bloomberg Index Services Ltd., Bloomberg Finance, L.P., and ICE BofAML (see Additional Disclosures). Bloomberg Barclays Indices: Corporate Bonds: U.S. Corporate Investment Grade Index; Municipal Bonds: Municipal Bond Index; U.S. Mortgage-Backed Securities: MBS Index; U.S. TIPS: U.S. Treasury: U.S. TIPS; 2-Year Swiss Gov’t.: Swiss Aggregate: Treasury 1–3 Years; 5-Year Swiss Gov’t.: Swiss Aggregate: Treasury 3–7 Years; J.P. Morgan Chase & Co. Indices: High Yield: Global High Yield Index; Bank Loans: Leveraged Loan Index; Emerging Markets Debt: EMBI Global Diversified Index; 2-Year German Bund: 2-Year German Bund benchmark; 5-Year German Bund: 5-Year German Bund benchmark. From Bloomberg Finance, L.P.: 3-Year Treasuries represented by the U.S. 3-Year Treasury Note in the U.S. Treasury Actives Curve; 5-Year Treasuries represented by the U.S. 5-Year Treasury Note in the U.S. Treasury Actives Curve; 10-Year Treasuries represented by the U.S. 10-Year Treasury Bond in the U.S. Treasury Actives Curve; European High Yield represented by the ICE BofAML European Currency High Yield Constrained Excluding Subordinated Financials Index Hedged to USD.

These holdings, while limited in number, can offer the potential for meaningful total return. They can also afford exposure to areas of the credit market that may not be closely followed by traditional buy-side investors and, therefore, could be mispriced.

Reorganization Plan Supports Holdings Related to Bankrupt Satellite Operator

For example, our investment in a bankrupt satellite operator is a special situation that produced meaningful absolute returns during the first quarter of 2021. Our investment team has closely followed developments in this credit story for several years, and when the company filed for bankruptcy in May 2020, we saw a favorable risk/reward opportunity in the secured part of the capital structure—we only own the company’s secured bonds and loans—based on our fundamental view that the value of the core business is sufficient to cover the company’s secured debt.

The various parts of the company’s capital structure rallied after the firm reached an agreement with some of its creditors and filed a financial reorganization plan that could significantly reduce debt and pay down secured bonds and loans upon exit from bankruptcy. This positions the company to potentially emerge from bankruptcy in the second half of 2021, although this could be extended due to the complex nature of the case. The longer the company stays in bankruptcy, the longer our position likely benefits.

Key Risks—The following risks are materially relevant to the strategy highlighted in this material:

Debt securities could suffer an adverse change in financial condition due to a ratings downgrade or default, which may affect the value of an investment. Fixed income securities are subject to credit risk, liquidity risk, call risk, and interest rate risk. As interest rates rise, bond prices generally fall. Investments in bank loans may at times become difficult to value and highly illiquid; they are subject to credit risk such as nonpayment of principal or interest, and risks of bankruptcy and insolvency.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.