June 2023 / INVESTMENT INSIGHTS

Why an All-Weather Approach Works Best for Euro Corporate Bonds

Aiming for outperformance through good and bad times matters

Focusing on delivering outperformance in varying market conditions, whether credit spreads are rising or falling or if volatility is high, is an ideal way to approach euro corporate bonds, in our view. We think an all‑weather approach will resonate with investors who view the asset class as a potential core allocation within their fixed income sleeve and aim for regular income without excessive price fluctuations.

In our two decades managing the T. Rowe Price Funds SICAV—Euro Corporate Bond Fund,1 we have seen higher‑beta2 managers perform strongly in good times, when credit spreads are falling, but then underperform when things turn bad. Investment‑grade credit, by its nature, has potentially greater downside than upside risk.3 As such, we think it is essential to mitigate drawdowns by avoiding companies with poor or deteriorating creditworthiness.

We believe this approach works well over the long term but is also relevant to the current environment. The volatility in the banking sector in March, an especially challenging year for bonds in 2022 and the current uncertain market and macroeconomic outlook underline the importance of consistency and stability.

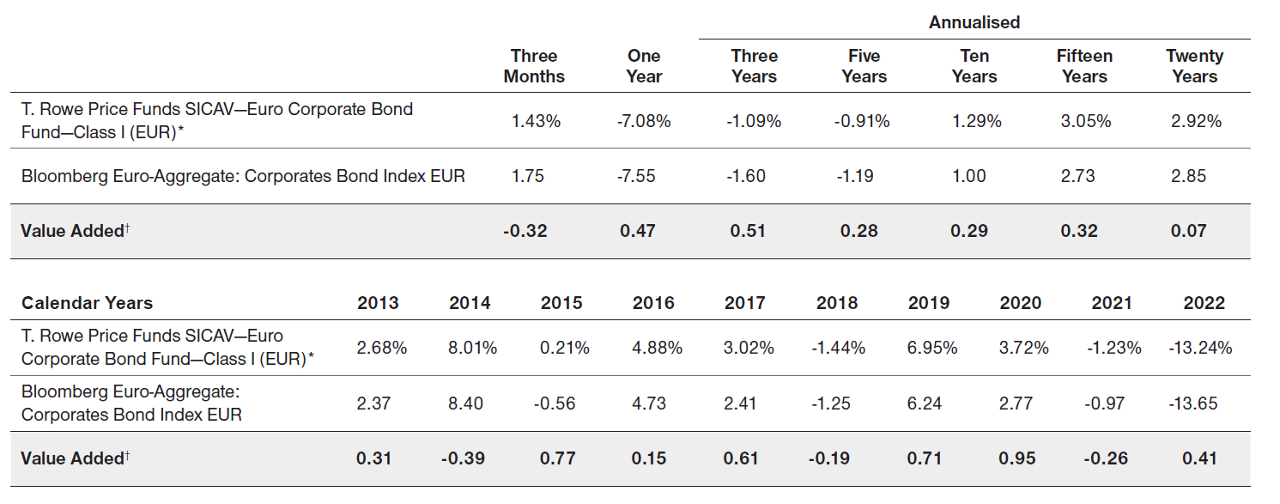

Performance Table

T. Rowe Price Funds SICAV—Euro Corporate Bond Fund

Past performance is not a reliable indicator of future performance.

*Source for performance: T. Rowe Price as of 31 March 2023. Fund performance is calculated using the official net asset value with dividends reinvested, if any. The value of the investment will vary and is not guaranteed. It will be affected by changes in the exchange rate between the base currency of the fund and the subscription currency, if different. Sales charges (up to a maximum of 5% for the A Class), taxes, and other locally applied costs have not been deducted, and, if applicable, they will reduce the performance figures. Where the base currency of the fund differs from the share class currency, exchange rate movements may affect returns.

† The Value Added row is shown as T. Rowe Price Funds SICAV—Euro Corporate Bond Fund—Class I (EUR) minus the benchmark in the previous row.

Source for Bloomberg index data: Bloomberg Index Services Limited. Please see Additional Disclosures page for information about this Bloomberg information.

The manager is not constrained by the fund’s benchmark, which is used for performance comparison purposes only.

How Do We Pursue Outperformance in All Weathers?

Firstly, it is important to target higher gains than the market when credit spreads are tightening. High‑conviction security selection, with a focus on picking the right companies and issues, is the main way we attempt to stay ahead when conditions are favourable.

We seek to generate an attractive yield in the portfolio but do this in a considered and balanced way, assessing carry opportunities relative to risk and volatility.

The yield on euro investment‑grade corporate bonds is currently higher than it has been for more than a decade. There is also the opportunity for capital appreciation, particularly in issues with scope for credit spread tightening or with a generous premium at launch.

Intensive company‑level research by our 18‑strong team of dedicated euro investment‑grade analysts helps us to identify the best opportunities, and we incorporate active views on rating, maturity, and seniority in our decisions. We also draw on support from in‑house economists, sovereign analysts, quantitative analysts, a responsible investment team and traders.

It is vital to try and outperform through difficult times as well, however, by adapting and responding to changing market conditions.

There are four key rules for steering through choppy waters:

Know your cargo: Just as we back the companies in which we have the highest conviction, we also seek to avoid the weaker ones. This approach will hopefully be beneficial when markets fall and should add value over time. Crucially, we determine how much pain we are willing to accept in each issue that we own, so we are ready to jettison names when needed or when we lose conviction. At the same time, we will firmly back positions where we are convinced of potential future success.

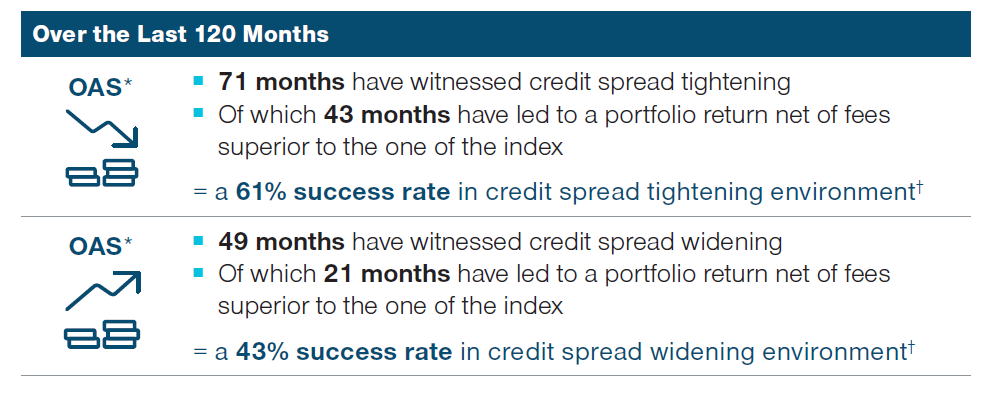

Performance Regularity Matters

(Fig. 1) Our fund has outperformed in different environments

As of 31 March 2023.

Past performance is not a reliable indicator of future performance.

*Option‑adjusted spread.

† The active success rate is the percentage of rolling periods that a T. Rowe Price fund generated excess returns that were greater than zero, indicating that it outperformed its benchmark, over the last 10 years. Outperformance is calculated as T. Rowe Price Funds SICAV—Euro Corporate Bond Fund—Class I (EUR) minus the Bloomberg Euro Aggregate Corporate Index. A composite that outperformed its benchmark in more than 50% of all rolling periods in a given time window was deemed to have achieved a positive active success rate for that window. The manager is not constrained by the fund’s benchmark, which is used for performance comparison purposes only. Source for performance: T. Rowe Price. Fund performance is calculated using the official net asset value with dividends reinvested, if any. The value of the investment will vary and is not guaranteed. It will be affected by changes in the exchange rate between the base currency of the fund and the subscription currency, if different. Sales charges (up to a maximum of 5% for the A Class), taxes, and other locally applied costs have not been deducted, and, if applicable, they will reduce the performance figures.Where the base currency of the fund differs from the share class currency, exchange rate movements may affect returns.

Source for Bloomberg index data: Bloomberg Index Services Limited. Please see Additional Disclosures page for information about this Bloomberg information.

Distribute the weights correctly: The ability to manage idiosyncratic situations by distributing risk across the portfolio is an important factor at both a company level and a sector level. We maintain a high degree of diversification—holding 100 to 200 issuers at any point in time—carefully weighting positions at issue level based on conviction, rating, and liquidity profile. By maintaining a portfolio that is not dominated by any one sector, geographic region, rating or issuer, alpha is driven by numerous factors to help keep the volatility of performance low. It means we have some built‑in resilience for when markets turn.

When storms approach, increase the ballast: When there are signs of a storm coming, we seek to reduce risk by employing credit derivatives to cushion the portfolio at times of rapidly increasing volatility, when credit is likely to underperform. Our use of credit default swaps on individual issuers or at an index level, either as short positions or option structures, has added value over time and was particularly important in 2022.

Rely on a knowledgeable crew: Portfolio Managers David Stanley and Howard Woodward have more than three decades of expertise each in the credit industry, including managing through numerous credit crises and liquidity squeezes. They are surrounded by a team of seasoned credit portfolio analysts based in the UK, the US and Asia.

Why an All‑Weather Approach Is Important Now

The ability to see out choppy conditions looks increasingly important in a world facing numerous transitions and uncertainties and even, as some would say, a new economic regime.

Firstly, an era of historically low interest rates and bond yields appears to be over, following aggressive monetary tightening. While this creates a healthier income environment for bond investors, it also introduces scope for greater volatility and more challenging economic conditions. The safety net of highly supportive policy measures is gone, and companies will have to pay more to issue debt, squeezing balance sheets.

Recent failures among US regional banks demonstrate the risks that higher interest rates introduce. Aside from the negative effect on sentiment, this may hurt the economy as the banking sector tightens up on lending, possibly increasing the risk of a recession.

As economic conditions become harder, with the lagged effect of tightening starting to bite, there may be more losers, in and outside of banking, particularly if panic sets in again, although winners will emerge too.

Added to this is the question of inflation. This looks likely to moderate further from the eye‑watering levels seen in 2022, but how much moderation will be enough to stop further interest rate rises is difficult to gauge. It is likely we will all have to adjust to higher rates of inflation overall than we have been used to over the past decade.

Finally, there is continued geopolitical uncertainty, particularly the ongoing war in Ukraine and the potential here for further destabilisation via energy supply disruption.

Performance Regularity Is Vital in a Changeable World

Taking all these factors together, there is considerable scope for financial markets to remain changeable and volatile. Discerning investment management will be key. Performance regularity, based on careful security selection, steady income and rigorous downside risk management could be essential for today’s uncertain investment landscape.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.