2026 Midyear Market Outlook: Five shifts reshaping markets

What’s next for markets in 2026

Competing forces drive a broader, more complex opportunity set

Competing forces drive a broader, more complex opportunity set

Markets have been anything but stable in the first half of 2026. A sequence of geopolitically driven shocks has collided with surging artificial intelligence (AI) investment, robust corporate earnings, and solid U.S. economic growth. Risk assets have remained relatively strong amid these crosscurrents. But the danger for investors is mistaking resilience for calm.

Many of the themes we identified at the start of the year have broadly played out: AI-driven growth, broader equity market performance, and continued strength in credit, even with upward pressures on bond yields. Macro forces are now driving a new and more dispersed opportunity set as the AI trade moves into physical sectors and geopolitical fissures reshape the global economy. The market regime is changing.

2026 Midyear Market Outlook - Summary

The first half of 2026 has reminded investors that markets can be resilient even when the world feels anything but stable. Geopolitical conflict, energy shocks, sticky inflation, and shifting supply chains have tested markets so far this year. Yet strong U.S. growth, healthy corporate earnings, and ongoing investment in artificial intelligence have helped support risk assets.

But beneath that resiliencThe first half of 2026 has reminded investors that markets can be resilient even when the world feels anything but stable. Geopolitical conflict, energy shocks, sticky inflation, and shifting supply chains have tested markets so far this year. Yet strong U.S. growth, healthy corporate earnings, and ongoing investment in artificial intelligence have helped support risk assets.

But beneath that resilience, a new market regime is beginning to take shape.

The global economy is becoming more fragmented, physical, and selective. Governments and companies are increasingly prioritizing energy security, domestic manufacturing, and supply chain diversification over efficiency. That shift may keep inflation higher and more volatile than investors have been used to.

Credit markets remain resilient, but disciplined credit selection is essential. With persistent inflation, we see opportunity in inflation-linked securities as portfolio hedges, alongside real assets.

AI is evolving from a purely digital story into a real-world infrastructure boom. Investment is spreading beyond large technology platforms into areas such as power, connectivity, and equipment. That broadening opportunity set is beginning to reshape market leadership into who owns the economic bottlenecks.

Meanwhile, the dominance of mega-cap technology stocks may be starting to fade as rising capital spending pressures free cash flow. Leadership is widening across sectors and regions, creating a more favorable backdrop for active investing and selective stock picking. Small-caps, value-oriented sectors, and select non-U.S. opportunities could benefit as dispersion increases and benchmark concentration weakens.

For investors and advisors, the message is clear: macro matters again.

Success may depend less on benchmark exposure and more on identifying companies and sectors positioned to thrive in markets defined by fragmentation, infrastructure investment, and durable earnings growth.e, a new market regime is beginning to take shape.

The global economy is becoming more fragmented, physical, and selective. Governments and companies are increasingly prioritizing energy security, domestic manufacturing, and supply chain diversification over efficiency. That shift may keep inflation higher and more volatile than investors have been used to.

Credit markets remain resilient, but disciplined credit selection is essential. With persistent inflation, we see opportunity in inflation-linked securities as portfolio hedges, alongside real assets.

AI is evolving from a purely digital story into a real-world infrastructure boom. Investment is spreading beyond large technology platforms into areas such as power,

connectivity, and equipment. That broadening opportunity set is beginning to reshape market leadership into who owns the economic bottlenecks.

Meanwhile, the dominance of mega-cap technology stocks may be starting to fade as rising capital spending pressures free cash flow. Leadership is widening across sectors and regions, creating a more favorable backdrop for active investing and selective stock picking. Small-caps, value-oriented sectors, and select non-U.S. opportunities could benefit as dispersion increases and benchmark concentration weakens.

For investors and advisors, the message is clear: macro matters again.

Success may depend less on benchmark exposure and more on identifying companies and sectors positioned to thrive in markets defined by fragmentation, infrastructure investment, and durable earnings growth.

- Scorecard

- Geopolitical Outlook

- Inflation Outlook

- Energy Outlook

- AI Outlook

- Return Dispersion Outlook

Revisiting our 2026 expectations

We were right that equity market leadership would broaden beyond mega-cap tech, but war-driven shocks have challenged our thesis on non-U.S. equities.

We were right that equity market leadership would broaden beyond mega-cap tech, but war-driven shocks have challenged our thesis on non-U.S. equities.

Nearly halfway through 2026, we looked back at the themes from our Global Market Outlook published last November. Many of the key trends we identified heading into this year, such as continued credit market resilience and broader equity market leadership, played out largely as anticipated.

Regional trends proved to be more mixed, however. While non-U.S. equities periodically outperformed, the bullish case for non-U.S. stock markets has weakened in the wake of the energy supply shock.

| Expectation at start of 2026 | How we did | On reflection |

|---|---|---|

| Fiscal expansion and AI investment would support U.S. growth | Fiscal expansion and AI‑related investment provided a stronger‑than‑expected underpinning for U.S. growth, supporting the economy | |

| The U.S. would outperform while the eurozone would lag as tariff front‑loading weighed on manufacturing | The U.S. has outperformed as expected, supported by resilient AI‑related investment and fiscal tailwinds, but anticipated eurozone manufacturing weakness has been less evident |

| Expectation at start of 2026 | How we did | On reflection |

|---|---|---|

| Equity market leadership would broaden beyond mega‑cap tech | Equity market leadership broadened beyond mega‑cap tech, with small‑caps and value stocks outperforming year‑to‑date1 even as AI‑related companies remained important drivers of returns | |

| AI would remain a key market driver, with leadership evolving | AI remained a dominant market driver, with leadership beginning to expand toward infrastructure and semiconductor enablers |

| Expectation at start of 2026 | How we did | On reflection |

|---|---|---|

| Fiscal expansion would push government bond yields higher | Government bond yields faced sustained upward pressure as the energy price shock, fiscal deficits, and increased issuance weighed on markets, reinforcing the influence of policy on interest rates | |

| Credit markets would remain resilient, but selectivity would be key | Credit markets remained broadly resilient, but tight valuations and emerging dispersion reinforced the importance of disciplined credit selection |

| Expectation at start of 2026 | How we did | On reflection |

|---|---|---|

| Equities would be favored over bonds | Equities generally outperformed bonds | |

| Non‑U.S. equities would offer stronger opportunities | Non‑U.S. equities showed improving fundamentals and periods of outperformance,1 but questions about the sustainability of those fundamentals have emerged due to headwinds from higher energy costs and less accommodative monetary policy |

“Expectations at start of 2026” are from our 2026 Global Market Outlook, issued in November 2025. The Scorecard does not reflect all views and expectations covered in that report. “How we did” reflects what we got right and wrong as of the time of this writing. The orange dash indicates we were partially right. Future outcomes may differ materially, and the information provided is subject to change. Past performance is not a guarantee or a reliable indicator of future performance.

1 Based on index data, as of May 29, 2026.

Geopolitical outlook

Rising global tensions are spurring reinvestment in domestic capacity and a broader shift toward economic fragmentation.

Rising global tensions are spurring reinvestment in domestic capacity and a broader shift toward economic fragmentation.

Policymakers worldwide are prioritizing energy security, domestic production, and supply chain leverage over efficiency and integration. This will likely widen regional divergences as globally exposed and trade-sensitive sectors face pressure. While markets have remained relatively strong this year, continued economic fragmentation is likely to drive a more differentiated and volatile environment.

Global supply chain pressures have spiked this year

Energy shocks and AI demand are lengthening delivery times

As of April 30, 2026.

Source: Global Supply Chain Pressure Index (GSPI), Federal Reserve Bank of New York.

Notes: GSCPI readings for the most recent months can be revised as realized data become available, replacing the imputed values generated through principal component analysis. Further, for some series, mainly the BLS airfreight cost indices, each new release comes with revisions to up to twelve months of previous data. Thus, revisions can have an impact up to a year back in time.

Source: Global Supply Chain Pressure Index (GSPI), Federal Reserve Bank of New York.

Notes: GSCPI readings for the most recent months can be revised as realized data become available, replacing the imputed values generated through principal component analysis. Further, for some series, mainly the BLS airfreight cost indices, each new release comes with revisions to up to twelve months of previous data. Thus, revisions can have an impact up to a year back in time.

What happens when supply chains are disrupted?

Potential impacts of the energy shock on inflation, growth, and interest rates

As of May 31, 2026. Analysis by T. Rowe Price. For illustrative purposes only.

Inflation outlook

The fight against inflation looks increasingly difficult as a manufacturing revival, fiscal expansion, and policy shifts introduce new risks.

The fight against inflation looks increasingly difficult as a manufacturing revival, fiscal expansion, and policy shifts introduce new risks.

Central banks are abandoning or reversing rate-cutting cycles amid the current energy shock, and the specter of stagflation further complicates monetary policy in some countries. At the same time, a global manufacturing recovery and rising industrial prices are adding to inflation pressures. Markets appear to be underestimating the longer-term inflation risks

Energy outlook

Energy scarcity is reshaping supply chains and opportunities

Energy scarcity is reshaping supply chains and opportunities

in commodities-related sectors.

War-driven supply shocks have exposed fragile energy markets, resulting in structurally higher prices, regional shortages, and rising demand for different sources of energy. In this new environment, the themes of energy security and diversification—in addition to critical minerals production—lead to compelling investment opportunities.

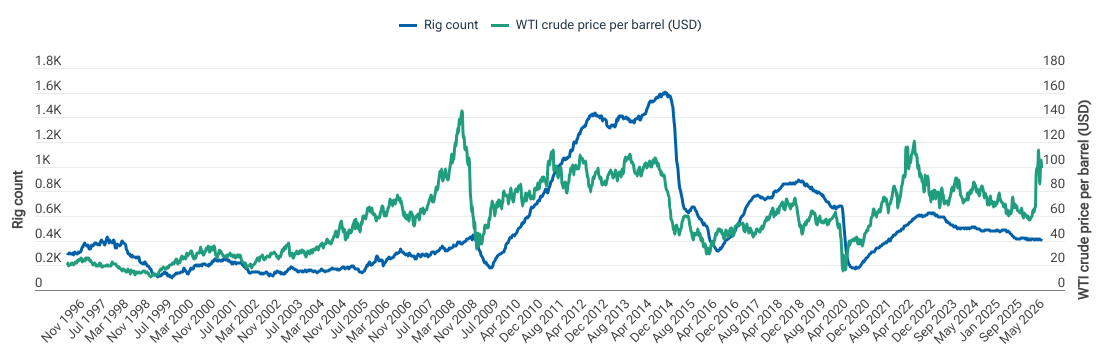

Oil markets were tightening before the Iran war

Rig count was falling despite elevated prices

As of April 30, 2026. Sources: Baker Hughes, West Texas Intermediate oil price.

AI outlook

AI is transitioning from a concentrated technology trade into a wider industrial and infrastructure investment cycle.

AI is transitioning from a concentrated technology trade into a wider industrial and infrastructure investment cycle.

As hyperscaler spending on AI accelerates, investment opportunities are expanding beyond semiconductors into infrastructure and industrial beneficiaries poised to capitalize on rising power, connectivity, and operational demands. But selective approaches toward the AI trade—rather than simple participation—will likely prove beneficial.

AI capex continues to soar

Hyperscaler capex, trailing 4‑quarter total

As of May 15, 2026.

E=Estimates.

K=1000.

The specific securities identified and described are for informational purposes only and do not represent recommendations to buy or sell any security. For illustrative purposes only. Estimates are consensus estimates. Actual outcomes may differ materially from estimates. Estimates are subject to change. Hyperscalers are cloud‑service providers that operate at an extremely large scale. This is a sample of U.S. hyperscalers and is not an all‑inclusive list. Source: T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved.

E=Estimates.

K=1000.

The specific securities identified and described are for informational purposes only and do not represent recommendations to buy or sell any security. For illustrative purposes only. Estimates are consensus estimates. Actual outcomes may differ materially from estimates. Estimates are subject to change. Hyperscalers are cloud‑service providers that operate at an extremely large scale. This is a sample of U.S. hyperscalers and is not an all‑inclusive list. Source: T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved.

The great rotation

Returns may shift toward infrastructure providers

Analysis by T. Rowe Price. For illustrative purposes only. Actual outcomes may differ materially.

Return dispersion outlook

The conditions that supported market concentration are shifting, expanding the opportunity set beyond the past cycle’s winners.

The conditions that supported market concentration are shifting, expanding the opportunity set beyond the past cycle’s winners.

The era dominated by scale and asset-light business models is giving way to a new equilibrium. As AI infrastructure spending has rewired market dynamics, leadership has begun to broaden across sectors and geographies. Active investors who can distinguish between capital investment that enhances returns and spending that dilutes them should be well positioned to take advantage of this shift.

Sign up to receive our monthly Global Asset Allocation Viewpoints from our Investment Committee

Each month, our Investment Committee prepare a report revealing the two market themes they are watching, their bull and bear views per region and their latest asset class over and underweights.It has been designed to aid you in your decision making and client conversations.

Investment Risks:

Active investing may have higher costs than passive investing and may underperform the broad market or passive peers with similar objectives. Each person’s investing situation and circumstances differ. Investors should take all considerations into account before investing.

International investments can be riskier than U.S. investments due to the adverse effects of currency exchange rates, differences in market structure and liquidity, as well as specific country, regional, and economic developments. The risks of international investing are heightened for investments in emerging market and frontier market countries. Emerging and frontier market countries tend to have economic structures that are less diverse and mature, and political systems that are less stable, than those of developed market countries.

Commodities are subject to increased risks such as higher price volatility and geopolitical and other risks. Commodity prices can be subject to extreme volatility and significant price swings.

Inflation-linked bonds (Treasury inflation protected securities in the U.S.): In periods of no or low inflation, other types of bonds, such as U.S. Treasury bonds, may perform better than Treasury inflation protected securities (TIPS).

Investing in technology stocks entails specific risks, including the potential for wide variations in performance and usually wide price swings, up and down. Technology companies can be affected by, among other things, intense competition, government regulation, earnings disappointments, dependency on patent protection, and rapid obsolescence of products and services due to technological innovations or changing consumer preferences.

Fixed income securities are subject to credit risk, liquidity risk, call risk, and interest rate risk. As interest rates rise, bond prices generally fall. Investments in high yield bonds involve greater risk of price volatility, illiquidity, and default than higher-rated debt securities. Investments in bank loans may at times become difficult

Because of the cyclical nature of natural resource companies, their stock prices and rates of earnings growth may follow an irregular path.

The value approach to investing carries the risk that the market will not recognize a security’s intrinsic value for a long time or that a stock judged to be undervalued may actually be appropriately priced. Growth stocks are subject to the volatility inherent in common stock investing, and their share price may fluctuate more than that of income‑oriented stocks.

All investments involve risk, including possible loss of principal. Diversification cannot assure a profit or protect against loss in a declining market. Index performance is for illustrative purposes only and is not indicative of any specific investment. Investors cannot invest directly in an index.

T. Rowe Price cautions that economic estimates and forward‑looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual outcomes could differ materially from those anticipated in estimates and forward‑looking statements, and future results could differ materially from any historical performance. The information presented herein is shown for illustrative, informational purposes only. Any historical data used as a basis for this analysis are based on information gathered by T. Rowe Price and from third‑party sources and have not been independently verified. Forward‑looking statements speak only as of the date they are made, and T. Rowe Price assumes no duty to and does not undertake to update forward‑looking statements.

Important Information

This material is being furnished for informational and/or marketing purposes only and does not constitute an offer, recommendation, advice, or solicitation to sell or buy any security.

Prospective investors should seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services.

Past performance is not a guarantee or a reliable indicator of future results. All investments involve risk, including possible loss of principal.

Information presented has been obtained from sources believed to be reliable, however, we cannot guarantee the accuracy or completeness. The views contained herein are those of the author(s), are as of November 14, 2025, are subject to change, and may differ from the views of other T. Rowe Price Group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

All charts and tables are shown for illustrative purposes only. Actual future outcomes may differ materially from any estimates or forward-looking statements provided.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

EEA—Unless indicated otherwise this material is issued and approved by T. Rowe Price (Luxembourg) Management S.à r.l. 35 Boulevard du Prince Henri L-1724 Luxembourg which is authorised and regulated by the Luxembourg Commission de Surveillance du Secteur Financier. For Professional Clients only.

Switzerland—Issued in Switzerland by T. Rowe Price (Switzerland) GmbH, Talstrasse 65, 6th Floor, 8001 Zurich, Switzerland. For Qualified Investors only.

UK—This material is issued and approved by T. Rowe Price International Ltd, Warwick Court, 5 Paternoster Square, London EC4M 7DX which is authorised and regulated by the UK Financial Conduct Authority. For Professional Clients only.

202605-5512997