Credit Investor’s Checklist

Spring 2026

Summary

- Investor concerns over potential risks from AI disruption, the credit cycle and war in the Middle East reinforce the importance of key principles for successful credit investing

- These principles include credit underwriting based on strong fundamentals, structuring expertise, downside protection, risk monitoring rigor and a long track record of success through cycles

- In an investment environment that may promote greater differentiation across credits and managers, these principles may help investors better evaluate credit managers and their potential to outperform

Focus on Strong Fundamentals

Credit Selection

OHA believes that borrowers with strong business fundamentals and reliable cash flows are better positioned to repay their debt across evolving market conditions. By focusing on these types of borrowers, credit managers may be better positioned to generate attractive risk-adjusted returns.

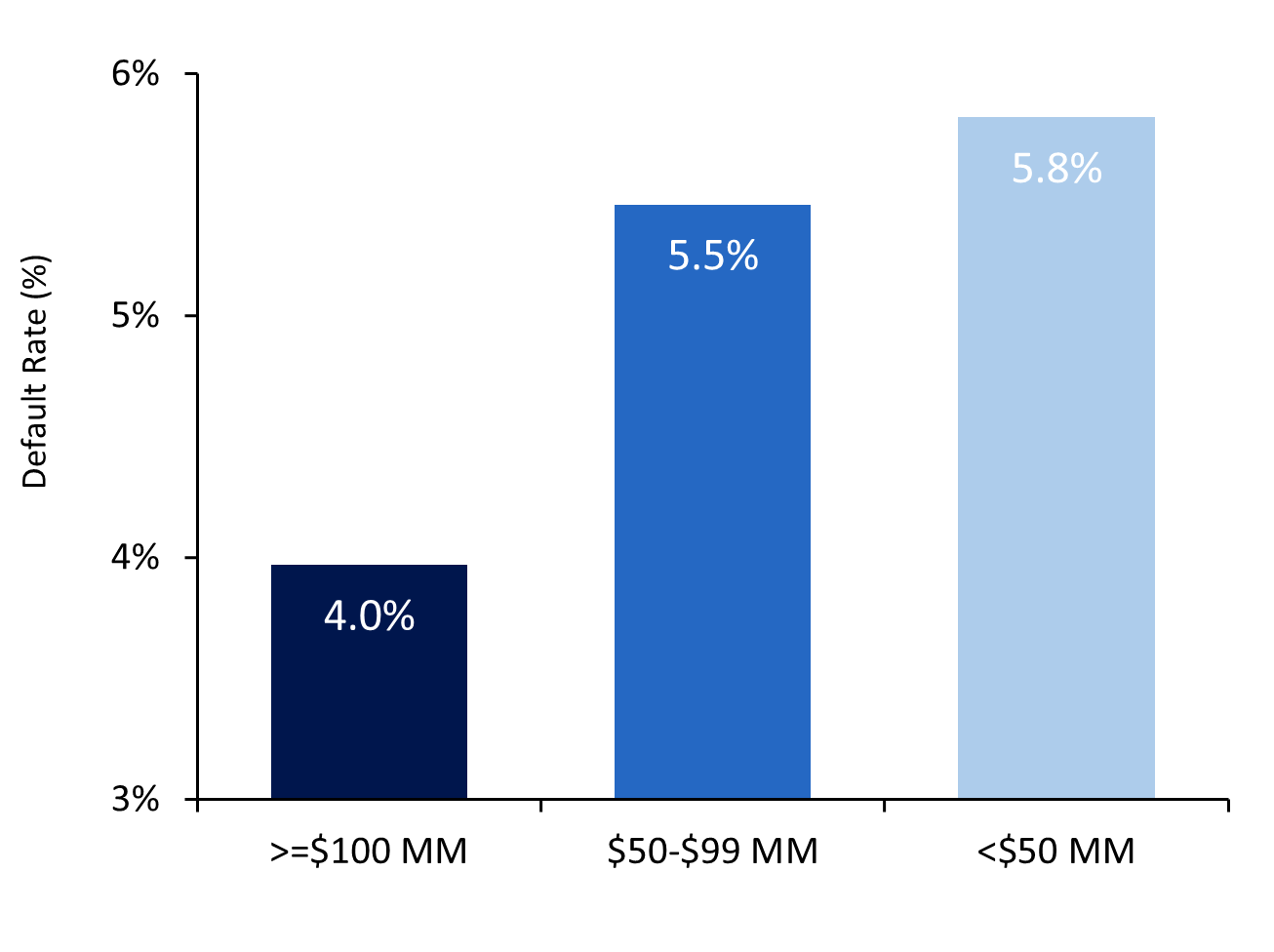

OHA believes that larger businesses are more likely to have strong fundamentals and be stronger borrowers, which may help mitigate downside risk. Larger businesses often have advantages that allow them to better weather market volatility and economic downturns — including greater scale, stronger pricing power, well-established management teams, more operational flexibility, and access to deeper financial resources. Together, these qualities can better position borrowers for successful financial outcomes.

Since 1995, larger companies have demonstrated greater resilience relative to smaller borrowers, exhibiting materially lower default rates across multiple credit cycles. Shown in Figure 1, borrowers with greater than or equal to $100 MM in EBITDA experienced a 32% lower default rate compared to smaller borrowers. We believe these long-term results suggest that larger companies have been better positioned to navigate market cycles than smaller companies.

Fig. 1: Loan Defaults by Borrower Size(1)(2)

As of December 31, 2025

Structuring Expertise

Seeking Lender Protections

OHA believes documentation and structuring expertise at the time of underwriting are key to protecting lenders against harmful borrower actions. These borrower actions have become known in the industry by the names of the well-known borrowers in which the tactic was deployed. These include past deals like J. Crew, Pluralsight, Chewy and Serta. Other tactics used by borrowers include loose definitions of EBITDA and leverage or debt caps which attempt to modify the value of collateral lenders have access to. Protections against these tactics have become increasingly important as defaults increase and are more commonly settled in out of court restructurings, also known as liability management exercises (“LMEs”), where borrowers may pit lenders against one another to maximize recovery.

Figure 2 highlights the three key protections OHA believes skilled lenders focus on to safeguard their position in an increasingly complex LME environment. When properly negotiated and structured, these protections can fortify credit agreements and help enhance downside protection for investors.

Fig. 2: Benefits of Lender Protections(3)

Downside Protection

Evaluating the Importance of Workout Capabilities

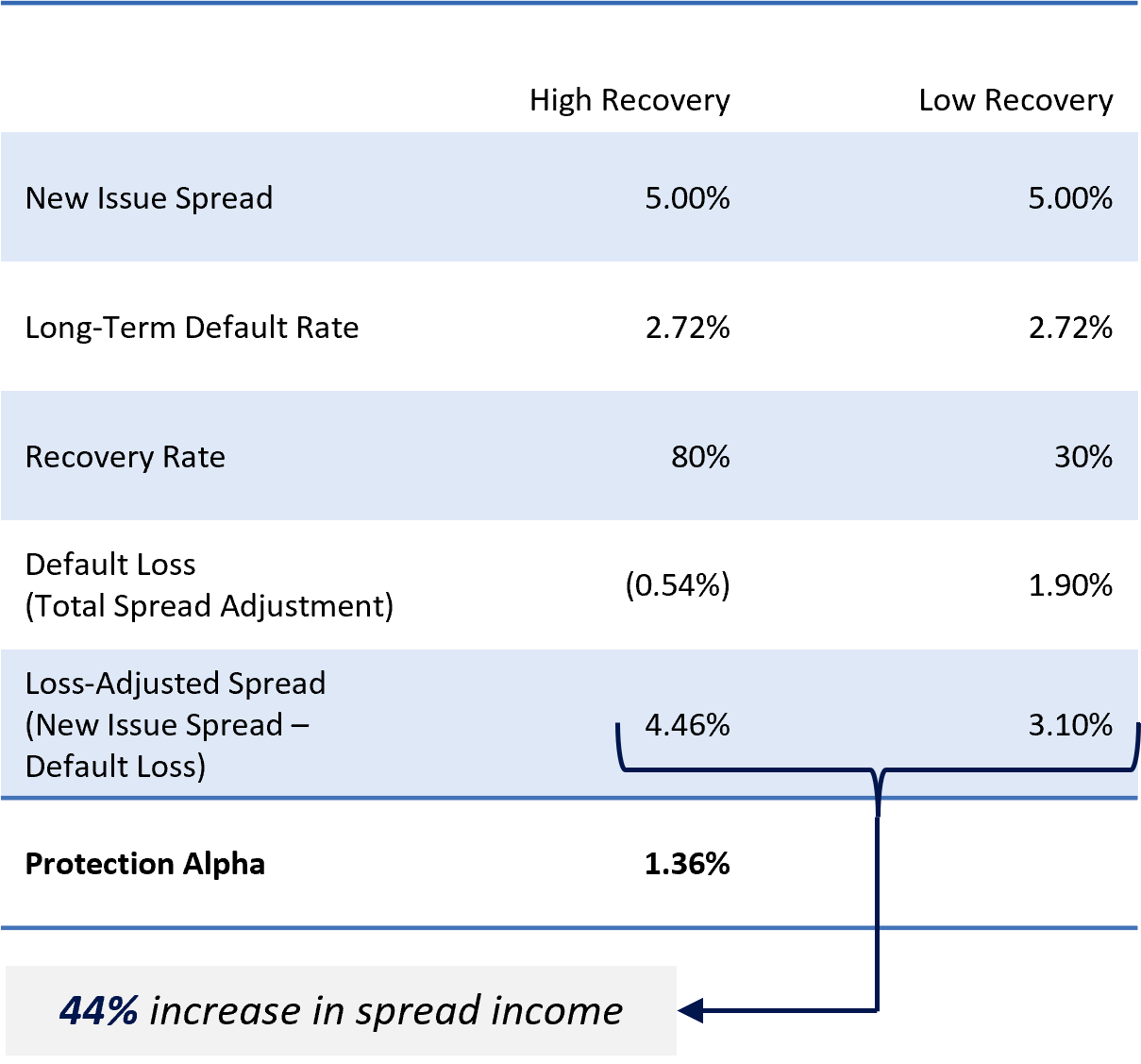

OHA believes that downside protection is a primary driver of long-term credit performance since returns are typically driven by contractual income versus capital appreciation. While nominal spreads are a key focus for investors, they do not account for potential credit losses over the investment’s full life. Figure 3 shows an illustrative analysis of portfolios with identical spreads and default rates, but differing recovery rates. After adjusting the spread for default losses, the higher recovery portfolio generates a 44% higher spread than the lower recovery portfolio. OHA believes this analysis illustrates how losses can materially erode realized returns, especially during periods of market stress when both default rates rise and recovery rates fall, leading to elevated losses.

Managers with extensive workout and restructuring expertise may be better positioned to optimize outcomes for their investors when defaults become unavoidable. This expertise, ideally honed over multiple credit cycles, may prove a key source of alpha. OHA refers to this incremental return as “protection alpha” to emphasize the importance of downside protection for credit investors.

As a result, OHA views loss avoidance, not spread maximization, as an area of differentiation among credit managers, consistent with its long-standing focus on downside protection across corporate credit strategies.

Fig. 3: Illustrative Loss-Adjusted Spread(4)

As of December 31, 2025

Risk Monitoring

Framework to Understand Credit Risks

OHA believes investors should look for managers with a strong risk monitoring framework to assess each portfolio company’s financial health as each borrower evolves over time. This includes assessing the potential impact of new and growing risks, such as the rise of artificial intelligence. Managers that re-underwrite their portfolio continuously and challenge prior assumptions may be able to identify risks earlier and analyze their direct and indirect impacts better than others.

Additionally, OHA believes deep industry expertise may help investors manage business, market and economic risks. OHA believes managers that focus on industries that are generally more recession resistant may find greater success. Investing in more defensive, less cyclical industries can help reduce volatility and support performance through economic downturns. These industries may include software, healthcare, utilities, business services, finance and insurance, as illustrated in Figure 4. These industries typically have more defensive characteristics such as durable demand due to the mission-critical nature of their product or service, creating high barriers to entry and stronger pricing power.

Together, OHA believes maintaining a well-defined risk management framework across both issuer and industry-level analysis is essential to mitigating downside risk, preserving capital and supporting more stable outcomes across market cycles.

Fig. 4: Recession-Resistant Industry Selection(5)

Length of Track Record

Time-Tested Approach to Credit Investing

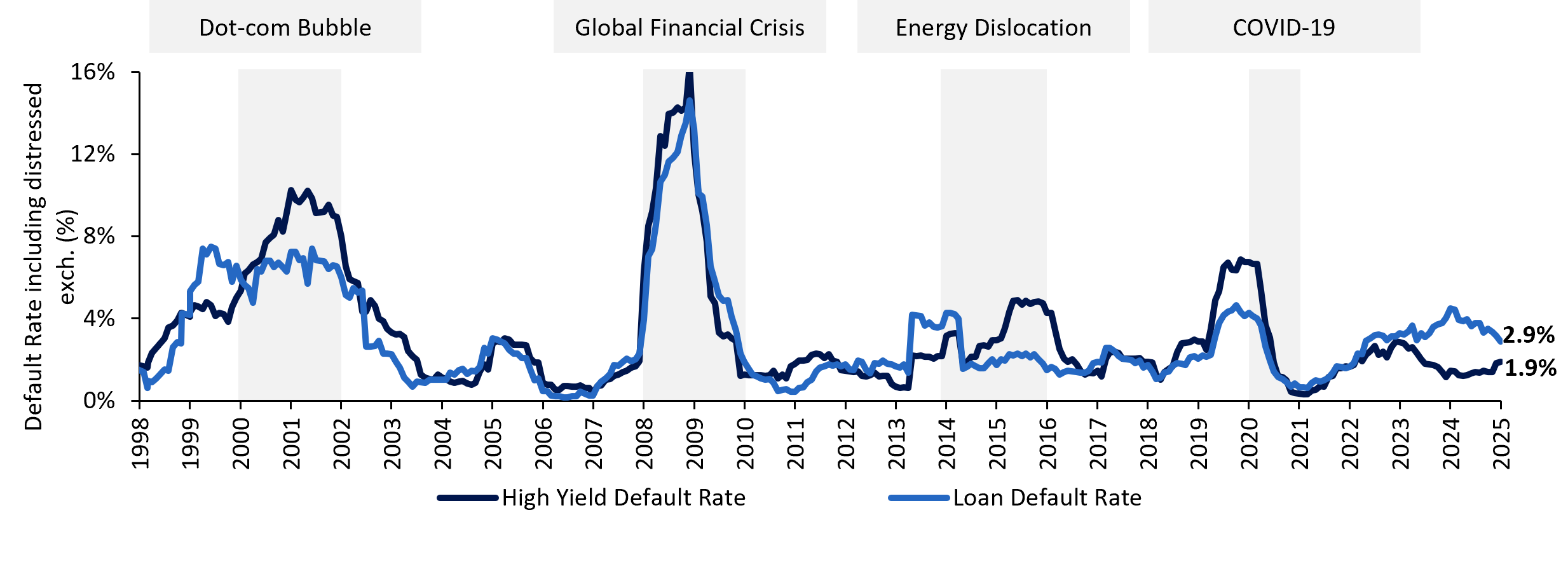

OHA believes consistent performance across multiple credit cycles is a key determinant of long-term success in credit investing. As illustrated in Figure 5, since 2000 there have been four periods of widespread market dislocation that materially affected default rates and recovery outcomes across the credit landscape. In our view, managers that have consistently maintained below-market default rates and superior recoveries through these periods have been better positioned to generate attractive, risk-adjusted returns over full market cycles. We believe that the consistency and length of track records reflect a deep, fundamental understanding of industries, companies and capital structures, developed through disciplined investing across evolving market environments. Identifying managers with historically proven, long-term track records should be viewed as a key consideration for end-investors evaluating opportunities across the credit spectrum.

Fig. 5: Historical default rates and market dislocations(6)

1998-2025

- January 2026

PIKing Your Spots in Private Credit

- December 2025

After Sell-off, Are Public BDCs More Attractive than Non-Traded BDCs?

Appendix and endnotes

1 Source: Pitchbook LCD as of December 31, 2025. Data shown is from LCD Default Review 4Q25. Comprises loans closed between 1Q 1995 and 4Q 2025. Default rates are calculated by dividing the number of defaulted loans by the aggregate number of loans in the Index. PitchBook defines default as when a borrower has missed a principal or interest payment and is not in a forbearance period, a borrower files for bankruptcy under Chapter 7 or Chapter 11 of the US Bankruptcy Code, a borrower has hired a restructuring advisor or has entered the restructuring process (applies only to European syndicated loans)or a loan has been downgraded to D by S&P Global Ratings (does not apply in cases of distressed exchanges).

2 EBITDA is defined as earnings before interest, taxes, depreciation and amortization. EBITDA is a common proxy for cash flow.

3 Source: OHA analysis as of February 2026.

4 Source: OHA analysis as of February 2026. Default rates represented by the average default rate from 1Q 2013 – 3Q 2025 of the Cliffwater Direct Lending Index.

5 Based on OHA analysis as of February 2026.

6 Source: J.P. Morgan U.S. High Yield and Leveraged Loan Default Update, December 2025. Represents par-weighted default rates including distressed exchanges. Past performance is no guarantee or a reliable indicator of future results.

Key risks and disclosures

All investments are subject to market risk, including the possible loss of principal. Some or all alternative investments may not be suitable for certain investors. No assurance can be given that a fund’s investment objectives will be achieved. Alternative investments are speculative and involve a substantial degree of risk. Opportunities for withdrawal/redemption and transferability of interests are generally restricted, so investors may not have access to capital when it is needed. Any investor who subscribes, or proposes to subscribe, for an investment in a fund or separately managed account must be able to bear the risks involved and must meet relevant suitability requirements.

Fixed-income securities are subject to credit risk, liquidity risk, call risk, and interest-rate risk. As interest rates rise, bond prices generally fall. Investments in high-yield bonds involve greater risk of price volatility, illiquidity, and default than higher-rated debt securities. International investments can be riskier than U.S. investments due to the adverse effects of currency exchange rates, differences in market structure and liquidity, as well as specific country, regional, and economic developments.

The use of a single advisor applying generally similar trading programs could mean lack of diversification and, consequently, higher risk. The use of leverage and other speculative practices may increase the risk of investment loss or make investment performance volatile. In addition, the fees and expenses charged may be higher than the fees and expenses of other investment alternatives, which will reduce profits.

Important Information

All opinions and estimates are based on assumptions, all of which are difficult to predict and many of which are beyond the control of OHA. In preparing this document, OHA has relied upon and assumed, without independent verification, the accuracy and completeness of all information. OHA believes that the information provided herein is reliable; however, it does not warrant its accuracy or completeness. All charts and tables are shown for illustrative purposes only.

This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action. The views contained herein are those of the authors as of February 2026 and are subject to change without notice; these views may differ from those of other OHA or T.Rowe Price associates. This information is not intended to reflect a current or past recommendation concerning investments, investment strategies, or account types, advice of any kind, or a solicitation of an offer to buy or sell any securities or investment services. The opinions and commentary provided do not take into account the investment objectives or financial situation of any particular investor or class of investor. Please consult your financial advisor and consider your own circumstances before making an investment decision.

T.Rowe Price Investment Services, Inc. OHA is a T. Rowe Price company. © 2026 Oak Hill Advisors. All Rights Reserved. OHA is a trademark of Oak Hill Advisors, L.P. All other trademarks shown are the property of their respective owners. Use does not imply endorsement, sponsorship, or affiliation of Oak Hill Advisors with any of the trademark owners.

202603-5333820