July 2022 / INVESTMENT INSIGHTS

Emerging Markets Face a Highly Varied Growth Outlook

Inflation and monetary policies are not affecting regions equally

Key Insights

- Russia’s invasion of Ukraine has complicated the investment environment for emerging market (EM) investors.

- The EM growth outlook is mixed, with considerable variation between regions.

- Many central and Eastern European and Latin American EM countries have been hiking rates aggressively, which should slow growth in those regions. Asia is much further behind in the cycle.

Global and Regional Politics

Geopolitical risks, and the war in Ukraine in particular, have created a very difficult environment for global investing. There is a sense of major precedents being shattered, the implications of which will take time to become clear. While EMs are unlikely to dump the U.S. dollar as a reserve currency, they will continue to seek ways to erode its usage. In the near term, however, sanctions risk is a more pressing concern.

Any Chinese trade with Russia will come under scrutiny. For now, the main Chinese institutions are not overtly challenging sanctions, but China has networks to continue to trade with countries such as Iran and North Korea that do not expose its major institutions to secondary sanctions. More broadly, the conflict will force a rethink about the probability of tail risks and the potential for new conflicts to arise in other regions.

For global markets, a major risk would be a disorderly oil embargo by the EU that is backed by sanctions that limit how much oil Russia can redirect to other countries, or Russia self‑embargoing to exert pressure on the EU. (For example, the fight over ruble payments for gas could escalate further.)

On the domestic side, two key elections have taken place, and one is set to be held in the autumn. Colombia’s next president will be former leftist rebel Gustavo Petro, who beat Rodolfo Hernández in the second round of the presidential election in late June. In the Philippines, Ferdinand Marcos, Jr., son of former dictator Ferdinand Marcos, Sr., achieved a comfortable victory in May’s presidential election. In Brazil, center‑left candidate Luiz Inácio Lula da Silva is the frontrunner for autumn’s election, but incumbent President Jair Bolsonaro has been closing the gap.

Beyond these scheduled elections, there is a strong likelihood of early elections in Malaysia and the possibility of an election in Pakistan. The political crisis in Sri Lanka deepened in mid-July when President Gotabaya Rajapaksa fled the country after months of turmoil culminated in protesters descending on the presidential palace.

Growth

EM growth is largely flat overall. Latin America and the central and Eastern Europe, Middle East, and Africa (CEMEA) region, are leading, with some countries showing signs of having positive output gaps. The main drag on growth has been China, where pandemic‑related shocks are now being felt after other indicators showed a reasonably strong start to the year.

China’s potential drag on EM growth could be significant if the COVID‑19 situation is not brought under control. Although China’s slowing economy last year did not transmit to EMs as the reopening of developed markets following the pandemic lockdowns proved sufficient to keep commodities elevated, China could resume having more of an impact on EMs via commodity prices this year.

The growth outlook for EMs is mixed, with considerable variation between regions. Many Latin American and CEMEA countries are now facing inflationary pressures and the prospect of central bank tightening, which should cause growth to slow in those regions. Further headwinds will come from developed markets, where central banks are also beginning to tighten and a rotation in demand is occurring away from pandemic‑era goods as economies reopen. This could lead to a fall in exports to developed markets, which will drag on growth.

In Asia, where economies are beginning to open up and there is less inflationary pressure because of persistent output gaps, growth prospects are more promising. As we have seen in other parts of the world, the post‑pandemic reopening of economies can lead to a natural lift in domestic demand—and Asia is just at the beginning of this process. As the pace of reopening picks up across southeastern Asian nations in particular, some of those output gaps are likely to close

Inflation and Monetary Policy

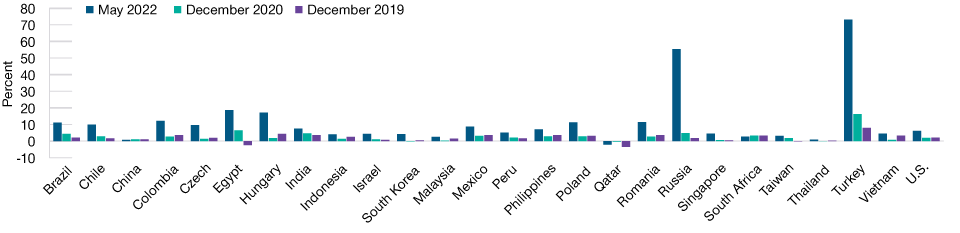

Inflation has continued to be a major problem across many EM countries, particularly in Latin America and central and Eastern Europe (Figure 1). Supply shocks and the global recovery have pushed up commodity prices, and the second‑round effects this time have also been significant. By contrast, Asia, South Africa, and Israel have seen limited inflation effects so far, partly due to their more persistent output gaps.

Energy and food are major components of EM consumer price indices (8% and 25%, respectively, on average). This means the first‑round effects from the Russia‑Ukraine conflict are likely to add 200bps–300bps to headline inflation in the near term. More problematic is the fact that some of these price shocks are likely to prove persistent given the damage done to the global fertilizer industry and ongoing uncertainty over how sanctions will affect Russia’s ability to export energy (and, hence, overall globally traded energy supply). This persistence means that even after inflation peaks, the overall disinflation process may take time.

The downside scenario for inflation would be a sharp slowdown in the global economy, particularly in the U.S. and China. While this is not our base case, the risk of this is rising, particularly given China’s struggle to get COVID-19 under control. Many EM central banks have been hiking rates aggressively due to their inflation targeting mandates. Most of the main middle‑income EMs—with the exception of Turkey—now have well‑institutionalized, inflation‑targeting mandates.

A key rule of thumb is that the hike in rates should match or exceed the rise in inflation. In this regard, the CEE/ Latin American central banks have largely matched or exceeded the year‑on‑year rise in core inflation. In Asia, the more developed economies have already started adjusting monetary policy as they have experienced a rise in inflation. Central banks in the Association of Southeast Asian Nations (ASEAN) region and India have yet to start raising rates but are expected to do so this year. China remains on a completely different trajectory, with the People’s Bank of China widely expected to cut rates—or at least ease monetary conditions—through other tools.

The Inflation Picture Across Emerging Markets Is Mixed

(Fig. 1) Europe and Latin America have been hit harder than Asia

As of May 31, 2022.

Chart shows 3‑month moving average inflation levels.

Source: Haver Analytics.

So far, the evidence of transmission from rate hikes is mixed. Credit growth remains above trend, or at least neutral in most countries, with little sign of slowing. However, M1 money supply1 growth has slowed sharply in the more aggressively hiking nations, which should eventually translate into slowing activity and credit growth.

Fiscal Policy

Many EM countries are in balance sheet repair mode as emergency pandemic spending rolls over and revenues begin to pick up. However, balance sheets are not yet back to where they were, and some countries in Asia (notably the Philippines, Thailand, and Malaysia) and Latin America (Colombia and Chile) are notable for having achieved limited fiscal consolidation so far. The Asian countries generally have the balance sheet space to continue to support their slower recovering economies; however, in Latin America, slower fiscal consolidation appears less warranted.

Commodity exporters are starting to see windfall revenues pick up. However, social pressures will see many EM countries recycle part of this revenue gain into subsidies for food and fuel, tax cuts, or other targeted social assistance. EM fiscal balance sheets deteriorated during the pandemic, but this should be viewed as a one‑off rise of debt/gross domestic product (GDP) levels by 10 percentage points on average. Given expected ongoing fiscal consolidation this year, particularly in Asia, debt levels should largely level off. This will leave the fiscal legacy of the COVID‑19 pandemic as primarily a small net increase in interest spending to GDP (by about 0.3% to 0.4% GDP given average borrowing costs of 3%–4%).

Longer term, the pandemic has thrown into starker relief the need for some countries to reform their revenue‑raising capacities, both to raise more revenue and to do so more efficiently. Several countries in Asia are pushing medium‑term tax reform agendas.

Rates and Currencies

Local rates have come under sustained pressure as upside inflation surprises and supply shocks continue. If or when inflation normalizes to central bank target rates, there will be considerable scope for a rally. There has been a notable repricing of forward policy rates with only three countries (Chile, the Czech Republic, and Poland) pricing in three‑year forward rates being below current policy rates. For countries that have been later to begin hiking rates, the markets are pricing in a long path to higher rates.

Markets will need to run with a higher risk premium on inflation for now. However, to the extent that hiking has become increasingly aggressive and the risks tilt toward a broader slowdown in growth, we may see somewhat faster inflation relief than is priced in, especially if global energy prices fall.

EM currencies have performed broadly along commodity lines. Exporters received a major bounce from the Russia‑Ukraine war shock, but this has since faded. Overall, EM currencies remain fundamentally cheap versus long‑term averages but lack a strong catalyst to perform outside of cyclical lifts from commodities or pickups in global growth and exports. The weakness in domestic growth drivers has been a limiting factor for EM currencies to more fundamentally revalue.

The U.S. dollar’s strength, fueled by the Fed’s more aggressive rate hiking stance and a decline in global risk sentiment, presents a difficult backdrop for EM currencies to perform. In particular, the weakness of the renminbi and the yen is a headwind for other Asian currencies. Given limited capital outflow channels in China, the influence of the renminbi has typically been felt more through real economy channels and on economies more connected to China.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

July 2022 / INVESTMENT INSIGHTS