How We’re Investing Through the Coronavirus Pandemic

- T. Rowe Price managers see a broad range of opportunity as well as risks in the volatile market environment.

- We highlight opportunities in the technology, health care, energy, and credit sectors as well as in Asia ex‑Japan.

- We are optimistic over the medium term that a new bull market can potentially be born from lower equity valuations as economies stabilize and normalize.

Investors face tremendous uncertainty and potentially more market volatility as businesses and consumers encounter continued economic disruption stemming from the coronavirus pandemic.

T. Rowe Price equity and fixed income managers are mindful that extreme market dislocations provide opportunities but also present risks, requiring careful analysis to seek out quality companies that have the financial strength, competitive position, and capable managements to survive the crisis and perhaps emerge even stronger. We’d like to share with you some of the more salient topics our managers are discussing.

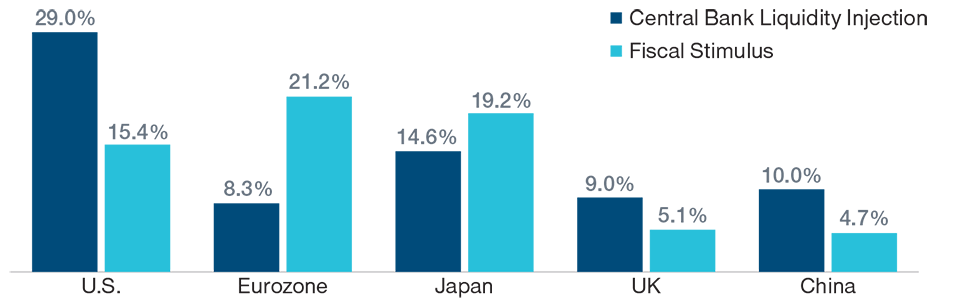

Pandemic’s Global Economic Stimulus

(Fig. 1) Percent of gross domestic product (GDP)

As of April 30, 2020.

Source: Cornerstone Macro.

It appears that we are still relatively early in a golden age for technology innovation....

It appears that we are still relatively early in a golden age for technology innovation....

Digitization Gathers Steam

The digitization of a wide range of industries and markets has accelerated during the pandemic. As individuals around the globe work, shop, and consume entertainment at home, companies that provide the infrastructure for the online economy have seen demand for their services boom, allowing them to extend their dominance.

Alan Tu, manager of the Global Technology Equity Strategy, notes that in this new digitized world, scale is crucial. Companies with the most capital to deploy can invest in the latest technology, which in turn attracts more customers. The tech giants that have best embodied this phenomenon are the world’s leading platform companies—a list that typically includes Facebook, Alphabet (Google), Apple, and Amazon.com in the U.S. and Alibaba and Tencent in China.

The leading players in the semiconductor industry have also grown more dominant over the past decade. Growing demand for leading‑edge chips to power computing‑intensive workflows and the rising costs associated with producing these advanced semiconductors give an important potential advantage to a select set of leading firms.

Along with advertisers and retailers, the media industry has been upended by online platforms that offer an improved customer experience. The primary disruptor has been Netflix, which has rapidly been adding subscribers during the pandemic. Amid the shutdown of production sets, Netflix stands apart in being able to draw on its huge, multinational library of previously filmed content.

Alan says that while tech giants have played a prominent role in the digitization of the economy, smaller industry upstarts are also sources of innovation and disruption, exploiting emerging areas where online services are making communicating and transacting easier. Investors may find some of the best investment opportunities in these younger and smaller companies, which could become takeover targets of the industry’s giants.

Being on the right side of change means identifying and investing in companies that make it easier for businesses of all sizes and across the economy to expand their online presence, improve productivity, and engage customers across multiple channels. It appears that we are still relatively early in a golden age for technology innovation, as the extraordinary power of the internet has enabled unprecedented value creation for both companies and investors.

Health Care: Changing Perceptions

Ziad Bakri, manager of the Health Sciences Strategy, believes that the longer‑term impact of the pandemic will be that investors will likely put an even greater premium on innovation and novel drug platforms. This should result in an even wider spread in valuations between “high and low value” medicines.

The intense focus on the importance of drug development during this crisis is also likely to change public perceptions on the trade‑off between drug pricing and innovation. As the regulatory overhang diminishes, valuations in the sector are likely to benefit.

Likewise, diminished political risk of a drastic overhaul of the U.S. health care system may provide a tailwind for managed care companies, at least in the intermediate term. More health care will likely be conducted virtually now that telehealth has demonstrated its viability and cost savings.

Ziad says his investment philosophy hasn’t changed as a result of the crisis. In the therapeutics and medical device sectors, he’s looking to invest in medicines and products that can meaningfully improve the standard of care and represent important advances in medical practice. The portfolio is evenly split between therapeutics (biotechnology and pharmaceuticals) and non‑therapeutics (life sciences, medical devices, and services).

Energy: Expecting a Near‑Term Comeback Amid a Secular Bear Market

Shawn Driscoll, manager of the Global Natural Resources Strategy, sees the potential for a powerful, countercyclical rally in crude oil prices and energy stocks that could last between 12 and 24 months as low energy prices drive supply cuts and oil demand potentially recovers from an unprecedented shock.

However, his longer‑term outlook for oil and the energy sector remains less sanguine. He believes that ongoing productivity gains from automation and improved reservoir management techniques in U.S. shale fields, among other factors, should continue to make hydrocarbons easier and less expensive to extract.

Among exploration and production (E&P) companies, Shawn prefers low‑cost operators that boast good balance sheets and sizable inventories of quality locations to drill wells. Although he likes many of the oil majors’ strong balance sheets, he has become more selective in that industry, avoiding names where strategic shifts could result in identity crises that distract management teams and dilute returns.

Shawn also sees select investment opportunities among oil field services companies and believes that the likelihood of a wave of bankruptcies in the industry, coupled with the flight of labor, could enable the survivors to raise prices for the first time in a long while as demand recovers.

Ryan Hedrick, an associate portfolio manager on our Large‑Cap Value Equity Strategies team, is finding opportunities in energy stocks that offer attractive dividend yields, including select names that own pipelines and other energy infrastructure and that he believes should generate more durable cash flows than their peers. The major integrated oil companies also fit this profile to an extent. He agrees that the magnitude of pain has created some opportunities in the more cyclical parts of the energy sector, specifically E&P and oil field services companies.

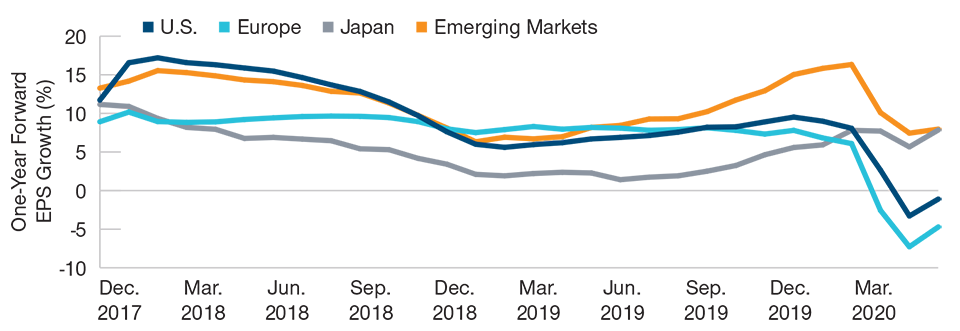

Global Earnings Growth Estimates

(Fig. 2) One‑year forward earnings per share (EPS) growth

As of May 26, 2020.

Source: FactSet. Financial data and analytics provider FactSet. Copyright 2020 FactSet. All Rights Reserved

Indices: US: S&P 500, Europe: MSCI Europe, Japan: MSCI Japan, Emerging Markets: MSCI Emerging Markets.

Where Does Value Investing Go From Here?

U.S. value investing’s decade‑long underperformance versus growth investing has widened since the onslaught of the pandemic.

John Linehan, Chief Investment Officer, Equity, says our objective, as always, with value investing is to find stocks that are trading at a significant discount to their intrinsic value. The current cheapness of so many industries means that companies with low valuations are plentiful; the challenge is to identify those that are likely to make it through to the other side intact. This requires in‑depth analysis of companies’ balance sheets, liquidity, and access to credit markets.

The managers of our value strategies have been able to upgrade the quality of their portfolios while, with a keen focus on the balance sheet, shifting selectively to more cyclical sectors. They increased their exposure to real estate, looking to take advantage of lower valuations and investor sentiment. They also added to semiconductors as the current environment is expected to further accelerate the proliferation of the internet of things.

Tom Huber, manager of the US Dividend Growth Equity Strategy, has also been buying high‑quality cyclicals, especially information technology and industrial companies developing innovative products. Meanwhile, our US Large‑Cap Value Equity Strategy, has been adding to positions in the bank, food product, and consumer discretionary categories.

Ryan Hedrick sees a slate of opportunities for utilities, driven by some of the following secular tailwinds: the shift from coal to natural gas and renewables for electricity generation; a corresponding mandate to modernize transmission and distribution infrastructure; the need to invest in older infrastructure to improve safety and reduce downtime; and the push to harden these critical systems against wildfires, hurricanes, and other natural disasters.

Although utilities’ resilient cash flows and dividend yields give the sector its defensive reputation, we believe the outlook for earnings growth makes the group’s risk‑adjusted value proposition more attractive.

...investors will likely put an even greater premium on innovation and novel drug platforms.

Opportunities in Asia ex‑Japan

Equity managers in Asia ex‑Japan strategies say the market downturn provided the opportunity to build positions in high‑quality companies that previously traded at prohibitive valuations.

Eric Moffett, manager of the Asia Opportunities Equity Strategy, sees the best potential opportunities in southeast Asia and India. In China, the A‑share market of domestic stocks has held up relatively well. His focus in China remains on two big areas where the tailwinds have only strengthened, partly as a result of the coronavirus.

The first is consolidating industries dominated by a few big players among many competitors. Whether that is in property development, retail, or certain industrials, Eric expects consolidation to accelerate, creating attractive opportunities. In industrial technology, for example, there are many good Chinese companies serving the domestic market—including factory automation, industrial motors, or components used in electric vehicles— that could become global competitors.

The other area is import substitution. As a result of the trade war with the U.S. last year, many Chinese companies wanted to avoid dependence on U.S. suppliers, so there was a move toward import substitution and less reliance on global supply chains. That trend is accelerating this year. Many of these companies are focused on the domestic market but could become competitive global players over time.

Fixed Income: Regaining Its Footing After the Upheaval

Unprecedented fiscal and monetary responses to the coronavirus pandemic have fortified credit markets. New issuance in investment‑grade and high yield corporate debt and emerging market bonds was heavy following the sell‑off, but well received. Looking across the fixed income landscape, our managers highlight opportunities and risks.

Munis:

Fears about the economic impact of the coronavirus pandemic in March, coupled with an atypical lack of liquidity, led to nearly unprecedented volatility in the municipal bond market. The market has remained under pressure as state and local governments contend with a loss of tax revenue and mounting expenses. Liquidity has improved, but risk appetite is low, generating periodic opportunities to buy muni bonds at historically attractive prices.

Hugh McGuirk, head of our municipal bond team and a portfolio manager, says we are focusing on bonds trading at prices that we think do not reflect their intrinsic value and that have strong balance sheets. With muni yields attractive relative to taxable securities, such opportunities can potentially produce solid longer‑term returns.

The asset class should remain high quality, but perhaps the most meaningful risk is the deterioration in the fundamentals of most issuers as the costs of the pandemic strain the finances of many municipalities. We believe that our municipal credit analysts are well prepared to evaluate this risk across issuers, helping our portfolio managers select bonds with solid fundamentals.

Securitized Credit:

Securitized credit instruments—which include asset‑backed securities (ABS), commercial mortgage‑backed securities (CMBS), and residential mortgage‑backed securities without agency credit guarantees (RMBS)—have, on average, lagged the rebound in other fixed income sectors, challenged by limited liquidity and primary markets that have been much slower to open.

However, we expect liquidity to improve and believe that parts of securitized credit could outperform as the economy reopens. We rely on our team of experienced securitized credit analysts to help identify fundamentally strong bonds trading at dislocated prices.

Christopher Brown, lead portfolio manager of our Total Return Strategy, says that within RMBS, we have focused on some lower‑rated credit risk transfer (CRT) securities, which are a type of MBS issued by Fannie Mae and Freddie Mac but with the credit risk borne by private investors. CMBS have been among the hardest‑hit segments of securitized credit because of exposure to retail and lodging businesses, and new issuance remains largely on hold. In CMBS, we prefer bonds with high‑quality underlying assets and significant credit enhancement.

In ABS, we think that select whole business securitizations (WBS) from high‑quality issuers such as household‑name, quick‑service restaurants are attractive. The collateral backing WBS is generally a first‑priority interest in a company’s primary revenue‑generating assets, often franchise fees and royalties. The issuers that we prefer are brands that have been successfully operating for more than 40 years and have survived multiple economic cycles as well as significant changes in consumer behavior.

High Yield Bonds:

Despite a rebound in some cyclical sectors, our investment team sees risks and volatility remaining along with liquidity challenges and a rise in downgrades and the default rate, which hit a 10‑year high of 4.85% in May.1

In the embattled energy arena, Rodney Rayburn, portfolio manager of the Credit Opportunities and High Yield Bond Strategies, cites appealing opportunities among larger E&P companies that have relatively low leverage as well as higher‑quality midstream operators that have generated relatively stable cash flows and serve diverse, well‑positioned customer bases.

Rodney believes compelling opportunities in the energy sector could emerge when investment‑grade issuers get downgraded into the high yield universe. These “fallen angels” often come under pressure from forced selling by strategies that can only hold investment‑grade securities.

We continue to rely on our proprietary fundamental research to guard against defaults and credit problems. We focus most of our attention on issuers with solid cash flow, few near‑term maturities, and flexible liquidity.

Emerging Market Debt

The managers of our emerging market bond strategies are optimistic that investors will recognize that emerging market governments and the International Monetary Fund have the capacity to support fundamentals and valuations in emerging market credit.

Furthermore, they think that investors are pricing in widespread credit distress, but many issuers are expected to recover in coming months, even though there will probably be more defaults and volatility.

…we are optimistic over the medium term that a new bull market can potentially be born….

Investing Through Periods of Market Stress

With so much uncertainty still surrounding the pandemic, it is difficult to gauge just how long the acute economic disruption might last. It is certainly possible that the time frame for returning to a “normalized” environment could be longer than anticipated.

In our view, the global economy is entering a severe recession, and we expect corporate earnings this year to be depressed and unpredictable. At T. Rowe Price, when we analyze the prospects for stocks individually and collectively, we are thinking much more about normalized earnings into 2021 and onward. What those projected earnings are and how quickly stocks normalize their earning power will be the keys to recovery.

Despite the near‑term uncertainty, we are optimistic over the medium term that a new bull market can potentially be born from lower equity valuations, as we see stabilization and then normalization of economies.

1 According to J.P. Morgan Chase (see Additional Disclosure).

The specific securities identified and described are for informational purposes only and do not represent recommendations.

Additional Disclosure

Information has been obtained from sources believed to be reliable but J.P. Morgan does not warrant its completeness or accuracy. The index is used with permission. The Index may not be copied, used, or distributed without J.P. Morgan’s prior written approval. Copyright © 2020, J.P. Morgan Chase & Co. All rights reserved.

Important Information

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

Australia—Issued in Australia by T. Rowe Price Australia Limited (ABN: 13 620 668 895 and AFSL: 503741), Level 50, Governor Phillip Tower, 1 Farrer Place, Suite 50B, Sydney, NSW 2000, Australia. For Wholesale Clients only.

Canada—Issued in Canada by T. Rowe Price (Canada), Inc. T. Rowe Price (Canada), Inc.’s investment management services are only available to Accredited Investors as defined under National Instrument 45‑106. T. Rowe Price (Canada), Inc. enters into written delegation agreements with affiliates to provide investment management services.

DIFC—Issued in the Dubai International Financial Centre by T. Rowe Price International Ltd. This material is communicated on behalf of T. Rowe Price International Ltd. by its representative office which is regulated by the Dubai Financial Services Authority. For Professional Clients only.

EEA ex‑UK—Unless indicated otherwise this material is issued and approved by T. Rowe Price (Luxembourg) Management S.à r.l. 35 Boulevard du Prince Henri L‑1724 Luxembourg which is authorised and regulated by the Luxembourg Commission de Surveillance du Secteur Financier. For Professional Clients only.

Hong Kong—Issued by T. Rowe Price Hong Kong Limited, 6/F, Chater House, 8 Connaught Road Central, Hong Kong. T. Rowe Price Hong Kong Limited is licensed and regulated by the Securities & Futures Commission. For Professional Investors only.

New Zealand—Issued in New Zealand by T. Rowe Price Australia Limited (ABN: 13 620 668 895 and AFSL: 503741), Level 50, Governor Phillip Tower, 1 Farrer Place, Suite 50B, Sydney, NSW 2000, Australia. No Interests are offered to the public. Accordingly, the Interests may not, directly or indirectly, be offered, sold or delivered in New Zealand, nor may any offering document or advertisement in relation to any offer of the Interests be distributed in New Zealand, other than in circumstances where there is no contravention of the Financial Markets Conduct Act 2013.

Singapore—Issued in Singapore by T. Rowe Price Singapore Private Ltd., No. 501 Orchard Rd, #10‑02 Wheelock Place, Singapore 238880. T. Rowe Price Singapore Private Ltd. is licensed and regulated by the Monetary Authority of Singapore. For Institutional and Accredited Investors only.

Switzerland—Issued in Switzerland by T. Rowe Price (Switzerland) GmbH, Talstrasse 65, 6th Floor, 8001 Zurich, Switzerland. For Qualified Investors only.

UK—This material is issued and approved by T. Rowe Price International Ltd, 60 Queen Victoria Street, London, EC4N 4TZ which is authorised and regulated by the UK Financial Conduct Authority. For Professional Clients only.

USA—Issued in the USA by T. Rowe Price Associates, Inc., 100 East Pratt Street, Baltimore, MD, 21202, which is regulated by the U.S. Securities and Exchange Commission. For Institutional Investors only.

© 2020 T. Rowe Price. All rights reserved. T. Rowe Price, INVEST WITH CONFIDENCE, and the bighorn sheep design are, collectively and/or apart, trademarks or registered trademarks of T. Rowe Price Group, Inc.

ID0003228 (06/2020)

202005‑1197925