PIKing Your Spots in Private Credit

January 2026

Summary

- Payment-in-Kind (“PIK”) is a negotiated feature in private credit that allows borrowers to defer a portion or all of their cash interest, with the unpaid interest accruing to the principal balance

- PIK is generally priced at a premium relative to a cash-pay loan, as lenders seek to capture additional spread in exchange for the flexibility and foregone cash income

- OHA views PIK structured at origination as a strategic financing solution to support borrowers’ liquidity and growth goals

- OHA believes PIK created by amendment after origination can be an effective temporary tool in select circumstances, but may serve as a signal of credit stress

Eric Muller

Portfolio Manager & Partner, CEO – BDCs

Eric Muller

Portfolio Manager & Partner, CEO – BDCs

Payment-in-Kind Overview

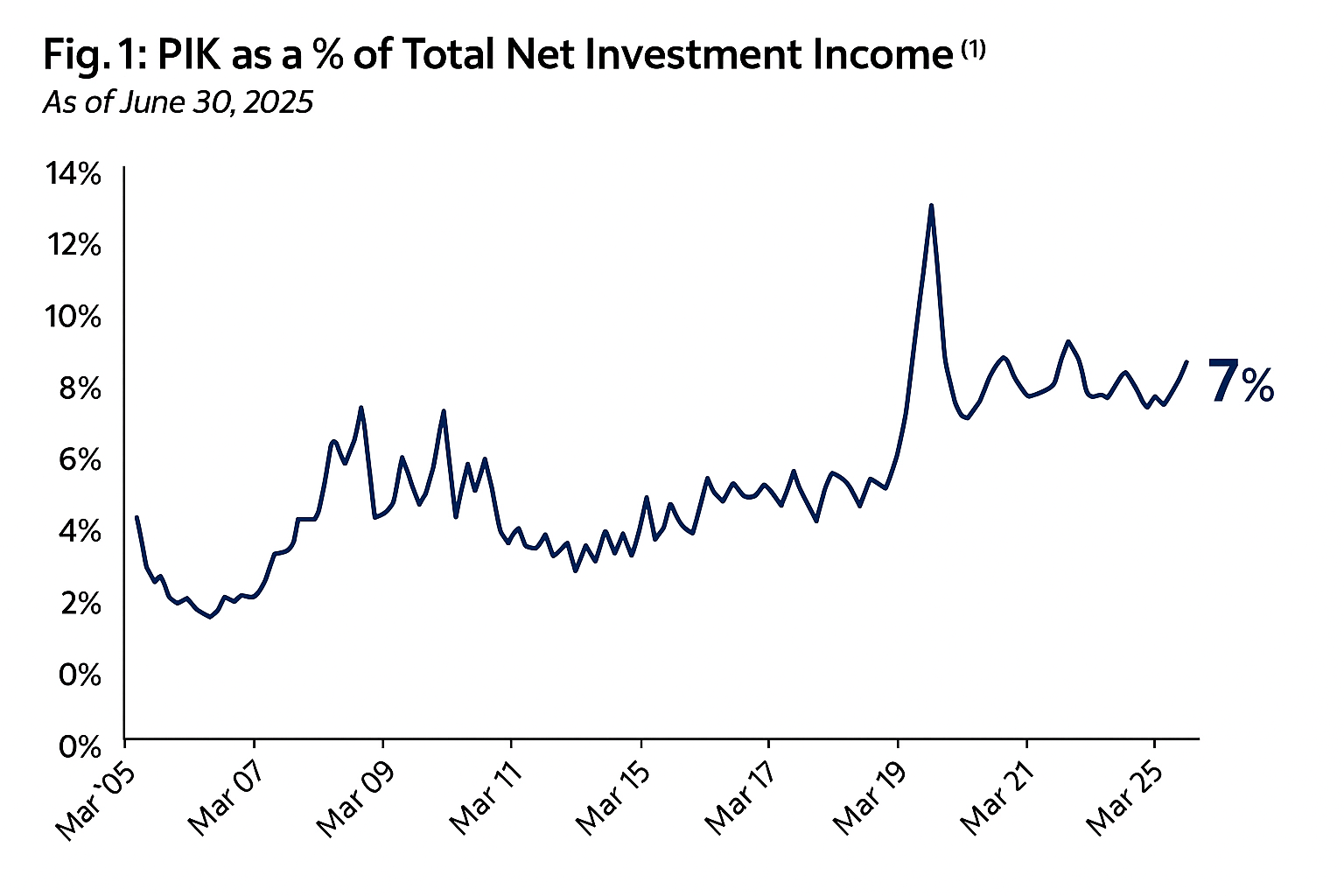

Payment-in-Kind, commonly referred to as PIK, allows borrowers to defer some or all of their cash interest payments by accruing them to the loan’s principal balance. At maturity, both the original principal and the accrued interest are repaid in full, typically with a higher spread compared to a traditional cash-pay loan. In recent years, private market borrowers have increasingly sought PIK financing to preserve liquidity and enhance flexibility following the rapid rise in base rates post-COVID-19.(2) Fig. 1 highlights this trend, with PIK now representing 7% of total net investment income.

OHA believes that a lender’s approach to PIK financing can significantly influence both risk and returns for end investors. In some cases, the use of PIK may be an early sign of underlying credit stress. However, when structured effectively, PIK can serve as a strategic tool for high-quality companies to preserve liquidity and invest in growth initiatives.

In this paper, we explore the scenarios where PIK may be utilized and the rationale as well as critical considerations for investors as PIK features become an area of increasing focus for private credit portfolios.

PIK Scenarios

PIK interest is most commonly utilized in one of two general scenarios: (I) at origination and (II) amendment after origination.

(I) PIK at origination is incorporated into the initial credit agreement and typically expires within the first two years of the loan’s life. This feature is most often offered to high-quality, high-growth companies to support further expansion initiatives such as M&A, synergy realization and organic growth.

In senior direct lending, PIK is commonly structured as partial PIK or PIK toggle, where lenders still receive most of the interest in cash. The cash-pay portion typically includes the base rate plus half of the loan’s spread component. For example, on a loan priced at SOFR + 500 basis points, the borrower might pay SOFR + 250 basis points in cash while PIKing the remainder of the spread.(3)(4) To compensate for added complexity, loans that are actively PIKing generally pay a 25 – 50 basis points premium to a comparable cash-pay loan.

While borrowers sometimes request PIK features, they still represent a modest portion of income in performing private credit. As shown in Fig. 1, in Q2 2025, just 7% of net investment income was PIK interest, underscoring the predominantly cash-pay nature of these portfolios.(1)

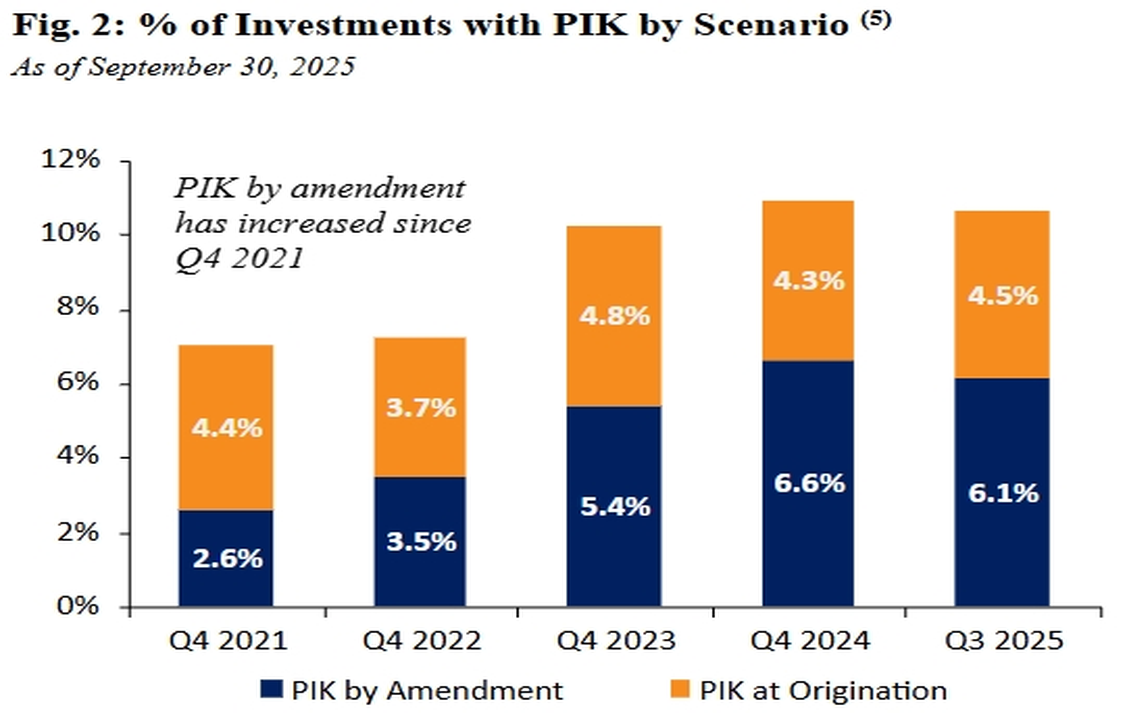

(II) PIK by amendment refers to a provision offered to existing borrowers who did not have a PIK option in their original loan documentation. It is sometimes extended to borrowers facing challenges in meeting their near-term cash interest obligations and seeking temporary relief to stabilize cash flows. Lenders entering these provisions may require additional collateral, such as incremental equity contribution in sponsor-backed deals, to seek additional downside protection.

PIK by amendment can be a highly effective tool for both borrowers and lenders in the right circumstances. A notable example occurred during the COVID-19 pandemic, when these provisions helped borrowers withstand widespread financial disruption. In such situations, the ability to PIK enabled companies to conserve cash and prioritize core operations while also offering lenders an attractive spread premium.

PIK by Type

Borrower Size Matters

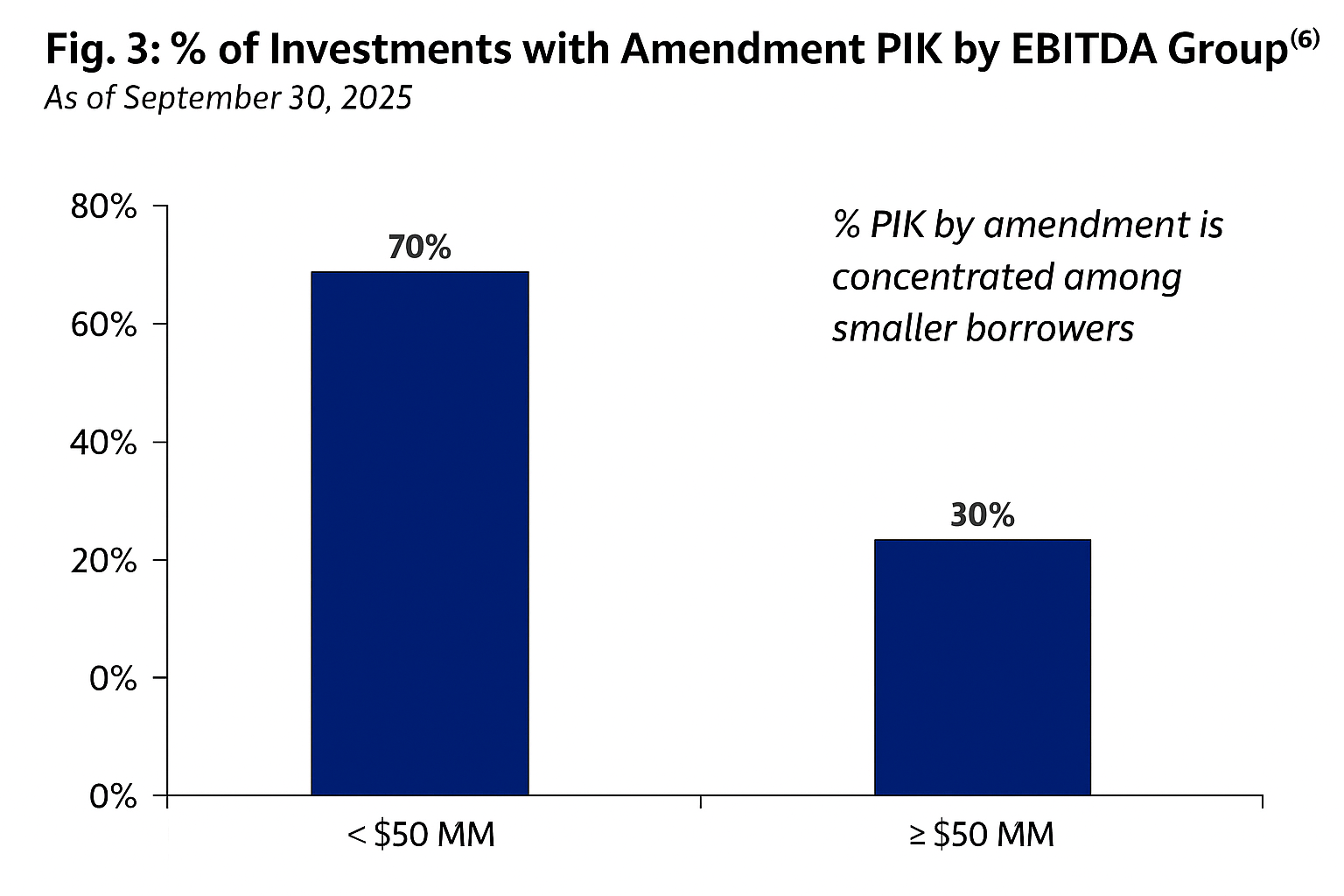

The use of PIK by amendment is a potential signal of credit stress. As shown in Fig. 2, PIK by amendment as a percentage of direct lending investments has risen from 2.6% in 2021 to 6.1% in Q3 2025, reflecting its growing prevalence. However, these PIK by amendment scenarios are concentrated among smaller borrowers, where 70% of PIKs by amendment are to borrowers with <$50 MM annual EBITDA, as shown in Fig. 3.(7)

OHA believes PIK by amendment is another indicator of the relative strength of larger companies compared to smaller companies. This characteristic reinforces OHA’s strategic focus on larger borrowers, aiming to mitigate downside risk and deliver attractive, risk-adjusted returns when evaluating private credit opportunities.

PIK Considerations

PIK financing can be an effective tool in private credit investing by helping to preserve borrower liquidity while delivering lenders an attractive spread premium. However, it is essential to thoroughly evaluate both the benefits and the considerations of PIK flexibility before incorporating it into a transaction.

Benefits

Growth Opportunity:

PIK features at origination allow high-quality senior direct lending borrowers to support future growth initiatives by reducing the burden of cash-pay interest during the first ~ two-years of the loan.

Spread Premium:

Lenders generally receive a 25 – 50 basis points premium when a PIK option is exercised to compensate for added structural complexity and foregone cash payments compared to a traditional cash-pay loan.

Capital Efficiency:

PIK financing does not require the lender to reserve capital for when a borrower draws on the commitment, as occurs in a typical senior private loan facility structure.

Considerations

Complexity:

PIK financing demands skilled lenders who can accurately assess the borrowers’ risk / reward profile, factoring in credit quality and liquidity needs. When executed effectively, this complexity creates an opportunity for experienced lenders to capture a meaningful spread premium while maintaining downside protection.

Context Matters:

Not all PIK opportunities are created equal, and given their higher-risk nature, lenders must determine whether incorporating PIK in a borrower’s loan structure is the appropriate solution.

Borrower Size:

Borrower size is a key consideration when evaluating private credit investments. Historically, smaller borrowers have been more likely to require PIK amendments after origination, which can introduce added complexity and risk. OHA believes its focus on larger borrowers is a critical part of its strategy to seek to generate alpha across market environments.

TAKEAWAYS

- OHA believes modest PIK exposure can be an effective way for lenders to capture additional spread, demonstrating the “complexity premium” offered by private credit

- OHA believes investors should carefully evaluate a manager’s underwriting process and structuring expertise when considering the use of PIK in private credit portfolios, as credit selection should be the largest determinant of performance over time

- Summer 2024

- Video

Industry spotlight: software credit

Read more to learn why OHA believes software companies can offer attractive all-weather investment profiles and inherent diversification as an “industry of industries”.

- Spring 2024

Credit market observations

Delve into OHA's analysis of credit markets, covering a wide range of assets including private, liquid, and structured credit.

Key risks and disclosures

This confidential document is for informational purposes only and does not constitute an offer to sell or a solicitation of an offer to buy any securities or partnership interests described herein. Interests in each fund may not be purchased except pursuant to each fund’s confidential private offering memorandum or relevant partnership agreement, which should be reviewed in its entirety prior to investment. Potential investors are urged to consult a professional regarding the possible economic, tax, legal, or other consequences of entering into any investments or transactions described herein. Any investor who subscribes, or proposes to subscribe, for an investment in each fund must be able to bear the risks involved and must meet each fund’s suitability requirements. Some or all alternative investment programs may not be suitable for certain investors. No assurance can be given that each fund’s investment objectives will be achieved. Alternative investments, including each fund, are speculative and involve a substantial degree of risk. Opportunities for withdrawal/redemption and transferability of interests are generally restricted, so investors may not have access to capital when it is needed. Oak Hill Advisors, L.P. (“OHA”) has total trading authority. The use of a single advisor applying generally similar trading programs could mean lack of diversification and, consequently, higher risk. Each fund may be leveraged and engage in other speculative practices that may increase the risk of investment loss or make investment performance volatile. In addition, the fees and expenses charged in connection with a fund may be higher than the fees and expenses of other investment alternatives, which will reduce profits. There can be no assurance that OHA will be able to implement its strategy or avoid incurring any losses.

There is no guarantee that an investor would achieve results comparable to those presented. All investments involve the risk of material or total loss. Past performance is not necessarily indicative of future results. The data used to calculate the returns is unaudited and subject to revision.

Opinions and estimates offered herein constitute the judgment of OHA as of the date this document is provided to you (unless otherwise noted) and are subject to change as are statements about market trends. All opinions and estimates are based on assumptions, all of which are difficult to predict and many of which are beyond the control of OHA in addition, any calculations used to generate the estimates were not prepared with a view towards public disclosure or compliance with any published guidelines. In preparing this document, OHA has relied upon and assumed, without independent verification, the accuracy and completeness of all information. OHA believes that the information provided herein is reliable; however, it does not warrant its accuracy or completeness.

This document may contain, or may be deemed to contain, forward-looking statements, which are statements other than statements of historical facts. By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. The future of investment results of the investments described herein may vary from the results expressed in, or implied by, any forward-looking statements included in this document, possibly to a material degree.

The offer and sale of any securities, products, services and/or interests described herein may be restricted or prohibited by law in certain jurisdictions. Some of these restrictions are described in the Appendix at the end of this document, if applicable. Prospective investors should inform themselves as to the legal requirements and tax consequences of the receipt of this document and the acquisition, holding and disposition of any investment described herein within the countries of their citizenship, residence, domicile and place of business.

The track records referenced herein, if included, reflect a subset of investments made by certain Client Accounts (as defined within the respective track record endnotes). The investments included in the track records were not managed as a single portfolio and may not be representative of what would have been achieved in a single portfolio. Because the track records reflect a subset of investments made by certain Client Accounts whose strategies included investments other than those included in the respective track record, such Client Accounts may have experienced significantly different returns than the returns provided herein. Further, as applicable, the account structures, advisory fee rates, performance compensation rates, expenses, capital structures, liquidity terms, holding periods, investment sizes, leverage (including the use of any subscription credit facility), investment guidelines, diversification requirements, foreign exchange management requirements, risk-return thresholds, strategies and other guidelines, objectives and requirements are different for each Client Account and therefore, the investment results included are not directly comparable to the portfolio that any specific Client Account may hold or the results that each individual Client Account or prospective investor has obtained or can expect to obtain.

The endnotes appearing at the end of this document, if included, are an integral part of this document and should be read in their entirety. This document has been prepared solely for the use of persons interested in obtaining detailed information on each fund and the investment advisory services of OHA and/or any of its subsidiary investment advisers. This document is not to be distributed without the prior written consent of OHA.

In the United States, this material is distributed by T. Rowe Price Investment Services, Inc. (“TRPIS”), a broker dealer registered with the U.S. Securities and Exchange Commission and a member of FINRA. Securities are offered through TRPIS, and advisory services are offered by OHA. TRPIS and OHA are both T. Rowe Price Group, Inc. affiliates. The recipient may contact a TRPIS registered representative located at OHA at (212) 326-1500 to obtain additional information or ask questions about any information, including the methodology used for any calculations and details concerning any summary charts or information provided herein.

© 2025 Oak Hill Advisors. All Rights Reserved. OHA is a trademark of Oak Hill Advisors, L.P. All other trademarks shown are the property of their respective owners. Use does not imply endorsement, sponsorship, or affiliation of Oak Hill Advisors with any of the trademark owners.

202502-4264032