April 2021 / INVESTMENT INSIGHTS

High Yield Debt Can Boost Income And Return Potential Amid Low Yields

Downside risk management is crucial

Key Insights

- Volatility and low yields are likely to persist over the next few years as the global economy recovers from the shock of the coronavirus.

- High yield bonds, which historically have tended to outperform equities in the years immediately following a recession, may be an attractive option for investors looking for yield in the post‑coronavirus economic environment.

- Some of the best opportunities within high yield over the next few years are likely to be in defensive areas such as cable and retail.

Volatility and low yields are likely to persist over the next few years as the global economy recovers from the shock of the coronavirus. Navigating this environment will be difficult, particularly as returns from equities are likely to be lower after the strong rally of the past year. High yield bonds, which historically have tended to outperform equities in the years immediately following a recession, may be an attractive option for investors looking for yield in the post‑coronavirus economic environment.

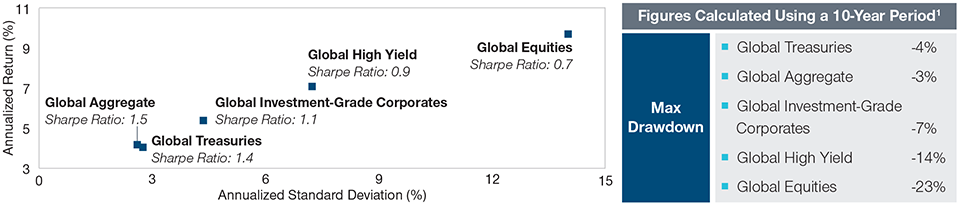

High yield debt is often overlooked by some investors as it is regarded as too volatile. This is something of a false perception, however. Over the past 10 years, both the annualized standard deviation and the maximum drawdown of the ICE Bank of America Global High Yield Index has been around half that of the MSCI All Country World Index (Figure 1).

High Yield Offered Significant Return per Unit of Risk

(Fig. 1) Its annualized returns were close to that of equities

As of December 31, 2020.

Past performance is not a reliable indicator of future performance.

Performance covers from December 31, 2010 to December 31, 2020.

1 Data is based on the 10 years ending December 31, 2020.

Sources: ICE, Bloomberg Barclays, and MSCI (see Additional Disclosures). Global Equities represented by the MSCI ACWI (net); Global Aggregate represented by the Bloomberg Barclays Global Aggregate Index; Global Investment‑Grade Corporates represented by the ICE Bank of America Global Corporate Index; Global High Yield represented by the ICE Bank of America Global High Yield Index; Global Treasuries represented by the Bloomberg Barclays Global Aggregate Treasuries Index. All returns are hedged to U.S. dollar.

Crucially, this reduced risk does not come at the expense of a major loss of return. Over the past 10 years, global high yield delivered an annualized return of around 7% compared with around 9% for global equities. So overall, global high yield has carried around half the risk of global equities over the past decade while it may potentially offer a stronger risk/return trade-off (Figure 2).

High Yield Bonds May Potentially Offer a Strong Risk-Adjusted Return

(Fig. 2) Our 5-year forecast for global high yield and global equities

As of January 2021.

Sources: T. Rowe Price, MSCI, Bloomberg Barclays, S&P, J.P. Morgan Chase & Co., HFR, Cambridge Associates, NCREIF, and FTSE/Russell (see Additional Disclosures). Global Equity represented by the MSCI ACWI; Global High Yield represented by the Bloomberg Barclays Corporate High Yield. This information is not intended to be investment advice or a recommendation to take any particular investment action. The forecasts contained herein are for illustrative purposes only and are not indicative of future results. Forecasts are based on subjective estimates about market environments that may never occur. The asset classes referenced are represented by broad-based indices, which have been selected because they are well known and are easily recognizable by investors. Indices have limitations due to materially different characteristics from an actual investment portfolio in terms of security holdings, sector weightings, volatility, and asset allocation. Therefore, returns and volatility of a portfolio may differ from those of the index. There is no guarantee that any forecasts made will come to pass. Actual results may vary.

Volatility Is Set to Remain Elevated

In a low‑yield world, investors need to cast a wider net for income. High yield bonds have a strong track record in delivering good income during periods when it is unavailable elsewhere. As high yield sits above equity in the seniority of any capital structure and typically has multiple securities to invest in, it may allow investors to take more selective credit risk while knowing that they are still likely to receive a decent level of income.

These features of high yield debt are likely to be very useful during the period ahead if volatility remains elevated—and we believe there is every reason to think that it will. Government and investment‑grade bond yields are low—and in some cases negative—while the rally in stocks that began last March has left prices stretched, potentially meaning lower returns over the next few years. At the same time, the prospect of many countries exiting lockdowns and kick‑starting their economies at the same time has led to growing concerns over inflation. This combination of low yields and potentially rising inflation means that continued volatility is highly likely.

We believe the next few years will be characterized by a battle between the underlying economic fundamentals that drive companies and their opportunities versus technical market factors, such as concerns over inflation. While technical factors will inevitably have an impact on prices in the near term, we believe it is better to focus on companies with strong fundamentals that look well placed to benefit from the more stable economic environment expected over the next few years. Investors who are able and willing to look beyond near‑term volatility and focus on longer‑term fundamentals should be more likely to capture strong medium‑term returns.

Lower‑Rated Firms Are Well Placed to Benefit From a Recovery

The search for yield has attracted a growing number of investors to high yield debt who have little or no previous experience of investing in the asset class. For such investors, it is essential to truly understand the risks they are taking on—and whether the pricing of those risks means they are likely to achieve a good return.

High yield investments are sub‑investment‑grade corporates and are at the weaker end of the ratings spectrum. Companies with lower ratings are likely to benefit more from the economic recovery than those with higher ratings, particularly if they have already survived 2020 and have balance sheets that are stable and sustainable to get them through the period ahead. If such firms are trading weakly at the moment, they may represent a good opportunity once the post‑coronavirus economic recovery is in full swing.

A number of sectors have suffered heavily during the coronavirus pandemic, particularly those—such as entertainment and transport—that are dependent on footfall. However, companies within those sectors that have strong balance sheets, have managed their debt well or even repaired it during the pandemic, and whose liquidity forecasts indicate that they are well placed to survive into 2022 may be among those who can perform very well during the post‑coronavirus economic recovery. Many of these types of firms are currently undervalued and, as such, represent good opportunities.

Fallen Angels Have Lowered Default Rates

Fallen angels—companies whose debt was formerly investment grade but which has been downgraded to high yield—have further enriched the high yield opportunity set. There was a record amount of fallen angel debt last year—almost USD 250 billion worth—in the global high yield market. The presence of so many fallen angels within the high yield space has improved the credit quality of the asset class: A decade ago, some 40% of the ICE BofA Global High Yield Index was BB‑ rated (the upper end of asset class’s rating scale); today, that figure is more like 60%.

As the average rating of high yield debt has increased, overall default risk has fallen. A year ago, we were expecting 2020 high yield default rates of around 10% in the U.S. and 4.5% in Europe; in reality, those figures were around 7.5% for the U.S. and less than 3.5% for Europe. This year, we’re expecting those rates to be halved. This indicates that a combination of balance sheet repair and the arrival of a large number of fallen angels should significantly reduce the risk of default among high yield issuers.

Moreover, the amount investors receive if a company defaults has also increased significantly and currently stands above 50%, according to J.P. Morgan Chase & Co.1 Take European high yield for example, if the default rate is 2% and the amount received from companies that have defaulted is 50%, the overall loss is 1%, or 100bps. Given that the spread of high yield debt returns over the risk‑free rate is currently around 390bps, the overall potential return is just under 300bps when default risk is factored in.

Default Rates Are Peaking as New Issuance Aids Liquidity

(Fig. 3) Fallen angels have also helped to improve credit quality

Fallen angels have also helped to improve credit quality")

As of December 31, 2020.

Past performance is not a reliable indicator of future performance.

1 Actual outcomes may differ materially from estimates.

Sources: Bank of America, J.P. Morgan Chase & Co. (see Additional Disclosures).

Defensive Areas Can Offer Some of the Best Opportunities

In our view, some of the best current high yield opportunities exist in defensive areas that can add ballast to portfolios. The cable industry, for example, would appear to have solid prospects as the shift toward working from home is likely to continue beyond the coronavirus pandemic, bringing greater demand for data transfer. While the leading names in the industry may no longer offer a great deal of value, they can potentially provide very strong income and a degree of stability.

Another area worth considering is food retail, and in particular supermarket chains. This sector offers similar potential stability to the cable industry and can offer some compelling opportunities when there are changes of ownership, as recently occurred when the UK supermarket group ASDA was bought out. Buyouts result in changes in the capital structure and potentially increased leverage, which means greater risk—and potentially some very good opportunities.

Riskier opportunities can be found in industries that are undergoing significant change. The automotive sector, for example, is in the process of a major secular shift toward electrification but at a pace that is not entirely within its control as attitudes toward the traditional internal combustion engine vary considerably around the world. There will inevitably be winners and losers within the industry. Firms with the intention and capacity to fully embrace electrification, particularly those large enough to offer a wide range of debt to invest in, are worth taking a closer look at.

Overall, then, although yields are lower than they have been in the past, we believe high yield investors are able to benefit from both the supportive fundamental environment and potential for lower volatility than other high‑returning asset classes. To make the most of the opportunities available, we think that investors should avoid trying to chase the market as a whole and be highly selective when choosing which high yield bonds to invest in. Finally, it is worth noting that because of its track record of delivering consistent returns, high yield debt works most effectively when included in a permanent asset allocation model in order to benefit from compounding interest over time.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

April 2021 / INVESTMENT INSIGHTS